Robotic Dentistry Market Latest Trend, Growth, Size, Application & Forecast by 2031

Other |

2026-05-25 08:15:04

As organizations finalize capital allocation and operational roadmaps for 2026, the aerial inspections service market has crystallized into a high-growth, technology-led sector that demands executive attention. Our latest market research — anchored on a 2025 base year and projecting through 2032 — shows a sustained compound annual growth rate (CAGR) of 13.5%. From a mid-decade vantage point, this trajectory signals both immediate implementation opportunities and a multi-year strategic agenda for enterprises that manage large-scale infrastructure, energy assets, or dispersed industrial portfolios.

Aerial Inspections Service Market

Three converging forces make 2026 a decisive planning horizon. First, the economics are now compelling: aerial inspection solutions routinely shave inspection time and operational cost materially versus traditional rope access and scaffolding approaches, with documented uplifts that accelerate payback on capital and service investments. Second, a fast-evolving regulatory backdrop — including baseline commercial pilot frameworks and active rulemaking for beyond-visual-line-of-sight (BVLOS) operations — is reshaping what scale and operational design are feasible this year. Third, technology maturation in autonomy, sensor fusion, and AI analytics has moved the industry beyond proof-of-concept into scalable deployments.

Aerial Inspections Service Market

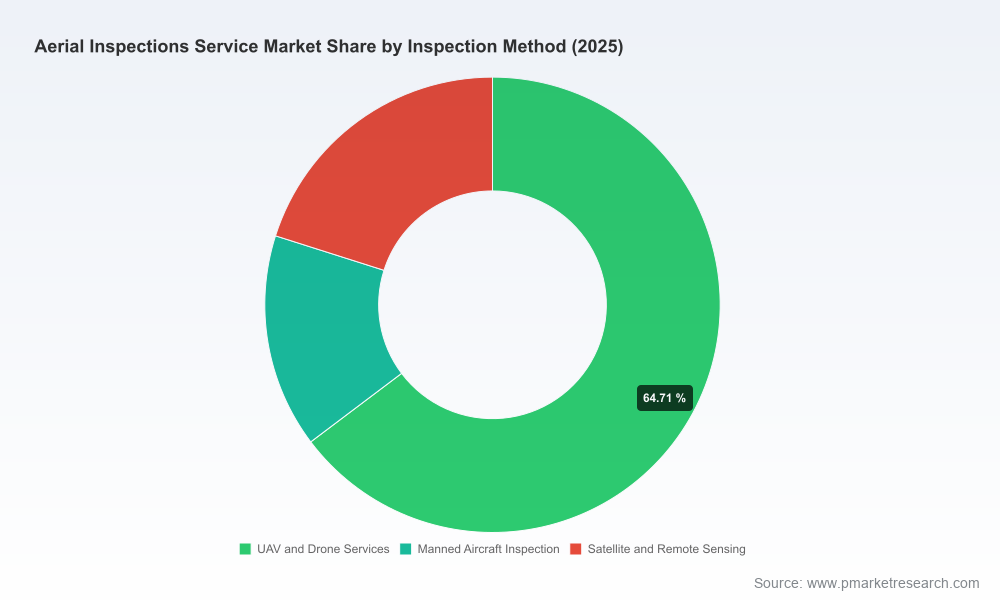

Our topline modeled market values show a robust expansion from the mid-2020s into the early 2030s. The topline growth pattern underscores predictable demand across industrial verticals and inspection modalities, and the market’s long runway is reflected in the report’s forecast through 2032. Yet the market remains fragmented: the largest players account for only a modest portion of total revenue, indicating substantial white space for differentiated propositions — whether through vertical specialization, proprietary data platforms, or managed services that tie aerial data to enterprise asset management systems.

Aerial Inspections Service Market

PW Consulting’s Aerial Inspections Service Market report is designed as an operational playbook as much as a market analysis. Beyond macro forecasts and qualitative trend narratives, the report contains:

Each of these modules includes worked examples, decision trees, and red-team considerations to ensure that executives can translate strategy into measurable execution plans without reinventing evaluation processes.

The report profiles leading service providers that illustrate three dominant strategic archetypes in the market: global integrators with deep vertical reach, platform-first providers offering enterprise-scale data management, and specialist systems players targeting high-value niches.

Recent industry developments captured in the research illustrate the market’s dynamism: major enterprise agreements standardizing reality capture across project portfolios, platform feature releases that materially cut processing times, and strategic launches expanding service coverage into offshore and subsea domains. These moves underscore a competitive battlefield that rewards both platform scale and sector specialization.

Regulatory changes are a double-edged sword. Continued reliance on baseline commercial pilot certifications remains a gating factor for many service providers, and the regulatory focus in 2026 includes enhanced enforcement initiatives and expedited violation resolution mechanisms. At the same time, proposed rulemaking for BVLOS operations and critical-infrastructure exceptions promises to unlock new productivity and reach for compliant operators.

Operationally, the economics of aerial inspections are now a central part of procurement conversations. Field implementations routinely demonstrate steep reductions in time-on-task and meaningful operational cost savings compared with legacy access methods. For buyers, this translates into smaller inspection windows, reduced exposure to hazardous access work, and the ability to move from scheduled checks to condition-based monitoring driven by higher-frequency aerial data.

Based on our analysis, executive actions for 2026 fall into three pragmatic horizons:

Given modest market concentration, acquirers can find attractive bolt-on targets: platform providers that can be vertically integrated into existing enterprise software suites, regional operators with regulatory approvals in growth markets, and analytics specialists that can accelerate AI-driven insights. Our report includes a playbook for target screening and integration risk management to preserve service continuity and client relationships during M&A.

What distinguishes our research is the emphasis on executable intelligence. We synthesize market-level forecasts with vendor-level capabilities and translate those into procurement-ready materials and operational roadmaps. For C-suite stakeholders evaluating multi-year capital programs, the report reduces uncertainty by coupling scenario-based market projections with prescriptive implementation steps and real-world vendor scorecards.

For leaders preparing 2026 budgets, the report is a strategic tool to: prioritize pilot investments, design supplier consolidation strategies, and align regulatory engagement with operational readiness. The full document contains the supporting appendices — including supplier scorecards, detailed cost-model templates, and segment-level tables — that will be indispensable for procurement, operations, and risk teams. We intentionally refrain from reproducing those proprietary segment tables here to preserve the analytic integrity of the report and to encourage direct engagement with our full dataset.

To access the complete analysis, including the appendices and vendor benchmarking datasets, please consult PW Consulting’s full Aerial Inspections Service Market report. The packaged intelligence will enable you to move from strategic intent to operational execution with confidence in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Aerial Inspections Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com