Primary Cell Media Market 2026 Strategic Brief: What Every Executive Must Know

PW Consulting releases an advance strategic brief drawn from our forthcoming Primary Cell Media Market report — a decision-grade resource designed to orient commercial, procurement, R&D and M&A choices in 2026. This brief highlights the report’s core macrotakeaways, competitive dynamics, and actionable playbooks while intentionally withholding the granular regional and application splits reserved for the full report. Our goal: give senior leaders a clear line of sight to the opportunities and risks shaping the primary cell media landscape next year, and show why the complete dataset and playbooks in the full report are essential for precise execution.

Primary Cell Media Market

Market snapshot: scale, trajectory, and why it matters for 2026

The global primary cell media market has moved from a niche research category into a commercially strategic product class. Our base-year analysis shows a market that expanded from roughly USD 675 million in 2020 to about USD 1,050 million in 2025. The market is forecast to continue robust growth through our projection window (2026–2032) at a compound annual growth rate (CAGR) of 9.25%, reaching roughly USD 1,950 million by 2032. This trajectory reflects durable demand from drug discovery, regenerative medicine and core research laboratories, and it signals a structural shift: primary cell media are now a vector for value capture across life-science supply chains.

Primary Cell Media Market

Why 2026 is an inflection year

- Commercialization of advanced cell- and tissue-based therapies is moving R&D-use products closer to clinical-grade expectations, raising buyer requirements for traceability, consistency and regulatory documentation.

- Adoption of chemically defined and low-/serum-free formulations is accelerating as labs prioritize reproducibility and scalability, creating differentiation opportunities for suppliers that can combine formulation expertise with robust quality systems.

- Supply-chain resilience and raw-material sourcing (including amino acids, growth factors and plant-derived hydrolysates) are emerging as strategic procurement topics rather than routine operational concerns.

- Competitive dynamics are consolidating around a mix of global platform vendors and specialized niche manufacturers; the market shows moderate concentration, leaving room for both scale plays and focused specialist strategies.

What the PW Consulting report delivers — practical, operational, ready-to-act

We designed the full Primary Cell Media Market report to be a hands-on toolkit for 2026 planning cycles. Highlights include:

Primary Cell Media Market

- Proprietary market model and scenario engine — baseline and downside/upside scenarios with sensitivity to pricing, adoption of serum-free media, and shifts in research funding.

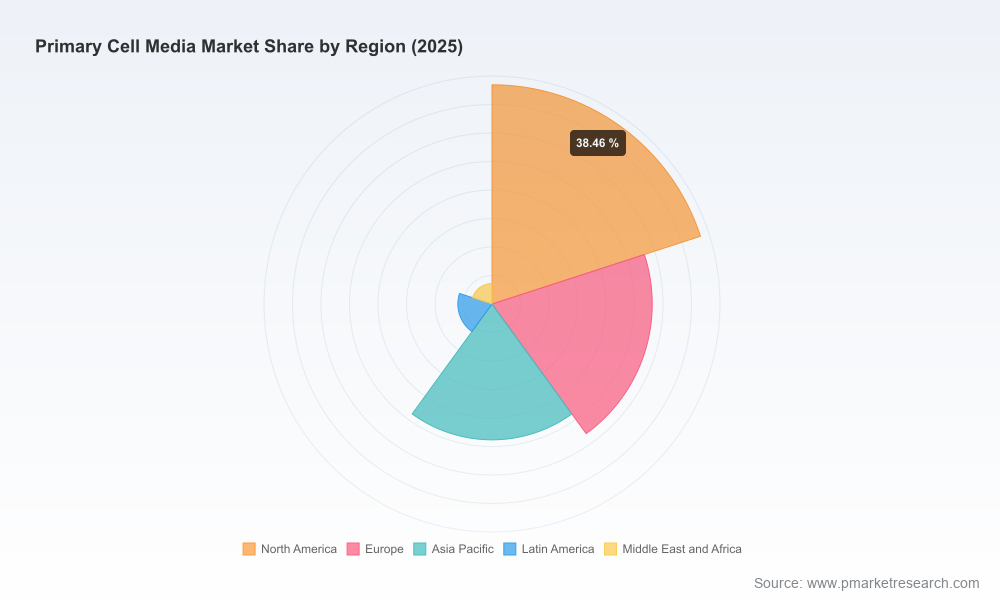

- Executive-ready dashboards — concise slices for C-suite briefing, investment committees and commercial planning teams (regional and application splits available in the full report).

- Supplier scorecards and capability mapping — assessment of 12+ vendors on formulation breadth, regulatory readiness, manufacturing footprint, and commercial support.

- Commercial playbooks — GTM tactics, channel mix recommendations, and pricing frameworks tailored to incumbent suppliers, new entrants and distributors.

- Procurement & raw-material risk matrix — lot-to-lot variability hotspots, single-source exposures, and mitigation strategies for critical inputs including growth factors and hydrolysates.

- Regulatory and quality compendium — practical checklists for upgrading research-use media to meet clinical supporting activities and translational research requirements.

- M&A and partnership heatmaps — prioritized targets and partnership archetypes aligned to strategic goals (scale, capability, or niche depth).

- Implementation toolkits — negotiation templates, validation trial designs, and a 90-day action plan for immediate deployment.

Competitive landscape — who matters and how to read their moves

Our competitive analysis synthesizes product positioning, capability edges and likely strategic plays among the leading vendors. The market is anchored by legacy life-science platforms and specialized media houses. Top-tier suppliers combine formulation IP with global distribution and strong technical services; niche players compete on tissue specificity, customer intimacy and bespoke formulations.

- Thermo Fisher Scientific (Gibco) remains the default scale player with broad formulation libraries and extensive technical support infrastructure — a natural go-to for buyers prioritizing portfolio completeness and global service.

- Merck KGaA (MilliporeSigma) leverages integrated reagent portfolios and kit-based offerings that simplify lab workflows — a strong position for customers seeking turnkey solutions.

- Lonza Group’s strengths sit at the intersection of research and bioprocessing, offering tissue-specific formats and a pathway to scale for suppliers and biotech customers pursuing translational programs.

- Corning leverages its consumable footprint to bundle media with hardware and protocols, nudging procurement toward integrated solutions where reproducibility is sold as part of the system.

- Specialists such as PromoCell, FUJIFILM Irvine Scientific, and STEMCELL Technologies differentiate through tissue-specific or chemically defined media and high-touch customer service that supports demanding primary cell types.

- A broader cohort of niche manufacturers and distributors remains important for localized channels, custom formulations and competitive pricing — serving as acquisition targets or strategic partners for platform players.

Market concentration metrics point to a competitive structure where the top three players control a meaningful, but not overwhelming, portion of value — creating room for both focused scale-ups and value-adding niche plays. The precise regional and application-level dynamics that inform market entry or expansion priorities are detailed in the full report.

Raw-material & regulatory realities that will shape supplier economics in 2026

Primary cell media formulations depend on a complex bill of materials: basal media components (amino acids such as L-alanyl-L-glutamine, L-arginine), vitamins, salts and energy sources, often supplemented with growth factors, cytokines and low percentages of serum or alternatives. Plant-derived hydrolysates (e.g., wheat hydrolysate) are common supplements used to provide peptides and amino acids; these inputs can introduce batch variability unless tightly controlled.

Quality and traceability expectations are rising. Research-use products are now routinely evaluated against standards that emphasize compositional consistency and supply-chain transparency. For organizations considering an upgrade path into clinical-support applications, expect higher scrutiny of supplier quality systems, raw-material provenance and documented controls for lot-to-lot consistency.

Strategic imperatives for 2026 decision-makers

- Prioritize formulation differentiation: Invest in chemically defined and low-/serum-free media that reduce variability and simplify downstream translation. Action: accelerate R&D roadmaps and validation pilots with key accounts.

- Secure raw-material supply and quality: Establish multi-source agreements and audit critical suppliers (growth factors, hydrolysates). Action: implement a raw-material qualification program within 90 days.

- Upgrade quality infrastructure for translational opportunities: Map regulatory gaps between research-use and clinical-support supplies and budget for necessary QMS upgrades.

- Design service-led commercial propositions: Bundle media with validation kits, protocols and technical support to capture higher-margin, stickier relationships.

- Pursue targeted M&A or partnership plays: Use capability mapping to prioritize acquisitions that fill product gaps or extend distribution into priority geographies and channels.

- Calibrate channel strategy for reproducibility seekers: Leverage OEM and consumable partnerships to sell “system+media” solutions where reproducibility drives purchasing decisions.

- Embed scenario planning into 2026 budgets: Use the report’s scenario engine to stress-test revenue, margin and inventory plans against macro and supply volatility.

Next steps: how to convert insight into 90-day actions

For executives preparing 2026 plans, the choice is straightforward: leverage broad-stroke market intelligence to set ambition, then use operational, supplier-level analytics to prioritize execution. PW Consulting’s full report provides the granular regional and application splits, supplier scorecards, and commercial playbooks necessary to translate intent into measurable outcomes. If your team is preparing an FY-2026 commercial plan, procurement refresh, or M&A hunt, the full dataset and toolkits substantially reduce execution risk and accelerate time-to-value.

Contact PW Consulting to arrange a report briefing, a custom market deep-dive or a workshop that maps these strategic imperatives onto your organization’s capability and capital plans. The full report contains the granular splits, validated supplier metrics and executable templates that organizations need to make confident, defensible decisions in 2026.

For detailed analysis of this topic, please visit the official page:Primary Cell Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com