Essentials Clothing

Home |

2026-06-30 10:59:33

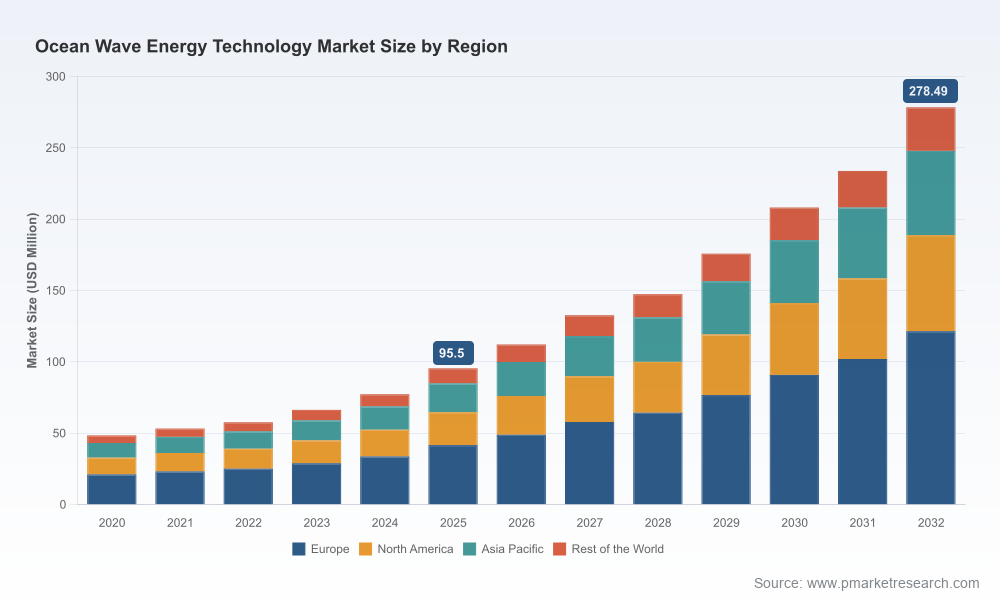

PW Consulting’s latest market research on Ocean Wave Energy Technology equips senior executives, investors, and policy-makers with the forward-looking intelligence needed to make high-consequence decisions in 2026. The global market is at an inflection point: after a period of early-stage demonstrations and selective commercialization, wave energy is entering a phase of accelerated scale-up. Our base-year assessment (2025) sizes the market at USD 95.5 million (revenue, Million USD basis) and our seven-year forecast to 2032 projects robust expansion to USD 278.49 million, reflecting a compound annual growth rate (CAGR) of 16.52% over the 2026–2032 period.

Ocean Wave Energy Technology Market

This release highlights the strategic value of the full PW Consulting report for 2026 planning cycles: it translates macro growth trajectories into actionable choices on portfolio allocation, technology selection, test-to-commercial pathways, and supply-chain resilience. This summary demonstrates the depth of our analysis while intentionally withholding proprietary split-level figures and unit economics that are available in the full report.

Ocean Wave Energy Technology Market

Transition from pilots to grid-integrated arrays: 2024–2025 produced multiple high-profile pilots and first-of-a-kind grid linkages. These programs validated core system concepts and created operational datasets that will underpin commercial bids and PPAs in 2026.

Ocean Wave Energy Technology Market

Capital formation and policy alignment are converging: public funding windows and utility-level procurement decisions scheduled for 2026 will materially shape which technology families access scale funding and long-term offtake.

Manufacturing and materials optimization are now procurement topics, not R&D debates—supply-chain choices made in 2026 will determine unit costs in the critical 2027–2030 window.

The market’s near-term scale-up is neither hypothetical nor uniform. Our model, calibrated to observed project outcomes and the latest operating metrics, shows an accelerating revenue curve beginning in 2026 and compounding through 2032. For executives this implies:

Prioritize modular scalability. Procurement strategies that favor modular, transportable architectures will reduce time-to-revenue and improve financing prospects for first commercial arrays.

Differentiate by the speed of grid integration. Firms with validated grid-connection experience and commercially proven power-take-off systems capture premium PPA opportunities.

Embed O&M discipline into bids. Operational data now permit realistic lifecycle cost models—proposals that demonstrate low OPEX relative to CAPEX (using accepted industry metrics) will be more bankable.

The PW Consulting report structures technology into a concise taxonomy—point absorbers, oscillating water columns, attenuators, overtopping devices, and hybrid variants—each carrying distinct implications for siting, survivability, and grid compatibility. Key technology takeaways for 2026 planners:

Point absorbers and advanced PTOs: compact point absorbers with high wave-to-wire efficiency have moved from concept to demonstrated survivability in severe conditions. These systems command investor attention where array density and marine logistics favor smaller footprints.

Nearshore converters and bottom-mounted systems: oscillating surge and bottom-mounted converters offer lower visual impact and simplified cable routes, making them attractive for early utility-scale nearshore deployments.

Multi-service designs: coupling electricity production with desalination or platform-power services accelerates utility offtake opportunities in water-scarce coastal regions and for offshore operators.

Materials and manufacturability: the uptake of modern composite manufacturing—especially filament-wound GFRP components—is altering unit mass, durability, and production economics; supply-chain strategies must be adapted accordingly.

Wave energy is moving from bespoke fabrication toward repeatable manufacturing. Our analysis identifies three procurement levers that corporate planners should prioritize in 2026:

Materials standardization: early alignment with composite fabricators and marine-grade component suppliers reduces lead times and cost volatility as production ramps.

Test staking and logistics: proximity to accredited open-water test sites and ports with service infrastructure materially shortens the commercialization timeline and lowers transportation risk premia.

O&M and digitalization: automation and remote monitoring upgrades demonstrated in recent projects materially cut year-one O&M budgets and improve data quality for future design iterations.

The sector remains moderately fragmented: the top three firms account for roughly a third of identifiable market activity and the top five remain below half. This concentration profile signals both opportunity for new entrants and the need for incumbents to secure differentiating assets. Notable firms profiled in our report include (non-exhaustive):

Eco Wave Power — innovating onshore floater solutions that attach to existing marine infrastructure and recently completed a high-visibility pilot in Los Angeles while achieving strong OPEX outcomes in Israeli operations. These operational milestones strengthen its position in collaborations with port authorities and energy majors.

CorPower Ocean — advancing compact point absorber designs with biomimetic PTO concepts; recent deployments at Portuguese test sites demonstrated survivability in severe storm regimes and paved the way for commercial-array plans.

Carnegie Clean Energy — combining submerged actuator-based generation with desalination capability, representing a differentiated product-market fit where water and power co-delivery is a strategic priority.

Ocean Power Technologies, AW-Energy, Mocean Energy, Oscilla Power, CalWave, ORPC, Seabased, NoviOcean, Marine Power Systems — each brings distinctive technological approaches and market entry strategies targeting either utility-scale power, remote/off-grid markets, or multi-service offshore platforms.

The full report provides comparative capabilities matrices, development roadmaps, and a curated set of vendor diligence questions. We intentionally omit tabular financials and unit-level metrics in this public summary to preserve the actionable granularity reserved for subscribers.

Public funding windows are significant and prescriptive. For example, multi-year federal programs targeting device development and open-water testing create matched-capital opportunities that savvy sponsors can layer with private capital to de-risk first commercial arrays.

Utility procurement is nascent but accelerating. The first continental U.S. PPA awards tied to wave facilities create an emergent market reference price and a template for future offtake agreements.

PPAs and blended financing structures will favor technologies that can demonstrate standardized performance metrics, replicable maintenance regimes, and clear escalation clauses for curtailment and force majeure.

Invest early in performance data acquisition. Short-duration investments in instrumentation and naval-hub partnerships yield disproportionate returns in bid competitiveness and insurer confidence.

Lock strategic test-site access. Securing berthing, cable corridors, and local community engagement at accredited test centers should be treated as a priority procurement item.

Layer financing with grants and PPAs. Structure deals to capture public funding while preserving equity upside—this is especially relevant for projects targeting first-mover utility contracts.

Design for maintainability. Prioritize modular PTOs, rapid retrieval capabilities, and remote diagnostics to reduce life-cycle cost and improve vessel utilization.

The full Ocean Wave Energy Technology Market report (base year 2025, forecast 2026–2032) contains the proprietary quantitative models and strategic tools needed for board-level decision-making, including:

Revenue and unit-growth projections with sensitivity scenarios (high/central/low) across the forecast period;

A granular technology assessment with readiness scoring, cost trajectories, and failure-mode analyses;

Supplier and materials risk heatmaps, including composite manufacturing capacity and long-lead sourcing constraints;

Competitive profiles with capability matrices, recent project outcomes, and partnership-fit assessments;

Investment and procurement checklists tailored to strategic buyers, project sponsors, and lenders.

Because our aim in this public bulletin is to provide strategic orientation rather than exhaustive data, we have intentionally omitted split-level region and application share tables and unit-specific pricing. These are available in the subscriber-only dataset alongside our financial models and scenario dashboards.

Wave energy is emerging from demonstration into selective commercial viability. The market’s projected trajectory—from a USD 95.5 million base in 2025 to a materially larger market by 2032 at a 16.52% CAGR—creates a narrow window in 2026 for firms to secure the strategic assets, partnerships, and funding structures that will define market leaders. PW Consulting’s full report provides the tactical playbook and proprietary datasets required to translate this structural growth into defensible competitive advantage.

To access the full report, including model outputs, segmentation tables, and the complete competitive due-diligence toolkit, visit PW Consulting’s Ocean Wave Energy Technology Market page or contact our industry practice lead for a briefing and bespoke scenario run.

For detailed analysis of this topic, please visit the official page:Ocean Wave Energy Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com