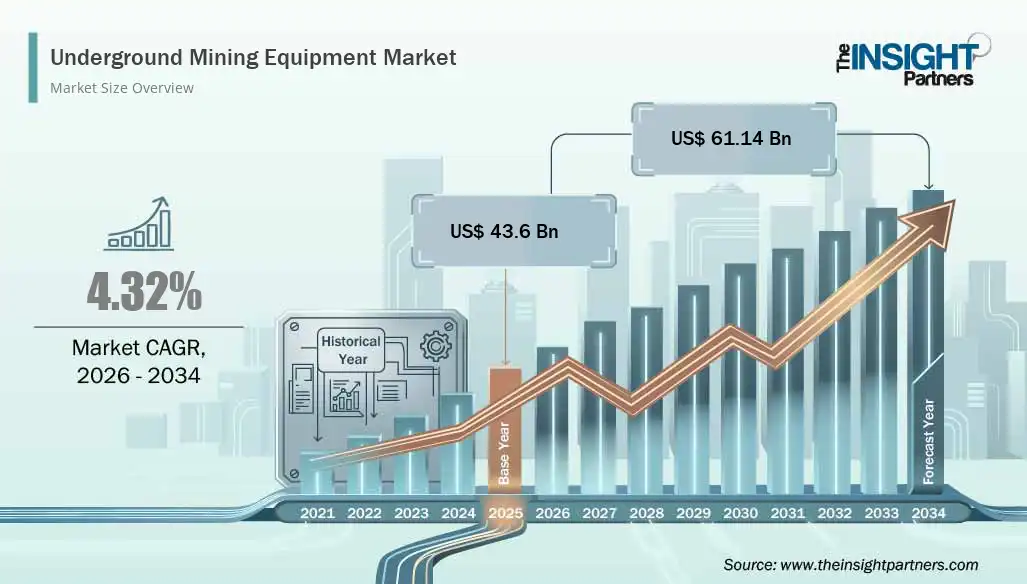

Underground Mining Equipment Market Size Worth USD 61.14 Billion Globally by 2034

Art |

2026-06-29 08:54:25

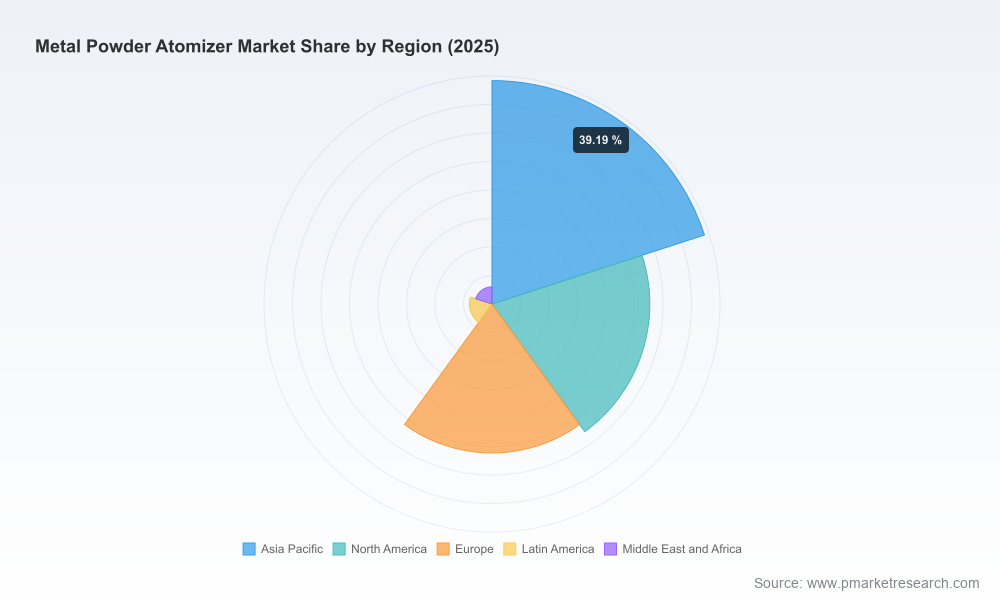

PW Consulting’s latest Metal Powder Atomizer Market report synthesizes five years of historical performance (2020–2025) and delivers a forward-looking, actionable roadmap for 2026–2032. The global market for metal powder atomizers demonstrated resilient growth through 2025, reaching a market size of approximately USD 673.4 Million in our base year. Our forecast anticipates continuation of this momentum, with a compound annual growth rate (CAGR) of 6.84% across the 2026–2032 horizon. This trajectory underlines expanding demand for high-quality metal powders across additive manufacturing, powder metallurgy and advanced coatings, and it reframes atomizer investments as strategic enablers rather than simple equipment purchases.

Metal Powder Atomizer Market

2026 will be a year of inflection for firms active in metal powders and their upstream equipment. Buyers, asset owners and investors must balance near-term capacity constraints and operating-cost pressures against longer-term demand gains and technology shifts. The PW Consulting report converts market-scale projections into decision-grade intelligence so that C-suite leaders can:

Metal Powder Atomizer Market

The market remains moderately fragmented: the three largest suppliers account for a material but not dominant share of industry revenue, and the top five move the market toward greater concentration without creating monopolistic barriers. Our proprietary concentration metrics show a CR3 of 34.2% and a CR5 of 48.65%, signaling an environment where leading engineering-specialist firms coexist with agile niche providers and new entrants.

Metal Powder Atomizer Market

Strategic implications: buyers enjoy supplier choice but must conduct rigorous vendor technical audits. For investors, consolidation through targeted M&A and capacity roll-ups remains a plausible near-term value-creation path—particularly for firms seeking to integrate atomization with powder processing and AM printing solutions.

Atomizer technology diversity is a defining feature of the market. Our report provides technology-level risk-reward maps that link process choice to downstream powder attributes, operating cost drivers and regulatory constraints. Key takeaways for 2026 planners include:

Operating expenses are as consequential as CAPEX in determining project economics. The report offers a granular view of the primary OPEX levers—energy, inert gases, consumables, and utilities—and models the impact of gas recirculation, water recycling and automation on cost per kilogram of powder. Notably, inert gases (argon, nitrogen) are a significant portion of gas-atomization operating costs; large-scale facilities that invest in recirculation or on-site generation can obtain meaningful unit-cost advantages.

Regulatory and safety constraints (for example, ATEX compliance for reactive metal production) also materially influence plant layout and capex. Our plant-level checklists for ATEX readiness and vacuum/inert-atmosphere control are designed to accelerate permitting and reduce time-to-first-production.

Our competitive analysis deep-dives into incumbent and specialist suppliers—profiling engineering capabilities, typical customer segments, and strategic positioning. A selection of firms examined in the report illustrates the diversity of suppliers that shape the market:

Each supplier profile in the full report includes engineering strengths, reference installations, typical lead times, maintenance footprints and suggested contractual structures for 2026 procurement (e.g., performance-based guarantees, spare-parts bundling, training packages).

Selected developments tracked by PW Consulting illustrate where the market is heading:

Collectively, these signals underscore two 2026 priorities: securing validated supply partnerships for critical alloys, and building flexible capacity that can pivot between premium and commodity powder grades.

The report is built for executives who need executable insight rather than abstract trends. It includes:

Leaders should convert the report’s insights into a three-part action plan for 2026:

As the market enters its next growth phase, atomizer investments are becoming decisive elements of competitive strategy rather than isolated procurement events. The projected CAGR of 6.84% highlights steady expansion, but the differential between high-purity, high-value powders and commodity grades will widen. Companies that combine rigorous supplier selection, targeted technology investments, and OPEX-led efficiency programs will be best placed to turn 2026 opportunities into multi-year advantage.

PW Consulting’s full Metal Powder Atomizer Market report contains the underlying data, proprietary segment intelligence, and vendor scorecards that inform the strategic recommendations summarized here. To access the in-depth segmentation, model assumptions, and vendor benchmarking used to generate these conclusions, please consult the report page on our website.

For detailed analysis of this topic, please visit the official page:Metal Powder Atomizer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com