Meal Replacement Products Market: Insights, Key Players, and Growth Analysis

Networking |

2026-06-29 07:54:59

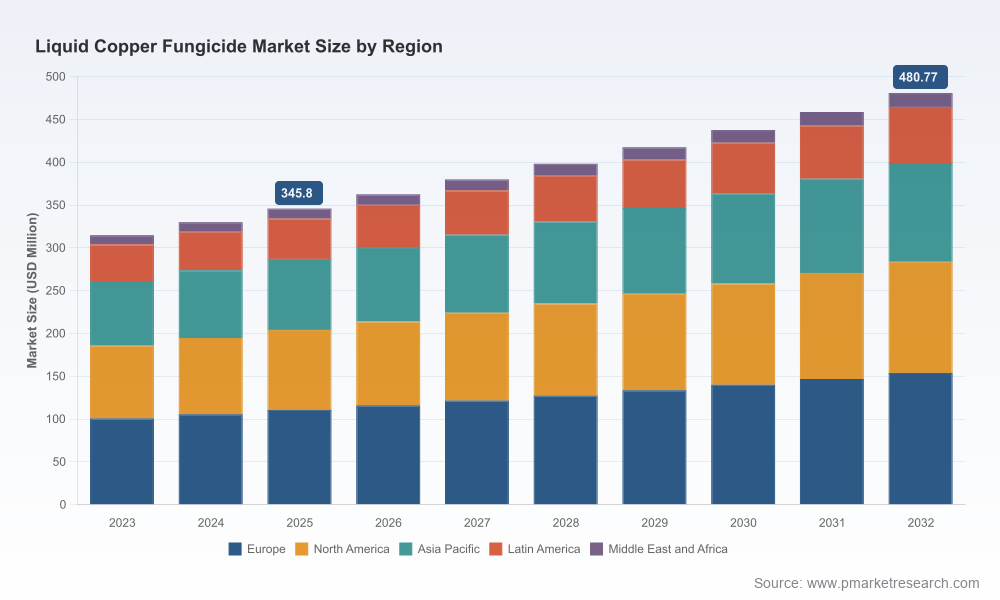

PW Consulting's latest market study on the Liquid Copper Fungicide Market (base year 2025; historical 2020–2025; forecast 2026–2032) delivers a forward-looking, decision-grade framework designed to inform boardroom choices and commercial playbooks for 2026 and beyond. The study quantifies a market that expanded from roughly USD 315 million in 2023 to an estimated USD 346 million in 2025 and is projected to reach approximately USD 481 million by 2032 at a compound annual growth rate (CAGR) of 4.82%. These headline numbers mask a more complex reality in which regulation, raw-material volatility, and tactical moves by both global majors and regional specialists are simultaneously compressing and creating value across the value chain.

Liquid Copper Fungicide Market

Regulatory risk is the dominant short-term headwind. European and national authorities are tightening conditions of use and elevating copper to candidate-for-substitution status in some jurisdictions, forcing product stewardship and reformulation choices that materially affect go-to-market plans.

Liquid Copper Fungicide Market

Input cost volatility and trade policy shifts mean procurement and pricing strategies can no longer be reactive. Recent spikes in copper salt prices and proposed tariffs on refined copper imports are already impacting manufacturing economics and margin models for liquid formulations.

Liquid Copper Fungicide Market

Innovation and channel strategy remain the most reliable levers to defend volume and premium positioning. Firms that combine formulation advances with distribution reach and farmer-facing agronomy services are outperforming peers in resilience and margin preservation.

Market structure is moderately concentrated: the top three players account for over a third of market revenue while the top five approach roughly half the market, indicating a mix of scale advantages and opportunity pockets for niche specialists and regional champions.

Regulatory tightening and stewardship requirements — Since mid-2025 regulators in Europe and selected national bodies have introduced stricter authorizations and conditions for copper-containing products to protect workers and the environment. EU-level limits on cumulative copper application and recent reclassification discussions have elevated compliance costs and shortened planning horizons for legacy products.

Raw-material and trade risk — Copper sulphate pricing and raw-material availability have shown significant swings driven by industrial demand and macro trade measures; an announced tariff posture in major consuming markets can raise the cost base for producers who rely on imported refined copper, compressing margins or passing costs downstream.

Product innovation and reformulation — The market is witnessing a two-track technical response: incremental improvements in copper delivery (to reduce total copper applied per hectare) and development of copper-alternative or copper-reducing technologies where allowed. These technical choices will determine which product lines remain viable under evolving regulation.

Channel differentiation — Growth in both professional agriculture and consumer/home & garden channels requires differentiated packaging, dosing convenience, and claims validation (e.g., organic-compatible options). Firms that align product formats with channel economics capture higher lifetime value.

M&A and distribution consolidation — Strategic acquisitions and portfolio shuffles are accelerating in Europe and North America as incumbents shore up distribution and regulatory expertise. Recent deals illustrate a playbook focused on combining complementary regional assets rather than large-scale blockbuster consolidations.

The competitive set spans global agrochemical integrators, regional formulators, and specialty producers. Multinational crop-protection companies continue to leverage R&D scale and integrated distribution to defend share, while nimble specialists and formulators target differentiated niches — organic-compatible solutions, suspension concentrates optimized for foliar uptake, and ready-to-use consumer products.

Global majors: Large agriscience firms bring breadth across crops and deep regulatory teams. Their play revolves around portfolio optimization, bundling with complementary actives, and investment in lower-dose technologies to adapt to regulatory constraints.

Regional formulators and distributors: Companies with strong local registration expertise and on-the-ground distribution can outcompete on speed-to-market and bespoke application support. Recent acquisitions highlight the strategic premium placed on European distribution networks.

Specialists and DIY brands: Home & garden and turf segments remain attractive for mature-product monetization and brand-led premiumization. Convenience formulations and clear consumer claims drive repeat purchase behavior in this segment.

Notable recent developments included product launches and regulatory authorizations that directly affect portfolio planning and market access. For example, new copper hydroxychloride products introduced into major markets illustrate how formulation innovation can broaden label claims and improve efficacy profiles. Meanwhile, regulatory agencies have issued renewed authorizations with stricter worker-protection conditions and environmental safeguards, underscoring the need for compliance-centered commercialization strategies.

This study is built for application, not just description. Key deliverables include:

Scenario-based demand models: Interactive forecasts that stress-test outcomes under different regulatory and tariff permutations for 2026–2032.

Regulatory risk matrix: A practical scorecard that ranks jurisdictions by near-term substitution risk, labeling complexity, and enforcement intensity to prioritize registration investments.

Supply-chain stress tests: Modular playbooks to assess supplier concentration, raw-material hedging needs, and reshoring vs. diversification trade-offs based on observed copper salt pricing and trade-policy signals.

Commercial playbooks: Channel-specific GTM templates for professional agriculture, seed/seedling nurseries, and consumer lawn & garden, including pricing elasticity guidance and promotional levers.

Technical roadmap and R&D prioritization: An evaluation framework for formulators to compare incremental copper-delivery improvements versus investment in copper-reducing alternatives, aligned to ROI and regulatory pathways.

Competitive benchmarking and M&A pipeline: Vendor scorecards, valuation multiples observed for recent deals, and a list of high-priority acquisition targets and distribution targets by strategic fit.

To honor the "preview" principle, the report intentionally omits granular public disclosure of core sub-segmentation figures in this press summary; the online report portal includes full tables, interactive dashboards, and downloadable data for licensed subscribers.

Rebalance portfolios toward stewardship-first products: Accelerate reformulation efforts and invest in lower-copper dose technologies to maintain label eligibility in high-risk jurisdictions.

Hedge and diversify supply chains: Given recent copper salt price volatility and trade-policy risk, build multi-sourcing strategies and contractual protections with upstream suppliers.

Sharpen go-to-market segmentation: Align product formats and pricing with channel economics — professional agronomy channels require efficacy and advisory services; consumer channels prize convenience and labeled safety.

Invest in regulatory and field-evidence capabilities: Resource regulatory teams and field-trial networks to shorten time-to-label and defend against substitution pressure.

Pursue targeted M&A and partnerships: Prioritize acquisitions that add distribution reach, local registration expertise, or formulation capabilities that reduce overall copper usage without sacrificing efficacy.

We combine sector expertise, regulatory intelligence, and commercial execution capabilities. Our advisory services for the liquid copper fungicide space include bespoke market-entry and market-exit strategies, supply-chain redesign and hedging plans, regulatory engagement roadmaps, product portfolio optimization, and M&A due diligence tailored to the nuances of copper-based chemistry. We also provide workshop-led scenario planning with your executive team to translate model outputs into executable 100-day and 12-month plans.

Leaders preparing budgets, R&D roadmaps, and M&A pipelines for 2026 should treat this study as a practical compass. The press summary above highlights the forces that will most influence commercial outcomes; the licensed report on PW Consulting’s portal contains the full segmentation, interactive forecasts, vendor scorecards, and downloadable data tables required to operationalize these insights. Access to the full report includes model files and a one-hour briefing with our lead industry analyst to walk through implications for your specific agenda.

For access to the complete Liquid Copper Fungicide Market report and the interactive decision tools, visit PW Consulting’s report hub or contact our agrochemical practice lead for a tailored briefing. As regulatory, raw-material, and commercial pressures converge in 2026, the next moves you make will determine whether your portfolio is constrained by compliance or enabled by strategic foresight.

For detailed analysis of this topic, please visit the official page:Liquid Copper Fungicide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com