Indomethacin Market Forecast: Competitive Landscape, Emerging Trends, and Future Outlook

Other |

2026-04-02 11:32:04

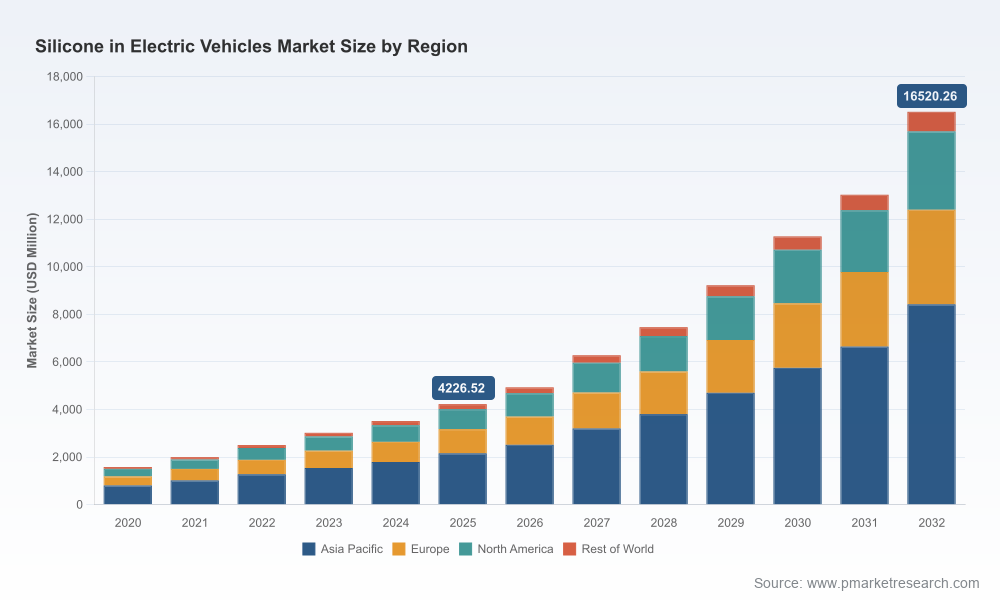

PW Consulting’s latest market study — Silicone in Electric Vehicles Market (Base year: 2025; Forecast: 2026–2032) — translates rapid product and policy shifts into a pragmatic roadmap for industrial leaders preparing decisions in 2026. The sector is moving from niche performance chemistry to an operationally critical material class across battery systems, power electronics, and drivetrain components. Our analysis projects a high-growth trajectory driven by electrification scale-up, tighter safety regulations, and accelerating innovation in thermal management: the market expands from the mid‑single‑billion USD scale in 2025 to a multi‑billion footprint by 2032, reflecting a compounded annual growth rate (CAGR) of 21.5% over the forecast window. This briefing highlights the strategic value of the report for executive decision-making while intentionally withholding detailed sub-segment tabulations to direct stakeholders to the full report for transaction‑level intelligence.

Silicone In Electric Vehicles Market

Several converging dynamics make 2026 a hinge year for silicone suppliers, automotive OEMs, and tier‑1 system integrators. First, regulatory ceilings on battery safety and materials composition have hardened in key markets, raising the technical bar for encapsulants, sealants, and flame‑retardant components. Second, EV volume growth has entered a phase where component selection materially affects manufacturing throughput, warranty risk, and total cost of ownership. Third, commodity and feedstock volatility has translated into meaningful cost pressure across silicone value chains, altering supplier economics and contract structures. Together these forces create a narrow window for strategic moves that lock in scale advantages, protect margins, and secure customer lock‑in.

Silicone In Electric Vehicles Market

The overall silicone-in-EV market demonstrated consistent expansion through 2020–2025 and emerges from that period poised for accelerated adoption across the vehicle architecture. Under our baseline, total market value climbs markedly in the 2026–2032 forecast horizon, driven primarily by widescale adoption of silicone solutions in battery thermal management, power electronics, and inverter/motor protection layers. For strategists, the implication is clear: component‑level volume sensitivity will dominate supplier bargaining power — firms that can demonstrate validated thermal performance, regulatory compliance, and scalable production will capture disproportionate share as OEMs de‑risk supplier bases ahead of large platform ramps.

Silicone In Electric Vehicles Market

Regulatory acceleration — New safety mandates (e.g., EU battery requirements adopted in recent years) have made flame retardancy and material traceability non‑negotiable attributes for battery systems. This alters qualifying criteria for materials and accelerates migration to certified silicone solutions for critical battery components.

Volume and application pull — The expansion of EV fleets and charging infrastructure continues to lift demand for silicone-based thermal interface materials, potting compounds, and EMI/insulation systems. Market adoption is not uniform by application; however, the overall uplift is broad‑based and persistent.

Input cost volatility — Recent uplifts in silicone rubber pricing and polysiloxane feedstock costs, driven in part by energy price swings and upstream metal availability, have compressed historical margins and necessitated revised procurement and hedging approaches. Expect continued supplier focus on feedstock diversification and process efficiencies.

Technology de‑risking — OEMs and battery manufacturers are increasingly testing silicone formulations at cell and pack level rather than component level, shifting validation cycles and creating premium value for materials with demonstrated long‑term performance in harsh thermal and electrical environments.

Our report dissects the market across product and application axes — from elastomers, gels, resins, fluids, and adhesives/sealants to battery thermal management, power electronics, motors, charging systems, and interior/exterior use cases. Instead of publishing the underlying segmentation tables here, we highlight the directional takeaways:

Market concentration data indicate a moderately consolidated supplier base: the top three firms account for a substantial share of the market, and the top five extend that dominance further. This balance presents both barriers and openings — incumbent leaders offer scale, broad product portfolios, and deep customer relationships; meanwhile, mid‑tier and specialized players can disrupt through rapid innovation or narrowly tailored, high‑performance solutions.

Key profiles and strategic positioning we examine in the report include:

Recent industry moves — product launches and trade show showcases by major players throughout 2025 — confirm that incumbents are sharpening portfolios around thermal management and regulatory qualification. These developments accelerate qualification timelines for EV platforms and raise the bar for new entrants.

PW Consulting’s practitioner‑oriented recommendations are designed to be implemented within 6–18 months and are covered in detail in the full report. Key priorities for 2026 include:

The full PW Consulting report is designed as an executable playbook for 2026 decisions. It includes:

To protect the commercial sensitivity of segmentation-level monetizations and proprietary vendor assessments, the full numeric tables and company-specific revenue splits are available through the PW Consulting research portal and licensed subscription channels. This briefing is intended to orient executives to the critical choices and to spur immediate action planning for 2026.

Silicone materials have transitioned from “nice to have” technical enablers to strategic inputs that materially shape EV system reliability, manufacturability, and regulatory compliance. The market’s strong CAGR and the trajectory of total market value through 2032 create both opportunity and urgency. For suppliers, the choice is between investing in scale, validation, and service capabilities now — or accepting commoditization pressures as OEMs consolidate their qualified supplier lists. For OEMs and tier‑1s, the choice is between locking in high‑performance, traceable supply chains or absorbing warranty and regulatory risk over the next product cycles.

PW Consulting’s Silicone in Electric Vehicles Market report converts these choices into a defined set of decisions, timelines, and financial sensitivities to support board‑level strategy and mid‑year planning in 2026. For access to the full dataset, scenario spreadsheets, and the supplier playbook, please consult PW Consulting’s research portal or contact our advisory desk to arrange a personalized briefing.

For detailed analysis of this topic, please visit the official page:Silicone In Electric Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com