https://www.facebook.com/PolorVisionDrivingGlasses2026

Art |

2026-06-21 11:31:24

PW Consulting’s latest market study on Low Salted Sodium Hypochlorite synthesizes primary sourcing, manufacturing innovation, regulatory signals, and end‑market dynamics to create a practical decision framework for executives entering 2026. The global market — measured across 2020–2025 history and modeled through 2026–2032 — shows resilient expansion, with total revenues rising from the mid‑hundreds of USD millions in the mid‑2020s and projected to grow at a compound annual growth rate (CAGR) of 5.29% through the forecast window. Our scenario baseline places the market at approximately USD 648.5 Million in 2025, expanding to roughly USD 706.1 Million in 2026 and trending toward a near‑billion dollar opportunity by 2032 under the central case. This briefing highlights how that macro trajectory should shape boardroom priorities, procurement strategies, and technology roadmaps in 2026 — while intentionally holding back detailed subsegment figures to encourage direct engagement with the full report for transaction‑critical numbers.

Low Salted Sodium Hypochlorite Market

Timing and scale: With steady mid‑single digit CAGR and a clear near‑term uplift in total market value between 2025 and 2026, 2026 is a window for both capacity investments and commercial repositioning that can capture disproportionate share as higher‑purity and high‑strength chemistry adoption accelerates.

Low Salted Sodium Hypochlorite Market

Technology inflection: Advances in multi‑stage chlorination, filtration to sub‑micron levels, and salt‑removal processing are changing unit economics for municipal and industrial buyers. These developments translate into lower usage rates, extended shelf life, and reduced downstream equipment wear — attributes that matter in procurement conversations this year.

Low Salted Sodium Hypochlorite Market

Regulatory and certification momentum: Certification pathways (national water association standards and laboratory certifications) are increasingly a gating factor for specification in public water systems and critical food & pharma water uses. 2026 will be a year when certified, low‑impurity grades gain preferential procurement treatment.

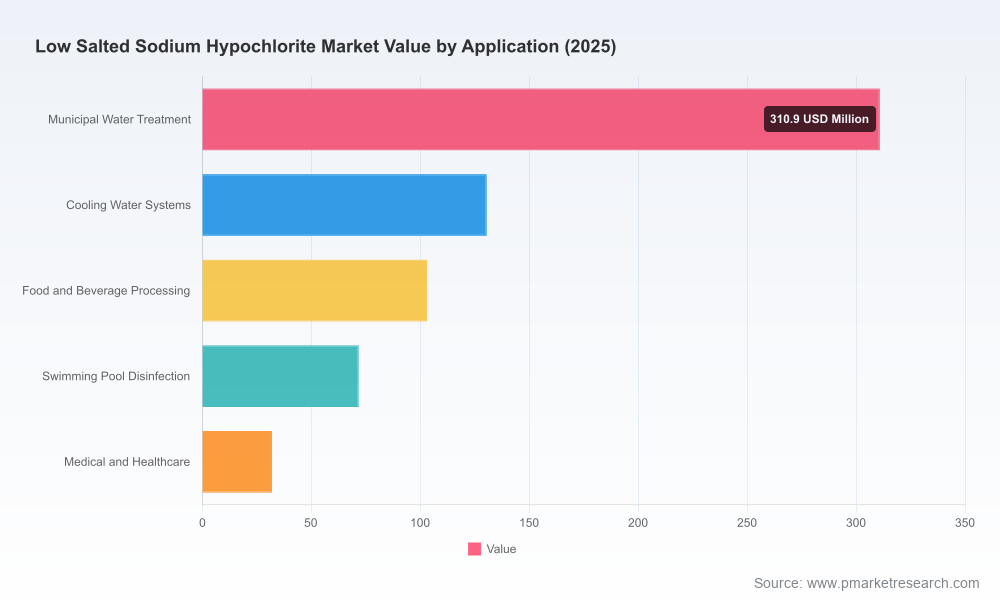

Demand drivers: Municipal water treatment, industrial cooling systems, food & beverage processing, pools, and healthcare disinfection continue to anchor demand. However, we observe an incremental shift toward higher‑purity, high‑strength product variants where lifecycle and operational cost advantages are demonstrable.

Supply and concentration: Market concentration is moderate — the leading three players account for a meaningful share, and the top five approach half of the market. This balance creates room for well‑capitalized incumbents to reinforce positions while offering differentiated niche suppliers pathways to scale through technical specialization.

Production & on‑site alternatives: Two parallel manufacturing trends are in play — centralized high‑concentration, low‑salt production with advanced purification, and decentralized on‑site generation systems that reduce transport and storage risk. Buyers in 2026 will evaluate these not as binary choices but as blended strategies to minimize total cost of ownership.

Performance economics: Recent field validations demonstrate material operational savings from high‑strength low‑salt grades, including significant reductions in usage volumes and improved performance consistency versus conventional formulations. These operational delta metrics are becoming the primary justification for premium pricing models.

Our competitive review covers established chlor‑alkali integrators and specialty chemical players that have positioned low‑salt sodium hypochlorite as a core offering. Rather than rank by reported subsegment revenues here, we summarize strategic postures and implications for buyers, partners, and acquirers.

Kuehne Company — A private producer with concentrated low‑salt formulations focusing on water treatment and disinfection. Their positioning emphasizes product stability and long‑term municipal customer relationships. For purchasers, Kuehne exemplifies the stable, relationship‑driven supplier model; for investors, it illustrates how private, specialized producers capture defense‑grade contracts.

HASA Inc. — Market leader in premium high‑strength low‑salt variants, including 15.5 wt% formulations filtered to sub‑micron levels and certified to applicable water safety standards. Recent trial data indicate meaningful operational benefits (for example, a recorded reduction in usage volume during a municipal wastewater trial), signaling that validated field performance can accelerate specification upgrades in municipal procurement frameworks.

Olin Corporation — As an integrated chlor‑alkali player, Olin combines scale with proprietary processing that targets very high percent NaOCl formulations and low impurity profiles. Their stewardship and handling documentation released recently underscore a strategic emphasis on enabling higher‑concentration product adoption while managing logistics and safety risks.

Shin‑Etsu Chemical and Kaneka Corporation — These Japanese incumbents emphasize certified grades tailored to tap water sterilization and food production uses, leveraging certifications and low‑impurity claims to access regulated procurement channels. Their presence illustrates the premium value of certification and localized standards compliance for public utilities and food/pharma customers.

Procurement transformation: Move from unit‑price procurement to total‑cost‑of‑use contracts. Incorporate usage efficiency metrics, shelf‑life assumptions, and equipment maintenance offsets into supplier scorecards. Validate performance claims with short, instrumented pilots — the signal‑to‑noise from well‑executed trials is high.

Capacity & M&A positioning: For producers, the path to mid‑term growth is twofold — expand technical capacity for high‑purity, high‑strength product lines and pursue regional capabilities that reduce logistic friction. For strategic buyers, target assets that combine purification know‑how with secure feedstock sources.

Product innovation & certification: Invest in certification and robust quality documentation as market access enablers. Certification to national water standards and third‑party lab validation will be decisive in public tenders and food/pharma contracts.

Hybrid supply models: Evaluate blended procurement (centralized delivery for base loads, on‑site generation for peak or remote needs). Structure contracts to allow operational switching and to monetize savings earned from lower usage and reduced transport risk.

Risk and resilience: Build contingency plans for raw material and logistics disruptions, and stress‑test contracts for impurity tolerance. Consider offtake or strategic supply agreements with processor partners to secure continuity in the event of spot market tightness.

Run a three‑month pilot with a high‑strength low‑salt supplier, instrumenting dosage, residuals, equipment wear markers, and labor hours to quantify lifecycle benefits.

Update procurement RFIs/RFPs to include purity, certification, and validated usage reduction metrics — not just concentration and price per unit.

Audit existing on‑site generation economics versus delivered product for each major facility, including freight, storage, insurance, and safety compliance costs.

Embed supplier stewardship and handling requirements into capital projects and operations manuals to reduce implementation friction and to accelerate approvals.

This study is built to be directly actionable. Highlights of the full report include:

Detailed market sizing and forward scenarios with transparent assumptions for macro and micro drivers across the 2026–2032 forecast horizon.

Segment‑level demand analysis (by region, product grade, and application), with scenario bands to stress‑test investment cases — note: the preview above intentionally omits those granular numbers to preserve the value of the full dataset.

Technology deep dives describing two‑stage chlorination, salt‑removal and filtration approaches, and on‑site generation economics — including sensitivity models you can adopt to assess vendor claims.

Supplier profiles and a competitive positioning map, with playbooks for partnering, contracting, and M&A targets.

Procurement templates and pilot design checklists to accelerate validation and specification changes within utilities and industrial customers.

Certification barriers: Certification and local water authority approvals can delay specification changes; plan at least one procurement cycle for adoption in regulated public tenders.

Technical trade‑offs: Higher concentration delivers lower transport volumes and usage but increases handling complexity; investments in safety and training are non‑negotiable.

Substitution risk: On‑site generation technologies continue to improve; producers must articulate service‑based offerings or technical differentiators to maintain relevance.

2026 presents an inflection moment for buyers and producers in the Low Salted Sodium Hypochlorite market. The macro trajectory is clear — a market expanding at roughly a mid‑single digit CAGR with a growing premium segment for high‑purity, high‑strength products. Executives should treat 2026 as the year to operationalize total‑cost‑of‑ownership procurement, validate high‑strength formulations via short pilots, and align product development with certification pathways to secure access to regulated tenders. For producers and investors, opportunities exist to scale specialized technical capabilities or to consolidate via targeted M&A that combines purification expertise with geographic reach.

PW Consulting’s full report contains the detailed subsegment figures, scenario models, and procurement tools needed to convert these strategic imperatives into executable plans. Access the complete dataset and downloadable playbooks on our report page to underpin your 2026 strategy with the granular evidence required for capital allocation, supplier negotiations, and operational rollout.

For detailed analysis of this topic, please visit the official page:Low Salted Sodium Hypochlorite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com