Facade Systems Market Size, Industry Leaders & Competitive Landscape

Literature |

2026-05-12 11:32:08

PW Consulting today publishes a strategic industry briefing that synthesizes our new Aircraft Composite Enclosures Market research. Built on a rigorous historical base (2020–2025) and a forward-looking forecast window (2026–2032), the study equips senior executives, procurement leaders, product strategists, and M&A teams with the directional visibility they need to make high-confidence decisions in 2026 and beyond.

Aircraft Composite Enclosures Market

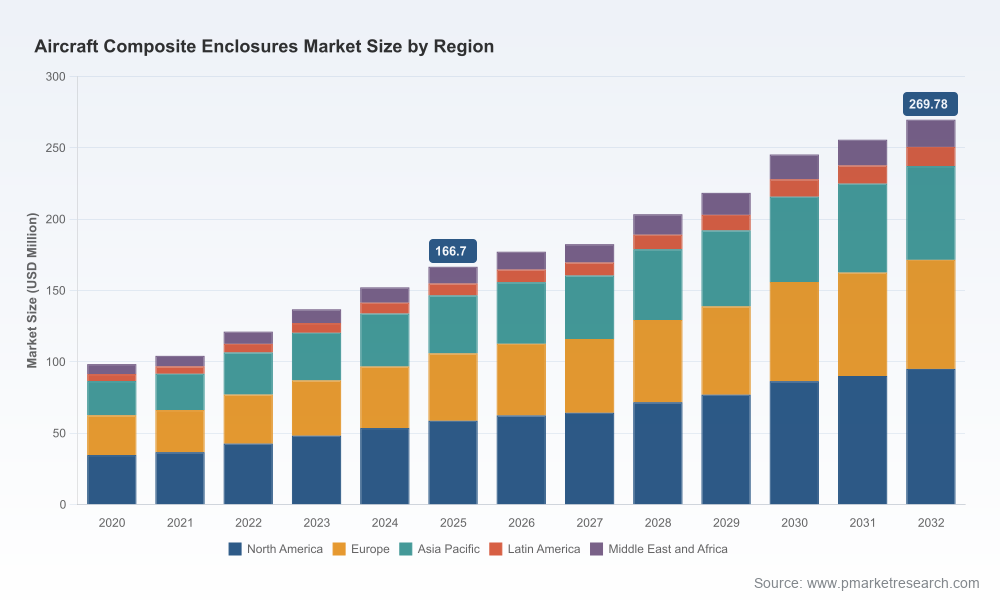

The aircraft composite enclosures market has transitioned from niche adoption to a mainstream component of aerospace systems engineering. Our modeling shows the market expanded materially over the last five years and, on the basis of the 2025 base year, is forecast to continue growing through 2032 at a compound annual growth rate of 7.12% (forecast period 2026–2032). This trajectory reflects a confluence of electrification of airframes, avionics densification, and sustained OEM prioritization of weight and corrosion advantages delivered by composite solutions.

Aircraft Composite Enclosures Market

For 2026, the practical implication is clear: organizations that act now to reconfigure supplier portfolios, lock in material supply resilience, and architect enclosure-centric product roadmaps will capture disproportionate share of incremental value. Those who wait risk paying premium prices, experiencing qualification delays, or losing specification influence in future platform procurements.

Aircraft Composite Enclosures Market

Three structural forces underpin the projected growth rate. First, systems densification and the shift toward more-electronic aircraft architectures increase demand for lightweight, high-performance enclosures that manage EMI, thermal loads, and structural integrity simultaneously. Second, material and process maturation — especially in automated layup, thermoplastic welding, and rapid cure chemistries — have reduced entry barriers for composite enclosure manufacture, improving unit economics. Third, procurement and lifecycle considerations — drive-to-zero emissions and lower operating weight — keep composite substitution compelling for both new platforms and retrofit programs.

At the same time, supply-side friction remains a near-term moderating factor. Raw-material inputs are exhibiting volatility: epoxy resin prices in North America reached USD 4.03/kg in March 2026, an increase of roughly 16.8% quarter-over-quarter, and aerospace-grade carbon fiber pricing continues to span a wide range. These dynamics make material sourcing strategies and long-term partnership agreements a central determinant of margin resilience.

The market exhibits a moderate degree of concentration. The top three suppliers account for a substantial minority share of the market, and the top five consolidate just over half of industry revenue — a structure that supports both supplier leverage and spaces for specialist competition. Within this environment, different player archetypes coexist:

Profiles of representative players included in the report:

Recent industry developments demonstrate the pace and nature of competitive moves. For example, a mid‑2026 strategic order secured by a major OEM highlighted the preference for composite-enclosed propulsion auxiliary systems in defense platforms, while early‑2026 long-term carbon-fiber supply agreements between major fiber producers and downstream integrators aim to stabilize availability and cost. Together, these signals indicate that companies securing material and integration continuity now will be advantaged in 2026 procurement cycles.

Regulatory guidance continues to evolve on composite airworthiness and qualification. Advisory frameworks require more rigorous test evidence and design allowables for composite structures used in aircraft systems, which increases up-front development time and pushes value toward vendors that can streamline qualification. Our report maps the practical steps engineering and certification teams must take to minimize schedule risk, including best-practice test matrices, allowable derivation approaches, and supplier audit checklists tailored to enclosure assemblies.

Unlike high-level summaries, this research is designed for operators. It combines granular manufacturing cost constructs, a supplier capability index, and scenario-ready demand models while preserving confidentiality-sensitive data that clients expect. The report balances prescriptive guidance (sourcing playbooks, certification timelines) with diagnostic tools (sensitivity analyses and acquisition due diligence templates) so that stakeholders not only understand market direction but can act to capture advantage in 2026.

To preserve the “trailer” utility of this briefing, we have intentionally omitted detailed segment-level tables and granular regional/application splits from this public release. The full report includes proprietary tables, downloadable Excel models, company scorecards, and appendices that quantify segment flows and supplier economics in ways that materially support negotiations, bidding, and M&A valuation. For organizations that require those datasets and the executable playbooks, the full deliverable and its supporting tools are available through PW Consulting’s customer portal.

For procurement directors, engineering heads, and corporate strategists preparing budgets and roadmaps for 2026, our recommendation is to secure access to the full report and its modeling artifacts before the start of Q3 2026. With material markets shifting and major suppliers locking in agreements, decisions made this year will determine competitive positioning for the remainder of the decade.

PW Consulting stands ready to deliver tailored briefings, workshops to integrate the report’s models into your planning systems, and bespoke advisory engagements to support supplier selection, partnership formation, or transaction diligence.

To request the full report, schedule a briefing, or obtain the proprietary Excel models referenced in this release, please contact your PW Consulting representative or visit our report landing page for this study.

For detailed analysis of this topic, please visit the official page:Aircraft Composite Enclosures Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com