Account Based Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-12 10:22:27

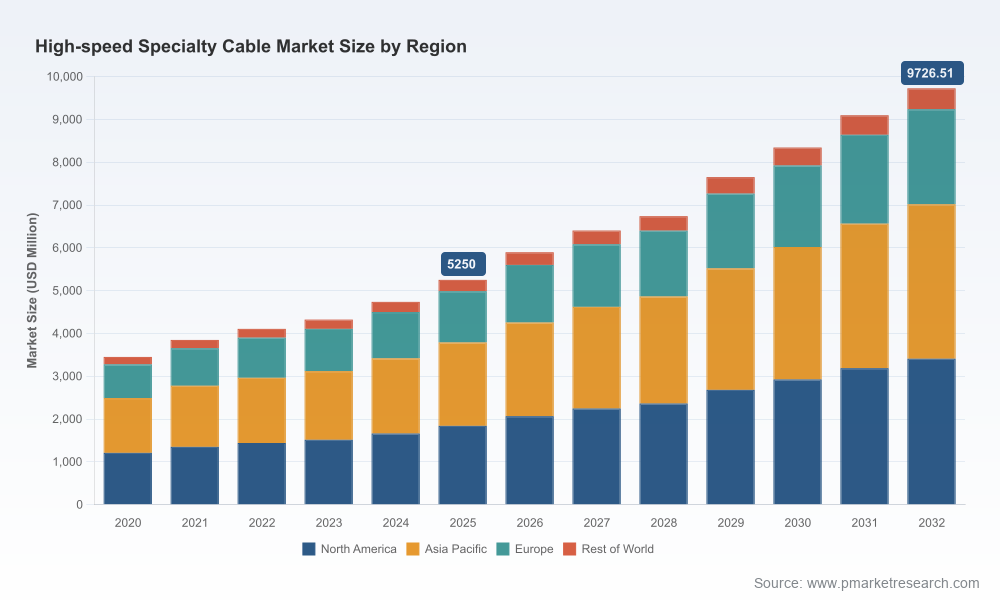

PW Consulting’s latest High Speed Specialty Cable Market report—anchored on a 2025 base year with historical coverage from 2020–2025 and a forward-looking forecast to 2032—arrives at a pivotal moment for infrastructure and systems planners. With the market estimated at roughly USD 5.25 billion in 2025 and projected to expand at a compound annual growth rate (CAGR) of 9.21% across the 2026–2032 forecast window, executives face a compressed decision horizon in which procurement, product architecture, and capital allocation choices made in 2026 will determine competitive positioning for the remainder of the decade.

High Speed Specialty Cable Market

As a “trailer” to the full dataset, this release reveals strategic signals and actionable frameworks while intentionally omitting granular regional splits and application-level tables to encourage users to consult the full report for detailed segmentation and downloadable models.

High Speed Specialty Cable Market

The high speed specialty cable market shows robust expansion driven by demand for higher throughput in data centers, telecom rollouts, industrial automation, and advanced mobility platforms. Our top-line numbers—an approximate USD 5.25 billion market in 2025 growing at a 9.21% CAGR—paint a picture of sustained opportunity but also rising complexity. Market concentration is meaningful but not overwhelming: the three largest players control just under forty percent of the market while the top five account for roughly half. This structure creates room for focused challengers and regional champions to capture niche premiums through technical differentiation, service excellence, or localized manufacturing.

High Speed Specialty Cable Market

Key inflection points for the coming 12–24 months include: (1) the pace of data center expansion and architectural shifts toward disaggregated compute; (2) telecom operators’ decisions on fiber densification and last-mile strategies; and (3) the rate at which industries adopt higher-speed cabling for industrial Ethernet, medical imaging, and avionics. Each of these will affect product mix, inventory strategies, and required capital intensity.

For 2026, procurement and strategy teams should treat raw-material volatility as an integral part of product-cost modeling rather than an exceptional contingency. Scenario-model outputs in our full report demonstrate how a set of plausible commodity and tariff shocks map to margin compression and recommended contract structures.

Technological evolution in the market is multi-dimensional. At the link and board level, the migration to higher-rate serial interfaces (and supporting ecosystems) is driving demand for lower-loss materials, tighter manufacturing tolerances, and new connector ecosystems. At the system level, buyers prize density, thermal performance, and predictable signal integrity under real-world conditions—metrics that increasingly favor hybrid optical/copper strategies and active optical cable solutions for certain applications.

Recent product innovations—high-density micro-distribution fiber, enhanced Category 6A and beyond copper solutions, and optimized cable assemblies for PCIe-class links—are examples of where vendor R&D is focused. Winning suppliers are translating these technical advancements into differentiated value propositions: reduced system power, simplified field-installation, and lower total cost of ownership (TCO) over multi-year refresh cycles.

The market features a mix of diversified conglomerates and specialized manufacturers. Large, global players bring manufacturing scale, broad product portfolios, and deep channel relationships; mid-sized specialists offer agility, customized engineering, and niche certifications that matter in defense, medical, and aerospace segments. Key vendor archetypes we assess include:

Recent corporate moves underscore these dynamics: a market leader reported significant organic expansion in high-speed interconnects and cable solutions; other suppliers launched new Category 6A and micro-distribution fiber products targeted at data-center densification; precision wire manufacturers announced capacity expansions to service high-performance cable manuf acturing. Taken together these developments signal a market gravitating toward higher value-add and supply-chain assuredness.

This study is built for executives and operating teams who must make 2026 decisions that lock in strategic trajectories. Key deliverables include:

Each tool is accompanied by clear assumptions, modeled scenarios, and a technical appendix explaining measurement protocols for high-speed performance—enabling internal teams to replicate, stress-test, and adapt models to their specific balance sheets and go-to-market timelines.

For corporate strategists, procurement leaders, product managers, and investors, PW Consulting’s High Speed Specialty Cable Market report is designed as both a decision-support manual and an execution playbook for 2026. The study couples top-line market sizing and a 9.21% compound annual growth framework with tactical tools—supplier scorecards, tariff and commodity sensitivity models, and go-to-market playbooks—so teams can convert insight into action quickly.

Please note: to preserve the “trailer” experience and drive practical engagement, this release highlights strategic findings and frameworks while withholding the full, table-level segmentation by region, type, and application. The complete datasets, downloadable scenario models, and the detailed vendor-by-vendor matrices are available on the report’s web page and are provided to subscribers and licensed purchasers.

Contact PW Consulting to access the full report, request a tailored executive briefing, or commission scenario work customized to your portfolio. The choices you make in 2026—on sourcing, technology adoption, and capital allocation—will determine not just near-term performance but the company’s structural position through 2032.

For detailed analysis of this topic, please visit the official page:High Speed Specialty Cable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com