Lip Fillers Injections in Dubai for Youthful, Soft, and Naturally Fuller Lips

Health |

2026-06-18 09:21:32

As global supply chains enter a new phase of automation and software-driven orchestration, PW Consulting today publishes an executive briefing drawn from our forthcoming Intelligent Automatic Warehouse And Logistic Equipment Market report. The market is entering a period of accelerated scale: having reached roughly USD 35.6 billion in 2025, our model projects expansion to nearly USD 78.8 billion by 2032, driven by a 12.04% compound annual growth rate across the 2026–2032 forecast window. For executives planning capital allocation, technology roadmaps, or M&A activity in 2026, the choices made this year will materially determine cost structure, service capability, and competitive positioning through the next decade.

Intelligent Automatic Warehouse And Logistic Equipment Market

Several converging forces elevate 2026 from a routine planning horizon to a strategic inflection point for warehouse automation: persistent labor shortages and rising logistics wages have converted what were once productivity investments into necessity moves to preserve throughput; energy-efficiency and ESG mandates in North America and Europe make regenerative drives and low-energy system architectures a procurement priority; and trade policy and commodity dynamics — including elevated steel and aluminum pricing and tariff changes — are reshaping total installed cost and supplier selection strategies.

Intelligent Automatic Warehouse And Logistic Equipment Market

These dynamics mean procurement teams must balance three often-conflicting objectives: speed-to-automation, total cost of ownership (TCO) resilience, and future-proof flexibility. Companies that treat 2026 as a moment for tactical pilots only risk losing multi-year advantages to first movers who align CapEx timing with software-enabled scalability.

Intelligent Automatic Warehouse And Logistic Equipment Market

The market remains characterized by rapid innovation and pronounced fragmentation. Our concentration analysis indicates that leading vendors do not dominate the space to the extent seen in adjacent industrial segments; top-three vendors account for less than one-fifth of the addressable market, and top-five players represent slightly more than one-quarter. This creates fertile opportunity for both niche innovators and systems integrators that can bundle hardware, software, and lifecycle services.

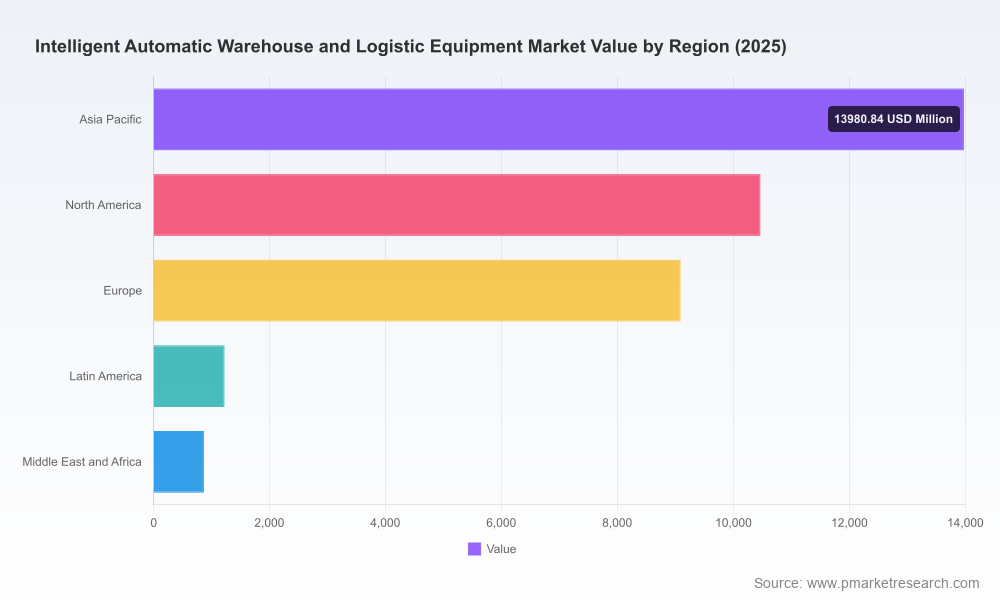

Geographically, adoption intensity varies by region — developed e-commerce and industrial markets continue to drive the largest absolute demand, while high-growth pockets in emerging markets present attractive greenfield opportunities for modular, lower-capex architectures. On the demand side, e-commerce and retail remain primary adopters, followed by food & beverage, automotive, healthcare/pharma, and general manufacturing. Technologies in demand include high-density AS/RS, AMRs/AGVs for flexible pick-and-move operations, integrated sortation and conveyor systems for high-throughput nodes, and warehouse management/execution software as the integration layer.

Importantly, product architecture decisions are increasingly determined by software strategy: openness, API maturity, and multi-vendor orchestration capabilities — not hardware specifications alone — are the principal differentiators for enterprise-scale implementations.

The competitive arena blends long-established systems houses and newer robotics-first entrants. Below are the strategic profiles that informed our vendor benchmarking and partner-selection frameworks:

Recent industry events — notably MODEX 2026 and Automate-related conferences — reinforced two themes: vendors are converging on software-defined automation stacks, and interoperability is the new battleground. KNAPP’s recent commentary on multi-agent robotic systems points to a rapid maturity curve in collaborative intelligence for fleets, while trade shows showcased integrations that bring AS/RS, shuttles, AMRs, and WES closer together operationally.

Our full report converts market intelligence into executable strategy. We blend proprietary demand-modeling, vendor-grade technical matrices, and pragmatic procurement tools to deliver not just “what” is happening, but “how” to capitalize. Clients receive: interactive scenario dashboards, vendor negotiation playbooks, implementation phasing guides, and a library of KPIs mapped to contract milestones. The briefing you are reading highlights the strategic contours; the full report contains the granular segmentation, regional breakdowns, supplier-level benchmarks, and the raw datasets necessary for procurement and investment committees to act decisively.

Note: in keeping with our briefing approach, this release intentionally omits the detailed subsegment tables and exact regional/applications splits — those core intelligence assets are included in the report package and the supporting data set available on our website.

For supply chain executives, CIOs, and private equity sponsors preparing budgets and M&A pipelines for 2026, PW Consulting’s Intelligent Automatic Warehouse And Logistic Equipment Market report is designed as a decision-enabling resource. Visit our report page to access the full dataset, vendor scorecards, and bespoke advisory services that translate these market dynamics into a 24–36 month action plan tailored to your operations.

PW Consulting — Strategic clarity at the intersection of capital allocation, technology adoption, and operational execution.

For detailed analysis of this topic, please visit the official page:Intelligent Automatic Warehouse And Logistic Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com