Overview of Signing Services Of America in the United States

Other |

2026-05-27 05:06:31

PW Consulting’s new market study on Patient Record Management (base year 2025; historical window 2020–2025; forecast 2026–2032) delivers a focused, decision-ready view for executives planning investments, procurement, or competitive moves in 2026. The global patient record management landscape has expanded steadily—from a multi‑billion dollar market in 2020 to an estimated USD 41,691.72 Million in 2025—and is projected to reach approximately USD 64,362.93 Million by 2032, growing at a compound annual growth rate (CAGR) of 6.41% over the 2026–2032 forecast horizon. This briefing highlights the report’s strategic value, the dynamics shaping vendor and buyer behavior, and the practical levers organizations must prioritize next year. As a trailer to the full report, we deliberately surface high‑value insights while reserving detailed segment tables and region/application breakdowns for the full download.

Patient Record Management Market

Actionable market sizing and trajectory: The study reconciles historical performance (2020–2025) with forward scenarios for 2026–2032 to help boards and investment committees set realistic revenue and adoption targets.

Patient Record Management Market

Decision‑grade vendor intelligence: Comparative vendor scorecards, product roadmaps, and integration readiness assessments enable CIOs and procurement teams to narrow vendor shortlists efficiently.

Patient Record Management Market

Implementation playbooks and TCO models: Practical cost, timeline, and risk templates allow health systems and ISVs to stress‑test plans before committing capital or signing enterprise contracts.

Regulatory and standards impact analysis: We translate HITECH, ONC/Cures requirements, CMS incentives, and the arrival of HL7 FHIR Release 5 into concrete compliance actions and procurement clauses.

M&A and partnership heuristics: Given the market concentration profile, the report outlines where M&A or strategic alliances can unlock scale or technical differentiation.

Three structural trends are driving the market’s steady growth and will be particularly material in 2026.

Cloud migration and consumption model shifts: Providers continue migrating toward cloud‑centric deployments for scalability and operational flexibility. Buyers are demanding outcomes—reduced integration burden, better uptime SLAs, and pay‑as‑you‑grow pricing—forcing vendors to refine managed service and SaaS offerings.

Interoperability and standards acceleration: With HL7 FHIR Release 5 consolidating API expectations and ONC rules constraining information blocking, interoperability is no longer aspirational; it is a procurement requirement. Vendors that demonstrate clean FHIR‑first architectures and documented API performance will enjoy faster wins in 2026.

Embedded analytics and AI: The shift from records as repositories toward records as intelligent, summarized clinical assets is underway. Recent product releases (notably AI‑powered summarization capabilities) signal that buyers will prize solutions that reduce clinician cognitive load, improve care transitions, and generate actionable insights without increasing documentation burden.

The market shows meaningful concentration—our CR3 is approximately 42.2% and CR5 near 58.4%—indicating a mix of incumbent dominance and an active tier of challengers. This structure shapes competitive tactics and procurement outcomes in the following ways:

Incumbents maintain leverage over large health systems through deep clinical workflows, long‑standing integrations, and scale economies. Their strategic playbooks emphasize platform extensibility, enterprise analytics, and partnerships with hyperscalers for advanced compute and AI services.

Mid‑market specialists and cloud natives are winning greenfield accounts and specialty practices by offering faster deployments, lower upfront costs, and more flexible integration patterns. These vendors pair EHR capabilities with modular services—telehealth, patient engagement, and revenue cycle management—to create horizontal sticks.

Strategic partnerships are accelerating: examples include alliances between EHR vendors and major cloud providers to deliver managed analytics and machine learning capabilities; such arrangements materially alter TCO, innovation velocity, and data governance options for buyers.

Key vendor signals (non‑exhaustive, recent events): Epic introduced AI‑driven record summarization enhancements in late 2025; a leading incumbent announced a cloud partnership with a hyperscaler for advanced analytics and machine learning; and another platform achieved updated ONC certification this year. These moves underscore three tactical imperatives for 2026: certify and test your EHR flows against the latest regulatory matrix, validate AI features in pilot settings before enterprise roll‑out, and renegotiate cloud SLAs with a precise view on data egress, residency, and auditability.

Top‑line market model: historical reconciliation (2020–2025) and scenario‑based forecasts (2026–2032), with sensitivity bands and assumptions documented for financial committees.

Vendor scorecards: standardized metrics for clinical functionality, interoperability, deployment flexibility, security, and total cost of ownership—designed for procurement shortlisting and RFP weighting.

Buyer’s decision framework: 12‑step roadmap covering procurement cadence, pilot design, change management, clinician adoption KPIs, and post‑implementation optimization.

Integration and data governance toolkit: sample contractual language, API performance SLAs, and audit templates aligned to FHIR Release 5 and ONC expectations.

Risk and value playbooks: migration risk matrices, incremental value capture templates, and payer/provider shared savings scenarios calibrated to real world examples.

Primary research appendix: synthesis of interviews with CIOs, CMIOs, vendor product leads, and payers, plus a description of quantitative model inputs and validation checks.

For hospital and health system executives: Prioritize integration hygiene and API budgets. Treat interoperability readiness as capital investment—reserve funds for API testing, mapping, and controlled pilots of AI summarization to protect clinician throughput.

For vendor leadership: Differentiate on implementation velocity and managed outcomes. Build packaged vertical templates (cardiology, oncology, ambulatory specialties) and partner with cloud providers to offer validated ML pipelines and compliance controls.

For payers and health IT investors: Focus on predictable recurring revenue models and platform extensibility. Look for assets with proven FHIR integration patterns and documented clinician adoption improvements—these underpin valuation multiples in 2026 rapprochement deals.

For procurement teams: Update RFP scoring to weigh (a) API conformance to FHIR Release 5, (b) documented AI explainability and clinician validation kits, and (c) data portability clauses ensuring exit options and patient access continuity.

For policymakers and regulators: Balance certification guardrails with sandbox pathways for AI features; practical safety testing protocols will accelerate beneficial innovation while reducing downstream compliance friction.

Our study combines a market‑grade financial model (reconciling historical revenue trends with scenario forecasting), granular vendor benchmarking, and practical operational tools designed for immediate uptake by practitioners. Rather than producing a static excel dump, PW Consulting’s deliverables include executable implementation playbooks and negotiation artifacts that procurement and clinical teams can apply in the first 90–180 days following purchase decisions.

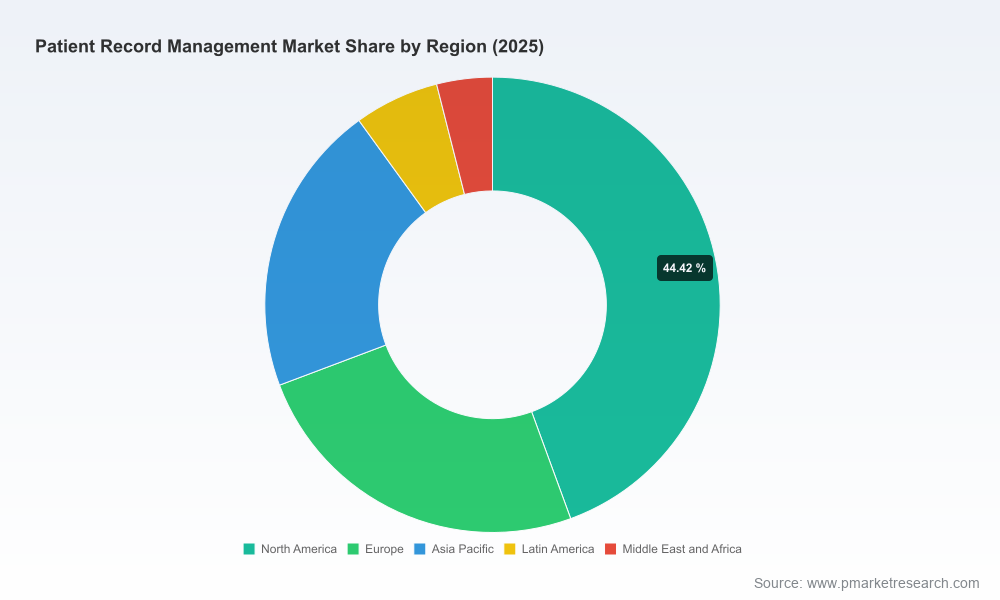

In line with the “trailer” purpose of this release, we surface headline market sizing, growth trajectory, concentration metrics, and high‑impact qualitative conclusions, while reserving detailed segmentation breakdowns, region/application percentage shares, and granular revenue-by‑deployment data for the full report. These segmented tables and interactive dashboards are essential for transaction due diligence and strategic procurement and are available via the PW Consulting report portal.

Download the full PW Consulting Patient Record Management report to access the vendor scorecards, downloadable TCO templates, and the interactive market model.

Request a tailored briefing for your organization—our analysts can map the report’s findings to your operating model and produce a 90‑day action plan for vendor selection, pilot design, or M&A screening.

Book a workshop on FHIR Release 5 readiness and AI validation: a half‑day session that aligns clinical, legal, and IT stakeholders around a single execution roadmap.

In an environment where regulation, standards, and technology are converging—yet buyer expectations and clinical realities remain complex—this report equips leaders with both a clear market map and the operational tools to capture value. PW Consulting’s Patient Record Management market study is designed to be the strategic companion for every decision maker preparing to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Patient Record Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com