Mobile Games Market Size, Share, Gaming Industry Trends and Forecast by 2029

Other |

2026-05-13 12:07:47

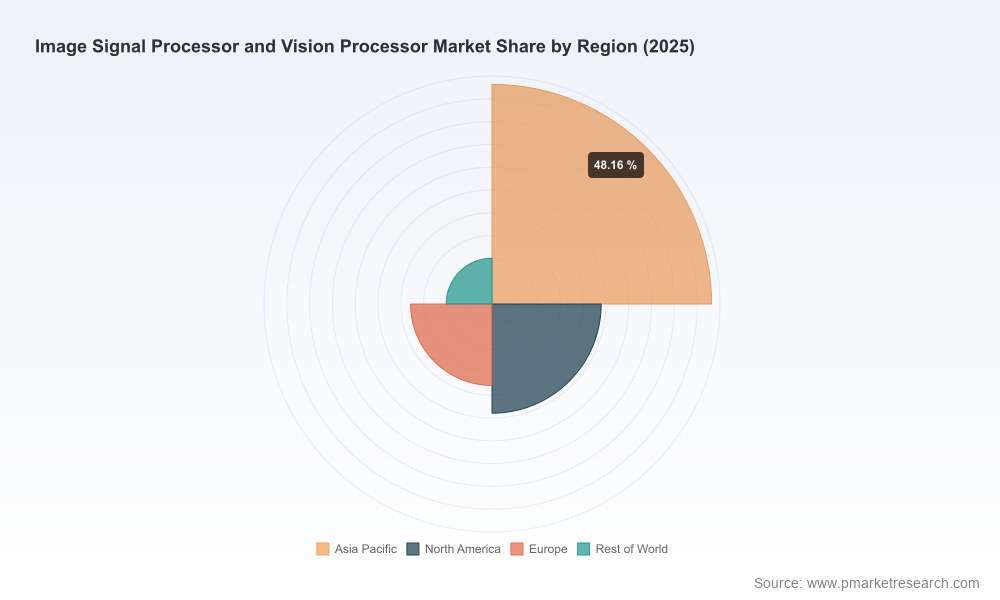

As demand for smarter, sensor-driven systems accelerates, the Image Signal Processor (ISP) and Vision Processor market is entering a new phase of structural growth and strategic reorientation. PW Consulting’s latest market study shows the industry expanding from roughly USD 3.85 billion in 2020 to about USD 5.8 billion in 2025, and we forecast an ascent to approximately USD 10.7 billion by 2032 — reflecting a compounded annual growth rate of 9.16% over the 2026–2032 projection window. These headline figures understate the rate of technology churn: edge AI integration, software-defined imaging, and system-level consolidation are reshaping supplier economics, OEM architectures, and channel dynamics.

Image Signal Processor And Vision Processor Market

Investment timing — Capital and R&D allocation timed to the 2026–2028 inflection will determine who secures first-mover advantages around 8K multi-stream processing, multi-sensor fusion, and on-chip AI acceleration.

Image Signal Processor And Vision Processor Market

Architecture bets — Choices between integrated SoC solutions versus modular ISP/vision-processor stacks will drive product roadmaps, qualification cycles, and margin profiles across automotive, industrial, and security end-markets.

Image Signal Processor And Vision Processor Market

Supply-chain resilience — Geopolitical and materials risks demand proactive sourcing and design-for-manufacturability strategies to avoid costly production interruptions and missed design wins.

The headline growth trajectory — mid‑single-digit to high‑single-digit CAGR approaching double‑digit growth over the forecast period — is powered by multiple, overlapping tailwinds: proliferation of multi-camera systems in automotive ADAS and cockpit sensing, uplift in edge analytics for security and industrial automation, and a secular upgrade cycle in consumer imaging for premium devices. Beneath these aggregates lie rapid shifts in product function and value capture. Vendors are moving from pure ISP pipelines to hybrid vision SoCs that combine best-in-class noise reduction, HDR imaging, and learned, on-device neural processing. This creates winner-take-most dynamics around software ecosystems, IP licensing, and strategic alliances.

The market is dominated by a mix of established semiconductor houses and specialized vision-IP firms. Our qualitative assessment highlights three strategic archetypes:

Integrated SoC leaders: firms delivering end-to-end edge AI vision platforms that embed ISPs inside broader compute fabrics and AI accelerators. Recent product introductions show this category accelerating toward higher process nodes and multi-stream video capabilities.

Complementary ISP suppliers: companies that focus on companion ISPs or ISP IP cores, optimized for sensor pairing and specific use-cases such as surround view or low-light enhancement. These players compete on latency, power, and image-quality pipelines rather than pure compute throughput.

Platform and ecosystem players: vendors tying ISPs and vision processors into software stacks, developer tools, and OEM partnerships to lock in long-term design wins and recurring revenue streams.

Recent commercial activity reinforces these archetypes. Leading edge announcements include a next‑generation edge AI vision SoC on advanced process nodes that targets simultaneous 8K multi-stream processing for security and automotive applications, demonstration of the industry’s first full AI-based ISP pipeline that promises software-defined real-time video enhancement, and high-throughput vision processors designed for concurrent multi-sensor ADAS workloads. These product moves underscore how compute, node migration, and software-defined imaging are converging to redefine competitive advantage.

Two interlinked trends will shape vendor and OEM strategy in 2026:

Policy and trade interventions — Recent tariff and export-control measures targeting advanced computing and processed critical minerals elevate the cost of cross-border supply and complicate market access to high-performance processors. Licensing requirements and security reviews for certain high-end vision chips are increasing program risk for suppliers dependent on global distribution models.

Component lead times and material concentration — Semiconductor lead times for select IC families have lengthened into multi-quarter ranges amid renewed AI-driven demand, and processed critical minerals face heightened import scrutiny. These dynamics favor firms with diversified qualified suppliers, forward-buy practices, and the willingness to localize manufacturing for strategic customers.

For OEMs and Tier‑1 suppliers, the implications are immediate: product qualification timelines must incorporate contingency for extended lead times; contractual terms need clauses for supply disruption; and sourcing strategies must account for potential tariff exposure or export restrictions that could affect cost competitiveness and time-to-market.

Automotive and ADAS — The automotive market will continue to demand deterministic performance, functional safety, and predictable long-term supply. Suppliers that can combine automotive-grade ISPs with on-chip vision AI and proven software stacks will be prioritized. Firms already reporting heavy automotive exposure illustrate how supplier revenue mixes can hinge on a small number of verticals, increasing the importance of diversified end-markets or exclusive partnerships.

Security & Surveillance — Cost-performance and developer ecosystems matter most here. The rise of multi-stream, high-resolution analytics at the edge is creating opportunity for solution providers able to deliver scalable software-defined pipelines and managed update mechanisms across installed bases.

Industrial & Robotics — Deterministic latency, hard real-time performance, and environmental robustness are differentiators. Vision processors that can be certified for industrial standards and integrated into robotics middleware will capture a disproportionate share of system value.

PW Consulting’s research translates analysis into a pragmatic set of actions that leadership teams should consider this year:

Prioritize modularity in architecture choices — Preserve optionality by designing reference platforms that can accept either integrated SoCs or dedicated ISP/vision modules; this reduces future requalification costs and accelerates OEM adoption.

Invest in software-defined imaging — OEMs and suppliers should accelerate development of firmware and AI enhancement suites that can be updated post-deployment to monetize continuous feature upgrades and reduce hardware obsolescence risk.

Harden supply-chain playbooks — Establish dual-sourcing for critical components, institute strategic inventory buffers for long‑lead items, and assess near-shore manufacturing or qualification to mitigate tariff and export-control risk.

Forge ecosystem partnerships — Pursue alliances with sensor manufacturers, AI-stack providers, and systems integrators to shorten time-to-market and build defensible solution bundles that raise switching costs.

Adopt scenario-based planning — Use our provided scenario matrices to stress-test product roadmaps against tariff escalations, process-node access limitations, and accelerated adoption curves in key end-markets.

The study combines quantitative forecasting with operationally focused deliverables designed to inform board-level and product-team decisions in 2026:

Market sizing and forecast models with sensitivity analysis across multiple adoption curves and process-node scenarios.

Competitive benchmarking and supplier scorecards that evaluate technical differentiation, software ecosystems, go-to-market agility, and supply-chain resilience.

Commercial playbooks for OEMs, Tier‑1s, and fabless vendors including negotiation levers, qualification templates, and cost-to-serve calculators.

Scenario planning templates addressing regulatory shocks, export-control constraints, and materials shortages, with recommended contingency actions and P&L impact modeling.

Deal and M&A heatmap identifying strategic targets for capability acquisition, vertical integration, or partnership to accelerate in-house imaging and vision competencies.

Executives and product leaders can use our report as both a diagnostic and an operational playbook. Recommended immediate steps are:

Run rapid ‘stress tests’ of your 2026 roadmaps against our lead-time and tariff scenarios; adjust BOM and qualification timelines where necessary.

Map existing supplier relationships to the competitive archetypes in the report and identify one supplier to deepen (strategic), one to diversify (risk mitigation), and one to displace (cost or capability).

Allocate a portion of R&D to software-defined imaging capabilities to extend product lifecycles and create recurring software monetization paths.

The ISP and vision processor market presents a rare combination of steady demand growth and rapid technological transformation. While headline market value is set to nearly double over the next decade, the strategic contests of 2026 will be decided by companies that translate technical differentiation into ecosystem lock-in, mitigate geopolitical and supply risks, and monetize software-enabled functionality. PW Consulting’s report equips decision-makers with the market context, supplier intelligence, and practical playbooks necessary to make those choices with confidence.

For a detailed breakdown of competitive positions, scenario model inputs, supplier scorecards, and the proprietary data tables that underpin our forecasts, please consult the full Image Signal Processor And Vision Processor Market report on the PW Consulting website. The public release is intentionally selective — our strategic aim is to provide you with the diagnostic framework and operational tools now, while reserving the granular segment-level data and model access for report subscribers and clients who want to operationalize these insights.

For detailed analysis of this topic, please visit the official page:Image Signal Processor And Vision Processor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com