Electronic Grade Barium Titanate Market to Hit USD 103.8 Million by 2032 at 6.6% CAGR

Other |

2026-06-17 13:29:43

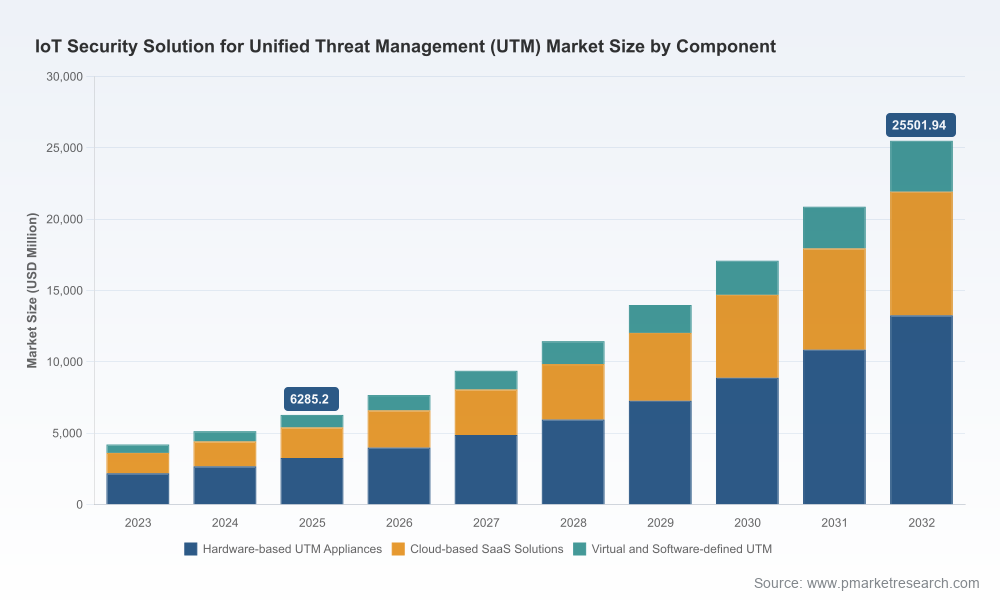

PW Consulting’s latest market study — "IoT Security Solution for Unified Threat Management (UTM) Market" — is released with a clear mandate: give security leaders and enterprise strategists the operational intelligence needed to make decisive architecture, procurement, and compliance choices in 2026. The study synthesizes historical performance (2020–2025), establishes 2025 as the analytical base year, and projects forward through 2032. Our macro findings are unequivocal: the IoT-focused UTM market is growing at a compound annual growth rate (CAGR) of 22.15%, moving from a multi-billion-dollar base in 2025 toward a substantially larger market by 2032. This brief highlights the strategic value of the report for 2026 decision cycles while preserving the detailed, actionable breakdowns behind the report’s paywall.

Iot Security Solution For Unified Threat Management Utm Market

Acceleration of connected assets: The pace of IoT deployments across industrial, healthcare, smart-city, retail, and logistics environments is creating a higher density of unmanaged endpoints. Enterprises that fail to consolidate threat management and visibility into a unified fabric will face disproportionate risk and operational friction.

Iot Security Solution For Unified Threat Management Utm Market

Regulatory inflection points: Several regulatory milestones that are in force or maturing by 2026 materially reshape vendor obligations and buyer risk profiles. The EU Cyber Resilience Act holds manufacturers accountable for product security across the lifecycle; the EU Data Act enshrines new data portability and anti-lock-in expectations; China’s Network Data Security Management Regulations and the U.S. DOJ Bulk Data Rule introduce layered constraints on cross-border processing and bulk data handling. Together, these regimes change procurement prerequisites and contractual expectations for both OEMs and enterprise buyers.

Iot Security Solution For Unified Threat Management Utm Market

Cost and infrastructure pressures: Rising data center construction costs and the economics of distributed compute influence decisions between hardware appliances, virtualized UTM, and cloud-native SaaS models. Our analysis shows these macroeconomic realities are a material part of total cost of ownership (TCO) calculus for security stack decisions in 2026.

Measured at scale, the market demonstrates robust expansion. After notable acceleration between 2023 and 2025, our projections show continued double‑digit growth through 2032. These macro numbers are intended to guide budgeting and strategic planning: security portfolios should be sized to participate in, and defend against, the dramatic growth of IoT-connected attack surfaces over the next investment cycle.

PW Consulting designed this study as an operational playbook for 2026 decision makers. Highlights include:

Vendor decision frameworks — comparative matrices that go beyond feature-checklists to evaluate integration cost, compliance fit, deployment velocity, and MSP/co‑managed operating models.

Deployment playbooks — step-by-step guides for common architectures (edge-appliance centric, hybrid virtualized stacks, cloud/SaaS-first), including reference network topologies, segmentation templates, and fallback procedures for phased migrations.

TCO and procurement modelling — configurable calculators that account for capital vs. operational cost drivers, hardware refresh cycles, licensing, managed services options, and regulatory compliance costs tied to data residency and lifecycle update obligations.

Compliance mapping — actionable mappings of major regulatory regimes to technical controls (e.g., secure update pipelines, device attestation, telemetry retention and portability), plus contract language templates for supplier SLAs and liability allocation.

Integration recipes and testing protocols — concrete guidance for integrating UTM platforms with IoT device management systems, SIEMs, and orchestration tooling, along with test scripts to validate segmentation, anomaly detection, and incident playbooks.

Use-case driven risk assessments — verticalized playbooks that prioritize controls for manufacturing OT, clinical device estates, urban infrastructure, and retail/distribution networks.

The UTM-for-IoT competitive set blends legacy firewall incumbents, cloud-first vendors, and specialized security appliance providers. Market concentration is meaningful but not dominant: the top three firms account for a significant share of vendor revenue, and the top five expand that footprint further, indicating both entrenched leadership and room for specialized challengers.

Fortinet, Inc. — FortiGate platforms remain a reference architecture for high-throughput, integrated NGFW + UTM deployments. Strengths: deep integration across security controls, strong ASIC-accelerated performance for hybrid models, and IoT-focused visibility/segmentation capabilities. Ideal for enterprises requiring scale and a consolidated management plane.

Cisco Systems, Inc. — Cisco combines Secure Firewall and Meraki MX offerings to cover the spectrum from core datacenter edge to simplified cloud-managed branches. Strengths: broad ecosystem integrations, global support footprint, and device-profiling that maps well to complex enterprise estates and service provider environments.

Check Point Software Technologies Ltd. — Check Point’s NGFW and CloudGuard suite emphasize policy-driven prevention, threat intelligence, and cloud-native controls. They are a natural fit where policy governance and centralized threat prevention across multi-cloud IoT ingestion points are priorities.

Sophos Ltd. — Sophos’ UTM and XDR convergences simplify operations for mid-market and distributed enterprises. Recent software refreshes further strengthen rule orchestration and ease-of-management — attractive for constrained security teams seeking rapid time-to-value.

WatchGuard Technologies, Inc. — WatchGuard positions strong in SMBs and channel-led models with focused appliances and coherent policy sets for IoT-friendly controls. Its strength is in straightforward deployment and channel enablement for managed services.

SonicWall Inc. — SonicWall continues to compete on price-to-performance for edge UTM appliances; its 2026 Generation 8 launch (with integrated ZTNA and co-managed services) signals a push to strengthen managed service provider propositions and warranty-backed offerings.

Barracuda Networks, Inc. — Barracuda’s CloudGen approach targets secure connectivity for distributed IoT estates, emphasizing simplified management and SaaS-enabled orchestration — useful for distributed retail and branch-heavy organizations.

Juniper Networks, Inc. — Juniper’s SRX line and AI-driven telemetry emphasize automated policy enforcement and anomaly detection. Their value is pronounced where adaptive, intent-based networking is paired with security operations automation.

Huawei Technologies Co. Ltd. — Huawei remains a major supplier in regions where its integrated networking and security stacks align with national infrastructure projects. Global buyers must weigh geopolitical and regulatory considerations alongside technical fit.

Palo Alto Networks, Inc. — PAN’s NGFW and platform strategy prioritizes device identification, Zero Trust principles, and consolidated prevention. Their platform depth makes them a frequent choice where program-level security posture and enforcement are prioritized across cloud and on‑prem estates.

Beyond these incumbents, 2026 product momentum also comes from new entrants and adjacent vendors making substantive moves into the secure access and SASE space — NETGEAR’s Exium-driven SASE offering and focal product updates from established players underscore the pace of competitive innovation.

Adopt a "composable" security architecture. Prioritize platforms that allow incremental integration (appliance, virtual, cloud) to reduce migration risk and preserve optionality against regulatory shifts.

Embed regulatory requirements into RFPs. For any procurement cycle in 2026, require lifecycle update commitments, provenance attestations, and data portability clauses aligned to EU and regional mandates.

Evaluate co-managed service models. Channel and MSP/co-managed offerings are maturing; where internal skill is constrained, co-management often delivers faster compliance and operational maturity than pure lift-and-shift.

Stress-test TCO against rising infrastructure costs. Model scenarios that include higher data center build and operational expenses; this will materially affect the “cloud vs. appliance” threshold for many buyers.

Focus on telemetry quality, not volume. With cross-border and bulk-data rules tightening, the ability to collect actionable, privacy-compliant telemetry will be decisive in detection and response efficacy.

Decision-makers should use the report as both a strategic primer and an operational toolkit. Security leaders will find the vendor evaluation frameworks useful for live RFPs; network architects will appreciate the deployment blueprints; legal and procurement teams will benefit from our compliance mapping and contract language templates. Importantly, the report is designed to be actionable within six to twelve months: it is time-boxed to 2026 priorities while projecting the competitive and regulatory path to 2032.

Schedule a briefing with PW Consulting to review the decision frameworks tailored to your vertical and regional footprint.

Use the included procurement templates and TCO models to re-scope any mid-2026 security procurements and pilot programs.

Engage our advisory arm to run an operational risk simulation against your IoT estate using the playbooks and testing protocols in the report.

PW Consulting’s market study is deliberately comprehensive, but this release serves as a strategic preview. For the full set of vendor scorecards, the detailed segment analyses, and the downloadable deployment templates and financial models, please consult the full report and supporting datasets on our website. The trends and tools within will help you make the high‑confidence decisions required to secure and scale IoT estates in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Iot Security Solution For Unified Threat Management Utm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com