Cold Press Juice Market Trends Every Business Must Watch in 2026

Food |

2026-04-01 06:19:24

PW Consulting’s new 4-Bromoanisole Market report (base year 2025) delivers an actionable intelligence set designed to guide commercial, procurement and R&D decisions through the 2026 planning cycle and beyond. The global market has expanded steadily in the first half of the decade—rising from roughly USD 46 million in 2020 to about USD 56.7 million in 2025—and is forecast to continue on an upward trajectory through 2032. Our 2026–2032 forecast (CAGR ~4.52%) frames a market environment that rewards disciplined supply-chain management, targeted product differentiation, and regulatory foresight.

4 Bromoanisole Market

Strategic timing: 2026 is the inflection year for many buyers and producers as legacy procurement contracts roll over and capital projects sanctioned during 2023–2025 come online. The report surfaces the near-term variables that will determine margin performance in that transition.

4 Bromoanisole Market

Clear growth trajectory: With annualized growth established in the 2020–2025 window and continued expansion projected to 2032, executives must now translate growth forecasts into portfolio and capacity choices that balance volume ambition with margin protection.

4 Bromoanisole Market

Operational risk factoring: Our analysis integrates recent supply shocks, regulatory updates and tariff dynamics to quantify downside scenarios that often are overlooked in headline demand forecasts.

Market sizing & multi-horizon forecasting: End-to-end historical series (2020–2025) and a detailed forecast through 2032, with scenario overlays for supply volatility, downstream demand swings and regulatory change.

Commercial playbooks: Tender and pricing strategies by buyer archetype; segmentation of commercial levers for contract manufacturers vs. captive users; negotiation templates and KPI benchmarks.

Supply-chain mapping: Supplier scorecards, geopolitical risk heat maps, and critical-path analysis for feedstocks and intermediates, enabling quicker supplier qualification and dual-sourcing plans.

Regulatory & compliance matrix: Practical actions to align with chemical safety frameworks and registration requirements, including recommended timelines for dossier completion and SDS updates.

M&A and partnership intelligence: A shortlist of strategic targets and collaboration models—ranging from toll-manufacturing partnerships to bolt-on acquisitions—tailored to buy-side objectives and integration complexity.

Commercial models & price-sensitivity tools: Proprietary elasticity models and revenue-impact calculators that let teams quantify how raw-material swings and tariff scenarios affect both pricing and gross margins.

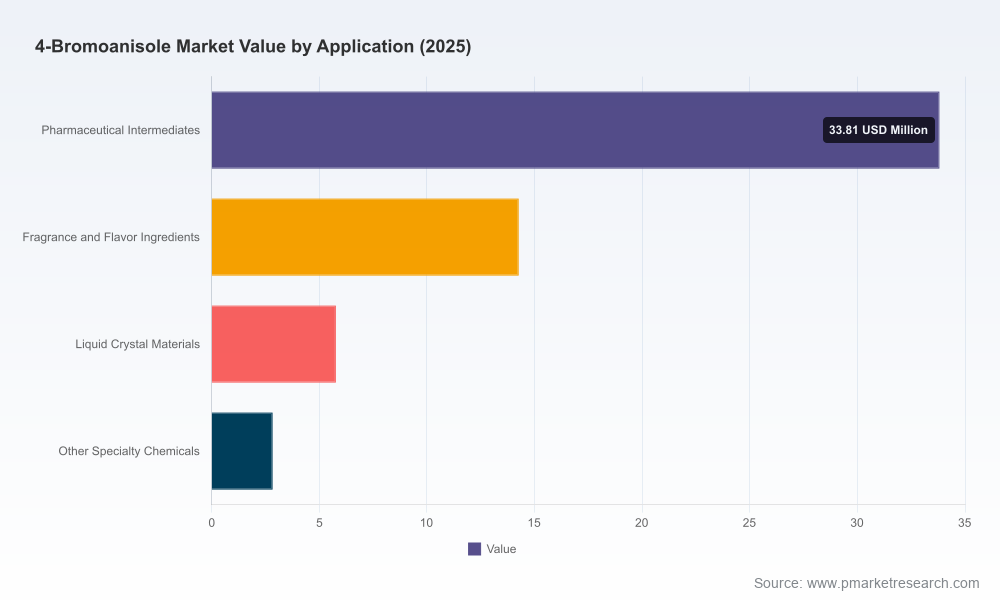

Demand drivers: Pharmaceutical intermediate synthesis, specialty materials and selected fine-chemical applications continue to underpin steady demand. Buyers in pharma and specialty materials are increasingly emphasizing traceability and quality certifications, which raises the commercial value of higher-purity grades and robust analytical documentation.

Raw-material volatility: Late-2025 supply constraints in certain bromine-producing regions created a material price spike and highlighted single-sourcing exposures across the value chain. Concurrently, shortages in phenolic derivatives have tightened the feedstock market for anisole family compounds—effects that ripple into procurement lead times and cost bases.

Regulatory tightening: The European regulatory landscape has evolved to require enhanced safety documentation and specific restrictions under existing chemical control frameworks. For companies active in ECHA-jurisdiction markets, extended dossier requirements and tightened downstream user obligations must be accounted for in go-to-market timelines.

Trade policy continuity: Recent trade reviews left existing tariff positions on brominated anisoles unchanged. This predictability helps landed-cost modeling but does not remove exposure to non-tariff measures and customs-related friction that vary by trading corridor.

Market concentration: The global supplier base shows measurable concentration at the senior tier. The top three suppliers control a meaningful portion of global supply while the top five collectively account for a majority—situations that create both cooperative and competitive opportunities for buyers and new entrants.

PW Consulting’s competitive analysis profiles incumbent chemical distributors, specialty suppliers and niche manufacturers. Leading laboratory- and industry-focused suppliers provide a range of pack sizes, purity grades and value-added services that address distinct buyer needs.

Sigma-Aldrich (Merck KGaA) — Operating from its European HQ, this supplier leverages global distribution and rigorous quality control for lab-grade and pharmaceutical synthesis applications. Their product strategy targets research and regulated workflows where documented traceability and small-batch availability are critical.

Alfa Aesar (Thermo Fisher Scientific) — Positioned in North America, Alfa Aesar blends broad product catalogs with supply reliability to serve organic synthesis and fine-chemical customers seeking high-purity intermediates.

TCI America (Tokyo Chemical Industry) — Focused on material science and pharmaceutical intermediates, TCI combines targeted regional stocking with technical support for customers advancing complex synthetic routes.

Apollo Scientific — Based in the UK, Apollo’s flexible packaging and broader bulk availability make it a logical partner for industrial-scale users pursuing aryl-halide chemistry at scale.

Combi-Blocks — With a specialization in custom quantities and building-block libraries, Combi-Blocks is aligned with early-stage drug-discovery workflows and small-batch synthesis services.

Biosynth — Their GMP-oriented capability and analytical support make them a preferred option for pharmaceutical R&D programs requiring regulatory-grade documentation and lot-release testing.

Oakwood Chemical — Known for custom synthesis and higher-purity materials, Oakwood serves customers with specific formulation or process requirements that necessitate bespoke manufacturing.

Each of these firms pursues a distinct combination of product breadth, pack-scale flexibility, regulatory assurance and customer support. The report provides supplier scorecards and engagement playbooks to help buyers and investors identify the right partner archetype for their strategy.

Shift from spot buying to hybrid contracts: Introduce blended procurement frameworks that combine shorter spot coverage with strategic forward purchase agreements tied to clear service-level commitments. This reduces exposure to feedstock-driven compressions while keeping optionality for demand spikes.

Prioritize regulatory-driven product segmentation: Segment offerings into clearly defined commercial tiers—e.g., research, industrial, and regulated pharmaceutical grades—with differentiated pricing and QA/QC pathways to capture premium value where it exists.

Invest in dual-sourcing and regional stocking: Where feasible, develop parallel supply corridors and regional buffer inventory to mitigate single-point failures from supplier or logistics disruptions; consider strategic tolling agreements to preserve continuity for captive processes.

Embed raw-material stress-testing in capital decisions: Use scenario-weighted IRR and margin models that explicitly incorporate raw-material supply constraints and timeline slippage—this will materially improve project selection quality.

Consider bolt-on capacity to secure specialized grades: For mid-sized specialty chemical players, selectively acquiring or partnering with niche producers (e.g., firms offering GMP or higher-purity capabilities) can shorten time-to-market for regulated customers.

Operationalize sustainability and compliance as commercial assets: Stricter documentation and lifecycle reporting are becoming procurement table stakes—invest in analytical traceability and SDS management to convert compliance into a competitive differentiator.

Beyond market-level forecasts, the report equips teams with immediately deployable tools: contract negotiation playbooks, supplier audit checklists, regulatory red-line matrices, and customizable pricing-sensitivity templates. For commercial leaders, our revenue-impact models translate supply scenarios into concrete P&L outcomes; for procurement, our supplier-risk framework converts qualitative supplier intelligence into quantifiable scorecards.

The full PW Consulting 4-Bromoanisole Market report includes segment-level demand estimates, supplier capacity balances, and a prioritized list of acquisition and partnership targets—data that we intentionally reserve for the report itself to maintain its commercial value. Readers seeking the granular intelligence necessary for contract renewals, capital allocation, or M&A screening in 2026 should consult the full dataset and proprietary models.

To request the complete report, supplier scorecards or a briefing tailored to your company’s risk profile, contact PW Consulting’s chemical industry team. Our analysts can deliver a customized workshop to translate the report’s insights into a 90–day action plan aligned with your 2026 objectives.

For detailed analysis of this topic, please visit the official page:4 Bromoanisole Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com