Understanding Liposuction: Benefits and Risks in Riyadh

Health |

2026-04-11 06:11:28

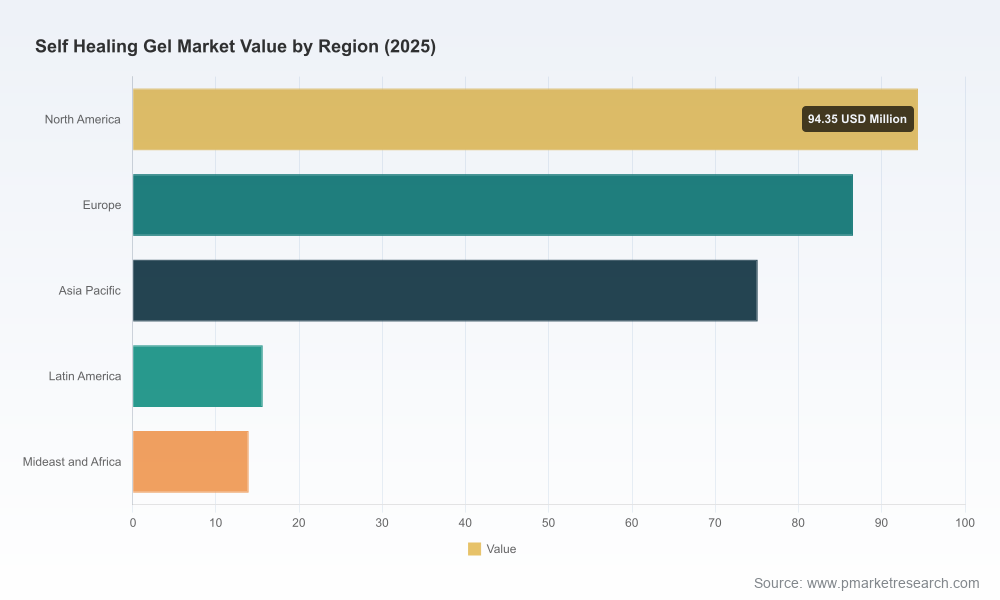

As the chief industry analyst at PW Consulting, I am pleased to introduce our latest market research on Self‑Healing Gels — a technology axis that is poised to reshape wound care, soft robotics, biomedical devices and next‑generation adhesives between 2026 and 2032. Our base‑year analysis shows the market reached USD 285.5 Million in 2025 and, under the scenarios modelled in this study, is projected to expand at a compound annual growth rate (CAGR) of 9.85% to approximately USD 551.15 Million by 2032. Those headline figures capture the macro momentum; the strategic challenge for executives in 2026 is translating that momentum into defensible, margin‑accretive commercialization paths. This release outlines the decision‑critical insights from the report while deliberately withholding granular segment‑level tables so that interested parties are directed to the full report for proprietary breakdowns and downloadable tools.

Self Healing Gel Market

Three converging dynamics make 2026 a make‑or‑break year for players in the self‑healing gel ecosystem. First, regulatory regimes are simultaneously enabling and constraining innovation: accelerated pathways in jurisdictions such as the U.S. are shortening time‑to‑market for advanced wound care products, but parallel expectations for robust clinical evidence and post‑market surveillance raise development costs and operational complexity in major markets. Second, science and product innovation continue to accelerate — material platforms that combine rapid mechanical recovery with bioactive release profiles are moving from lab to bedside, creating new use cases but also higher standards for manufacturing controls. Third, end‑market economics remain unsettled: clinical adoption in trauma and specialised centres is advancing faster than reimbursement systems in many markets, creating a patchwork commercial environment in which commercial strategy must be coordinated with payer engagement and evidence generation.

Self Healing Gel Market

These deliverables are designed to be operational from day one: slide‑ready GTM plans, editable clinical protocol templates and modelled financials that teams can use to test strategic options. To preserve the commercial value of our proprietary work product, aggregate headline numbers appear in this brief but segmented numeric tables, regional breakdowns and application share figures are retained in the full report.

Self Healing Gel Market

The market structure remains de‑consolidated: our concentration metrics indicate that the top three players account for a relatively modest share of the market, while the top five bring the cumulative concentration to a level that signals both continued fragmentation and rising consolidation pressure. That configuration creates a set of strategic plays we outline in the report: scale through distribution and manufacturing, capability acquisition via targeted M&A, and differentiation through clinical evidence and IP‑backed formulations.

Key players profiled in the report span established medtech platforms, specialized hydrogel innovators and materials specialists. Examples include Advanced Medical Solutions Group PLC and Smith & Nephew, who leverage large commercial footprints and strong clinical channels; 3M and Cardinal Health, whose scale and distribution can compress commercialization timelines; specialized innovators such as Hydromer and Axelgaard, which focus on coatings, sensing and device‑integrated hydrogel applications; and high‑velocity startups like Gel4Med, which has converted regulatory clearances into rapid clinical evidence generation. Mid‑sized firms such as Alliqua and Contura operate in niche segments and are attractive targets for partnerships or bolt‑on acquisitions.

Recent developments underscore the speed of translation from lab to clinic: Gel4Med’s real‑world evidence publication in partnership with a leading academic medical centre documented accelerated healing in diabetic foot ulcers, reinforcing the commercial value of clinically validated matrices; Gel4Med’s prior 510(k) clearance opened market pathways that others are racing to emulate. Parallel academic breakthroughs — including a March 2025 publication demonstrating a skin‑mimetic hydrogel with high mechanical strength and rapid self‑repair, and polysaccharide‑based smart release systems reported in early 2025 — signal that new entrants with platform IP could rapidly influence product roadmaps and competitive positioning.

Our scenario set translates the headline CAGR into commercial outcomes under three adoption archetypes: conservative, base case and accelerated uptake. The base case aligns with the 9.85% CAGR projection and assumes staged uptake across acute wound care and select device integrations; the accelerated uptake scenario models faster reimbursement and rapid national roll‑outs in major markets, while the conservative scenario reflects slower payer acceptance and supply constraints. For executive teams, the critical decision is which scenario to plan for: build to scale (capex and supplier contracts) or pursue nimble, evidence‑first roll‑outs. The report contains downloadable financial models that let you input your own pricing, uptake and cost assumptions to quantify NPV, payback and margin sensitivity without exposing our proprietary segment forecasts in a public summary.

The full report supplies the scorecards, templates and granular forecasts needed to execute each step; this press summary intentionally avoids publishing segment‑level percentages and regional/application tables so that corporate subscribers access the full, interactive dataset on our portal.

PW Consulting’s Self‑Healing Gel Market report is written for boardroom decisions in 2026 — enabling CEOs, commercial leads, R&D heads and corporate development teams to convert scientific momentum into defensible commercial positions. If your organisation is evaluating entry, scale, or acquisition opportunities in self‑healing gels, the report equips you with executable playbooks, regulatory timelines and financial models tuned to current market dynamics. For access to the full dataset, company scorecards, downloadable financial models and our proprietary segment‑level forecasts, please visit the PW Consulting report page. Our team is prepared to deliver an executive briefing and a custom scenario workshop within two weeks of subscription.

— PW Consulting, Global Strategy & Industry Analysis

For detailed analysis of this topic, please visit the official page:Self Healing Gel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com