Solid State Transformers Market Dynamics: Key Drivers and Restraints

Other |

2026-05-14 11:53:37

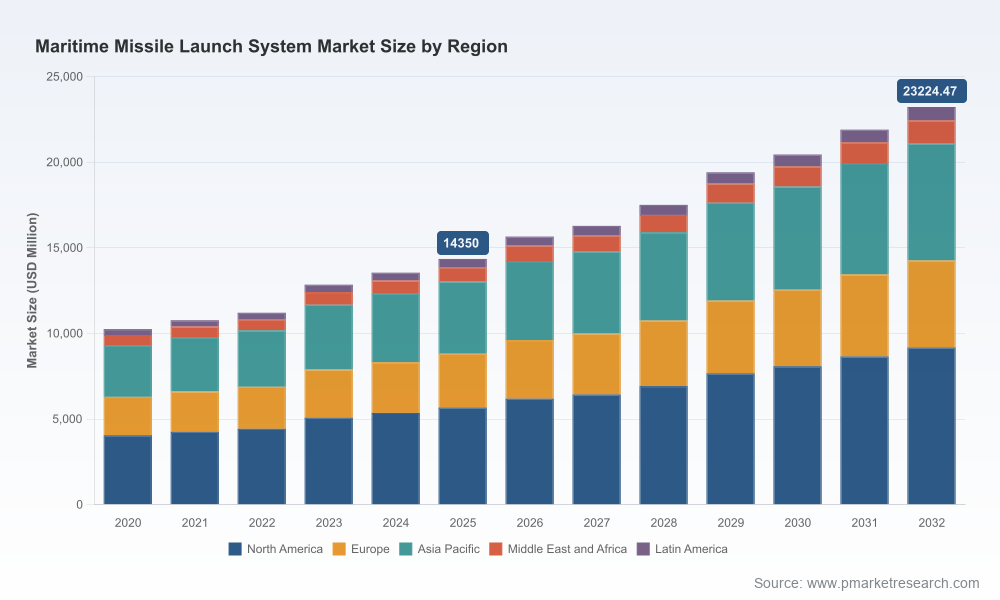

PW Consulting today releases its latest deep-dive into the Maritime Missile Launch System (MMLS) market, built to inform board-level decisions, program prioritization, and deal strategies heading into 2026. Anchored on a base year of 2025 and a calibrated historical series from 2020–2025, our model projects the market through 2032. The market is expected to expand at a compound annual growth rate (CAGR) of 7.12% across the 2026–2032 forecast window, rising from an estimated USD 14,350 million in 2025 to roughly USD 23,224 million by 2032. This outlook synthesizes procurement pipelines, platform modernizations, supply-chain stress tests, and policy risk scenarios to produce actionable guidance for OEMs, integrators, component suppliers, and defense customers.

Maritime Missile Launch System Market

Macro visibility with operational detail: The study combines a statistical market model with program-level assessments and procurement timing windows to convert long-term demand trends into near-term business opportunities and delivery risks.

Maritime Missile Launch System Market

Risk-informed investment roadmaps: We translate geopolitical and industrial constraints into quantified implications for revenue timing, margin pressure, and capital allocation — the practical inputs CFOs and investment teams need when setting 2026 budgets.

Maritime Missile Launch System Market

Competitive playbooks: Beyond market sizing, the report maps capability gaps among tier-1 vendors and identifies commercially viable partnership and M&A targets that accelerate access to key platforms and export markets.

Geopolitics is the demand engine. Rising strategic competition in the Indo‑Pacific has translated into measurable uplifts in allied procurement postures and capability refresh cycles. Our analysis finds that defense budgets and procurement priorities in the region are materially altering program timing and platform mix — an essential consideration for suppliers prioritizing program capture in 2026.

Alliance frameworks accelerate interoperability. Initiatives such as AUKUS are catalyzing common standards and technical convergence for VLS interoperability between select partners, shortening integration cycles for compliant suppliers and elevating the strategic value of modular, open-architecture launch systems.

Export controls and regulatory friction. Stringent export control regimes (notably ITAR) continue to constrain cross-border technology flows and necessitate robust compliance and localization strategies from vendors seeking to participate in allied procurement programs.

Supply-chain and material pressures. Specialized inputs — for example, high-strength steels used in canisters and launch cells — have experienced supply tightness and price appreciation. Our supply-chain stress tests demonstrate how a sustained price shock or lead-time extension can compress supplier margins and delay retrofit programs unless proactively hedged or mitigated through nearshoring.

Top-down market model and bottom-up program mapping — multi-scenario forecasts that reconcile procurement budgets, shipbuilding schedules, and upgrade cycles to produce timing-sensitive revenue curves through 2032.

Technology and platform playbooks — capability matrices for Vertical Launching Systems (VLS), single-cell and inclined launchers, decoy systems, and platform integration profiles (surface combatants, submarines, patrol vessels).

Supplier capability mapping and partner shortlists — comparative analysis of manufacturers, integrators, and subsystem suppliers including delivery track records, integration depth, and aftermarket positioning.

Procurement risk and compliance toolkit — export-control impact assessment, localization threshold models, and contracting clauses to insulate OEMs from sanction-driven program stoppages.

Commercial response playbooks — five actionable GTM strategies by segment (OEM, subsystem, service), including pricing models for upgrades vs. new-builds and capture plans for follow-on sustainment revenue.

Scenario simulations — high-, base-, and low-growth scenarios that stress-test the business case for new product launches, production capacity expansions, and M&A transactions.

The MMLS market exhibits meaningful concentration at the top. The leading three vendors account for a dominant share of installed VLS capacity and ongoing retrofit contracts, with the top five aggregating an even larger portion of the market. This concentration underscores both entry barriers for new entrants and potential transactional pathways for mid-tier players seeking scale through alliances or carve-ins.

Lockheed Martin (United States) — Deeply embedded through AEGIS combat system integrations and Mk 41 VLS deliveries. Lockheed’s recent deliveries of Mk 41 modules for next‑generation destroyers reinforce its status as a go-to integrator for large fleet programs.

BAE Systems (United Kingdom) — Strong platform integration pedigree and recent contract awards to upgrade allied destroyer VLS suites highlight BAE’s strategic focus on sustainment and retrofit opportunities beyond new-builds.

Raytheon Technologies (RTX, United States) — Offers advanced gun and launcher integrations and maintains significant systems-integration capabilities that pair launchers with sensor and effectors across surface combatants.

MBDA (France/UK/Italy) — Supplier of SYLVER VLS solutions in Europe; continues to pursue upgrades and interoperability demonstrations that can accelerate European fleet modernization.

Naval Group, Leonardo, Thales, Saab — Regional system integrators and subsystem specialists who command platform-specific relationships. Recent platform launches and exhibition showcases indicate a continued emphasis on modularity and exportable solutions.

Recent industry moves reinforce these dynamics: Lockheed Martin’s late‑2025 deliveries of Mk 41 modules, BAE’s 2025 contract to upgrade allied destroyers, MBDA’s mid‑2025 showcase of SYLVER upgrades, and Naval Group’s launch of a modern frigate with integrated VLS—all point to active replacement and upgrade cycles that will shape supplier order books in 2026 and beyond.

For OEMs and system integrators: prioritize interoperability and modular open interfaces. Winning major volume programs increasingly hinges on demonstrable ease of integration with allied combat systems and common launcher standards.

For component suppliers: secure long-lead material contracts and diversify sourcing. Given recent material-price pressure and lead-time risk, locking supply through strategic LPAs and nearshoring can be a decisive differentiator.

For defense customers: adopt staged procurement with sustainment-linked contracts. Structuring purchases to combine capability upgrades with long-term sustainment commitments reduces lifecycle cost and incentivizes supplier investment in local supply bases.

For investors and M&A strategists: target mid-tier subsystem vendors that provide high-margin aftermarket services or unique interoperability modules—these offer attractive bolt-on opportunities to broaden solution sets without competing directly on large platform deliveries.

Across the board: build robust export compliance programs. ITAR and allied export regimes materially affect route-to-market; early investment in licensing and dual-use engineering will accelerate program participation and limit bid disqualification risk.

Our base-case leverages the consensus macro and defense procurement trajectories and applies a 7.12% CAGR across the forecast. Two deviant scenarios are of critical importance to 2026 planning:

Upside scenario — accelerated procurement driven by regional crises and rapid fleet recapitalization, which compresses program schedules and benefits suppliers with modular, proven VLS offerings and spare capacity.

Downside scenario — heightened export restrictions plus persistent supply-chain inflation that delays retrofits and raises program costs, disproportionately impacting firms with single-source suppliers and limited compliance infrastructure.

Custom market-sizing and procurement timing workshops to translate the report’s scenarios into specific revenue forecasts for your product lines.

Supplier-readiness assessments and localization strategies to insulate programs from export and material risks.

M&A diligence and integration playbooks focused on consolidating subsystem capabilities and aftermarket revenue streams.

This press overview highlights the strategic contours of the MMLS market for 2026 planning, but omits granular segment-level allocations and country-by-country forecasts that are included in the full PW Consulting report and accompanying datasets. If your organization is preparing contract bids, investment memoranda, or program roadmaps for 2026, accessing the complete dataset and scenario spreadsheets will provide the detailed segmentation and timing inputs required to act with conviction.

Contact PW Consulting to request the full Maritime Missile Launch System Market report, regional and platform-level breakdowns, and tailored advisory packages for bid capture, supplier strategy, and compliance readiness.

For detailed analysis of this topic, please visit the official page:Maritime Missile Launch System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com