Revealed: Municipal Pump Market Set to Transform with Sustainable Innovations

Other |

2026-06-22 10:04:42

PW Consulting’s newest market research brief on the Automotive Automatic Spray Guns market delivers a focused, actionable intelligence package intended to support high-stakes decisions in 2026. Built on a rigorous five-year historical base (2020–2025) and a seven-year forecast horizon (2026–2032), the study synthesizes macro growth trajectories, regulatory inflection points, supplier positioning, and implementation playbooks to help OEMs, Tier suppliers, industrial paint shops, and procurement teams orient strategy where it matters most.

Automotive Automatic Spray Guns Market

The market has shown steady expansion over the past half‑decade, rising from the low‑hundreds of USD Million in 2020 to a base‑year peak in 2025. Our modelling projects continued growth across the forecast window through 2032, with a compound annual growth rate (CAGR) of 5.85% from the 2026 base. This momentum reflects a combination of regulatory-driven technology adoption, fleet modernisation cycles, and increasing use of automation and electrostatic systems in high-volume lines. The shape of the curve in our base dataset highlights distinct cyclical responses to supply‑chain dynamics and raw material cost pressures, followed by a stronger recovery into the late‑2020s as manufacturers retrofit and expand automated finishing capacity.

Automotive Automatic Spray Guns Market

Regulatory regimes such as EPA NESHAP 6H and regional rules like South Coast AQMD Rule 1151 are accelerating adoption of HVLP or equivalent automatic spray systems by imposing VOC limits and equipment performance standards. In parallel, the EU VOC Directive continues to influence refinishing operations and aftermarket workflows. These rules create near‑term compliance obligations and long‑term incentive structures for low‑solvent, high‑transfer technologies.

Automotive Automatic Spray Guns Market

Robotic line integration, vision‑guided paint application, and smart nozzles are no longer experimental; they are table stakes in high‑throughput plants. The combination of precise atomization, repeatability, and reduced rework is driving demand for systems that can be seamlessly integrated into Industry 4.0 environments.

Rising costs for stainless steel and specialty alloys used in nozzle and gun assemblies have compressed margins for premium gun manufacturers and are influencing total cost of ownership (TCO) calculations. Manufacturers must weigh incremental equipment costs against solvent savings, reduced rework, and throughput gains.

While HVLP technologies maintain strong traction due to regulatory alignment, electrostatic and airless systems are gaining share in specific high-volume and powder application contexts. The optimal technology choice is often application‑specific and must be validated through factory trials and lifecycle costing.

The market exhibits moderate concentration: our CR3 and CR5 indicators demonstrate that the top three and top five players capture a significant portion of demand, making their strategic moves relevant to market entrants and incumbent purchasers alike.

Known for a broad portfolio including robotic‑ready and electrostatic options, Graco’s offerings emphasize transfer efficiency and integration with automated production cells—traits that appeal to high-volume OEM lines.

SATA positions itself on precision atomization and ergonomic design, with new premium models previewed recently—an important signal for premium automotive painting operations focused on finish quality.

With a heritage in advanced atomization, Anest Iwata’s refreshed catalogues underscore incremental performance improvements that matter in both OEM and refinishing contexts.

Nordson’s strength in electrostatic systems and powder coating positions it strongly where precision and transfer rates are critical in high-throughput lines.

These suppliers collectively provide complementary approaches from premium European engineering to cost‑competitive, customization‑oriented solutions from Asia—important options for procurement when balancing TCO, lead time, and after‑sales support.

Recent market activity reinforces these themes: a 2026 partnership between Fuji Spray Auto and technical education programs signals talent pipeline strengthening for collision repair equipment; product previews and catalog releases in 2025–2026 indicate supplier readiness to field next‑generation guns aligned with regulatory and automation trends.

Rather than a dry compendium, this study is structured as an operator’s toolkit for 2026 decision cycles. Components include:

Procurement leaders: Use our supplier benchmarking and TCO models to re-run RFQs with true lifecycle comparisons, not just purchase price. Engineering teams: Adopt the pilot playbooks to reduce integration risk and create repeatable commissioning scripts. Plant managers: Map retrofit phases to planned downtime windows and regulatory milestones to minimize production impact. Private equity and corporate development teams: Leverage concentration and growth metrics to prioritise targets for M&A or strategic partnerships.

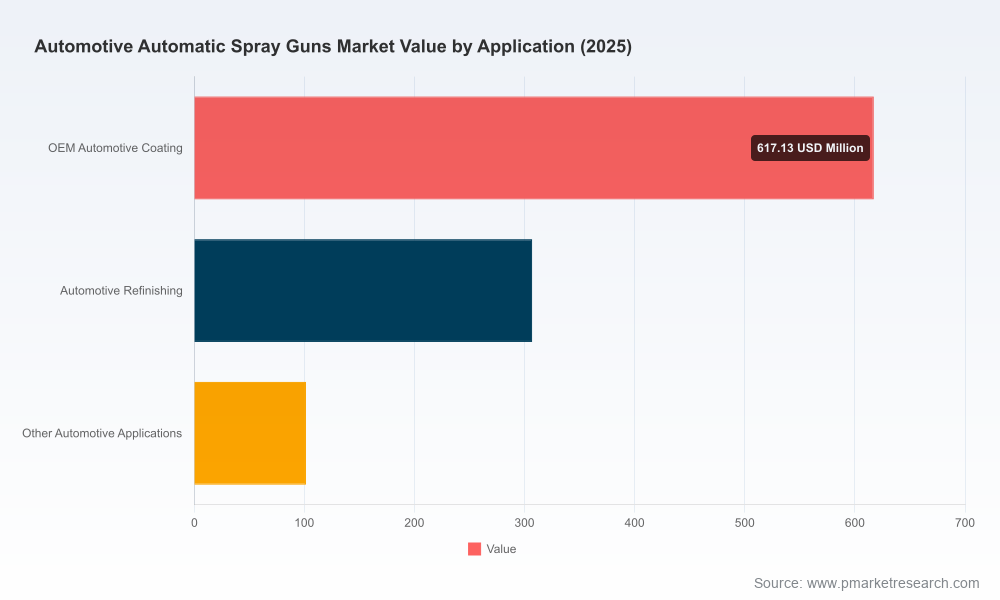

This article highlights the strategic contours that PW Consulting’s full report covers in operational depth. To preserve the utility of this summary as a gateway, we intentionally withheld granular regional splits and itemised application revenues here. The complete report supplies those critical tables, primary‑source interviews, and downloadable TCO tools that enable immediate deployment in 2026 planning cycles.

For teams preparing CapEx proposals, compliance remediation schedules, or supplier negotiations in 2026, the full study is the pragmatic next step—combining the big‑picture growth path (CAGR 5.85% from our 2026 baseline) with the micro‑level decision tools needed to convert strategy into measurable outcomes.

Contact PW Consulting to access the complete Automotive Automatic Spray Guns Market report and the associated spreadsheets, pilot protocols, and supplier scorecards that will make your 2026 decisions faster, more defensible, and ROI‑aligned.

For detailed analysis of this topic, please visit the official page:Automotive Automatic Spray Guns Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com