Возведение, модернизация, а так же ремонт рельсовых линий

Other |

2026-05-14 18:12:26

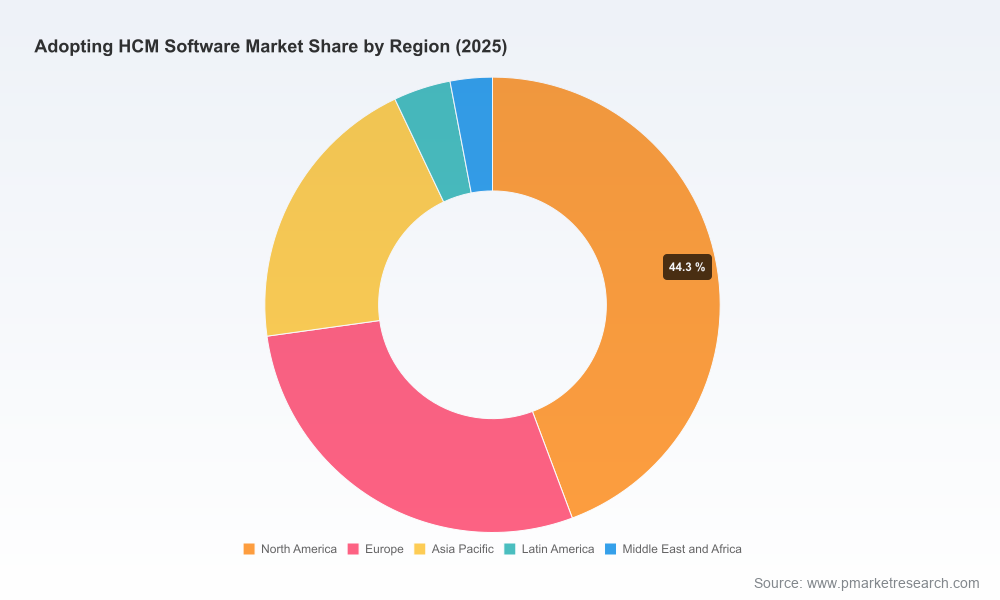

PW Consulting’s new market research brief, Adopting HCM Software Market (Base year: 2025; Historical: 2020–2025; Forecast: 2026–2032), distills the signals that will shape human capital management (HCM) investments through the next planning cycle. Our modelling shows the global HCM market accelerating from a 2025 base and tracking to a robust compound annual growth rate (CAGR) of 9.24% across the 2026–2032 forecast window. By 2032 the market is projected to be materially larger than today, reflecting sustained demand for integrated HR, payroll, talent and workforce management capabilities as enterprises retool for hybrid workforces, regulatory scrutiny and pervasive AI adoption.

Adopting Hcm Software Market

Timing and spend allocation: The growth trajectory signals that 2026 will be a pivotal year for portfolio rebalancing—organizations that move early to rationalize legacy systems, negotiate enterprise terms, and lock in roadmaps with vendors will capture disproportionate efficiency and talent-management gains.

Adopting Hcm Software Market

Risk and compliance posture: New privacy and automated-decisioning rules heighten legal and operational risk for HCM deployments. Strategic procurement must now bake in privacy impact assessments, vendor audit rights and integration controls as non-negotiable contracting elements.

Adopting Hcm Software Market

Vendor concentration and negotiation leverage: Market concentration metrics indicate a marketplace where a small set of global providers maintain substantial share, but enough fragmentation exists to preserve competitive tension—an environment that rewards sophisticated sourcing and phased adoption strategies.

The full study is built as an execution toolkit for C-suite, HR leaders, IT procurement and transformation teams. Rather than simply charting topline trends, we provide actionable assets designed for direct use in vendor selection, budgeting and program management. Highlights include:

Decision frameworks that map business priorities (growth, cost, compliance, employee experience) to HCM capability sets and implementation sequencing.

Vendor evaluation scorecards that combine capability, roadmap fit, integration risk and commercial flexibility—designed to be used as a working annex during RFPs.

ROI and TCO templates calibrated to the report’s macro market model to help CFOs and HR leaders stress-test scenarios across different adoption timelines and scales.

Migration playbooks and data-mapping matrices for common legacy-to-cloud transitions, including phased rollouts that reduce business disruption.

Compliance and governance checklists tailored for key regulatory regimes and for AI-assisted decisioning within HR processes.

Operational benchmarks and case vignettes covering time-to-value, typical implementation risks, and post-go-live optimization levers.

Our quantitative base uses annualized market sizing from 2020 through 2025 and projects forward to 2032. The headline growth rate (CAGR 2026–2032 = 9.24%) reflects three reinforcing forces: continued replacement of legacy on-premise systems; rising spend on AI-enabled talent management and employee experience; and expanding scope of HCM platforms to encompass workforce analytics and real-time payroll. Together these drivers create both scale opportunities and integration complexity for buyers and vendors alike.

Market concentration analysis in the report provides an objective lens on competitive dynamics. While the top-tier vendors hold meaningful share—creating stable enterprise-grade options—there is still room for specialized and vertically oriented providers to compete on differentiation and speed to value. This combination of scale and fragmentation is why procurement strategy matters: it determines whether organizations gain vendor-driven innovation or become constrained by long migration cycles.

The report profiles the major suppliers and evaluates their strategic posture along product breadth, global compliance capability, AI/automation maturity and target customer segments. Representative vendors covered include cloud-first incumbents, long-established ERP providers that have replatformed HCM, payroll specialists, and fast-growing modern platforms focused on seamless integrations and middle-market agility.

Cloud-native enterprise suites are advancing AI-enabled workforce planning, recognition and employee experience modules to secure renewals and large deals; several recent platform releases and strategic partnerships have reinforced this trend.

Payroll and global workforce specialists continue to strengthen cross-border compliance and payroll accuracy—an essential capability in multi-jurisdiction rollouts where regulatory expectations for data protection and auditing have intensified.

Mid-market and SMB vendors differentiate via rapid deployment templates, single-database simplicity and price-performance, but must continually invest in compliance and interoperability to address growing buyer demands.

Major platform vendors have accelerated releases and partnerships focused on AI-driven HR workflows and recognition mechanics—these moves raise the baseline functionality buyers should expect when negotiating new contracts.

Large vendors’ consolidated workforce suites and product integrations aim to reduce friction for global customers but also increase vendor lock-in risk—an important factor in governance and exit planning.

Regulatory shifts in privacy and automated decision-making—especially in key jurisdictions—mean compliance is now a first-order procurement criterion, not a post-implementation checklist.

Two regulatory realities stand out. First, enhanced privacy and ADMT (automated decision-making technology) rules require demonstrable safeguards around HR data usage, transparency of algorithmic decisions, and routine risk assessments. Second, long-standing frameworks for data protection continue to require formal impact assessments for large-scale processing and AI applications. These obligations alter both RFP requirements and vendor diligence protocols.

On the cost side, cloud-first adoption reduces infrastructure friction but introduces new areas for optimization—chief among them inefficient or unused SaaS spend. Buyers must therefore balance the commercial simplicity of managed cloud offers with active governance practices to curb waste and align operational metrics to business outcomes.

Prioritize modularity: Structure contracts to allow phased adoption of high-value modules (e.g., talent mobility, payroll modernization) while preserving flexibility to pivot as vendor roadmaps evolve.

Embed compliance gates early: Make privacy impact assessments, algorithmic explainability and external audit rights mandatory parts of procurement and implementation milestones.

Negotiate optimization clauses: Insist on transparent usage metrics, rights to cost audits, and mechanisms to reclaim wasted SaaS spend as part of vendor commercial terms.

Align AI adoption to business outcomes: Avoid technology-first buys. Define clear KPIs for how AI features will materially improve recruitment, retention, productivity or payroll accuracy, and require vendors to validate those claims with client references and measurable baselines.

Use competitive tension: Leverage a mix of established global vendors and niche specialists to secure innovation and pricing leverage, while safeguarding integration and support guarantees.

This study is designed as a practical companion for fiscal and HR planning in 2026. It blends a rigorous market model with pragmatic takeaways—scalable templates, negotiation playbooks, and vendor scorecards—built to be applied during RFPs, board-level reviews and transformation programs. The report will help leaders shorten decision cycles, reduce deployment risk and convert strategic HCM intent into measurable outcomes.

If your 2026 planning includes HCM modernization, our report is the next rational step. We present the macro sizing and growth context to justify investment levels, the competitive intelligence to inform vendor selection, and actionable tools to accelerate time-to-value. For teams preparing budgets, negotiating renewals, or mapping multi-year transformation programs, the brief is a concise road map with the operational scaffolding needed to execute confidently.

To access the complete analysis, including the full market model, vendor benchmarking matrices, and downloadable implementation templates, please consult the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Adopting Hcm Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com