AI Code Market Overview: Key Drivers and Challenges

Other |

2026-03-24 09:30:13

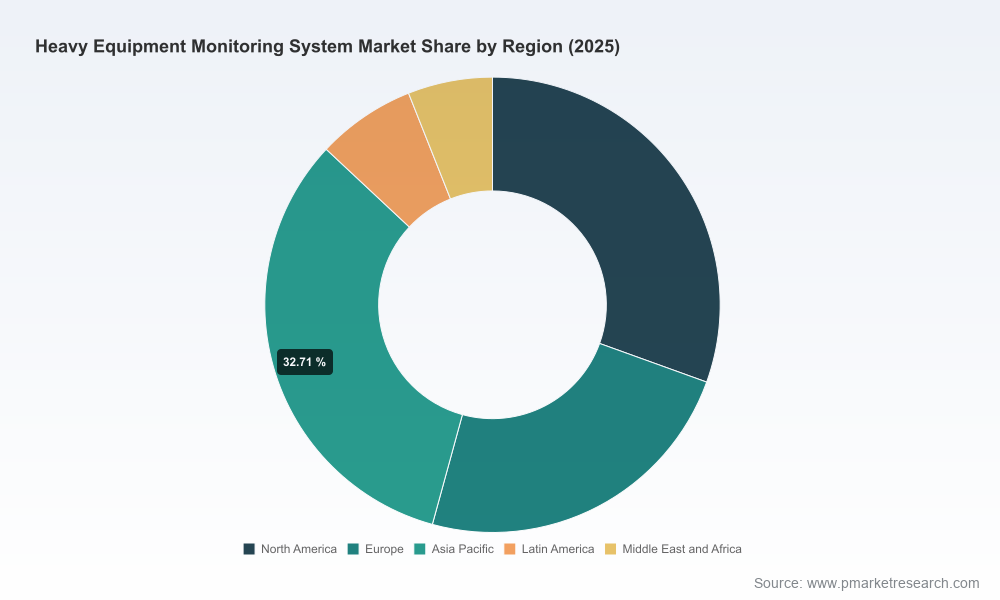

PW Consulting’s latest market study on Heavy Equipment Monitoring Systems positions the industry at a decisive inflection point as enterprises plan capital and operational decisions for 2026. Our analysis shows the global market expanding from approximately USD 3.95 billion in 2020 to USD 5.54 billion in 2025 (base year), with a projected compound annual growth rate (CAGR) of 7.0% across the 2026–2032 forecast window. Under that trajectory, the market is set to approach roughly USD 8.9 billion by 2032. These headline numbers are only the starting point; the full strategic value lies in the cross‑sectional intelligence, scenario modelling, and executable playbooks contained in the report.

Heavy Equipment Monitoring System Market

Budget timing: Many capital and IT budgets approved in late 2025 will be implemented in 2026. Accurate, vendor‑aware sizing and near‑term adoption curves can materially change fleet modernization plans.

Heavy Equipment Monitoring System Market

Compliance and safety: New international standards and evolving occupational limits are pushing monitoring systems from optional efficiency enablers into compliance‑critical components of heavy equipment ecosystems.

Heavy Equipment Monitoring System Market

Technology window: Advances in embedded sensors, edge compute, and AI‑driven diagnostics create a narrow window for incumbent OEMs and new entrants to secure defensible telematics positions before commoditization accelerates.

Our study synthesizes macroeconomic adoption drivers with bottom‑up device and software trends. Primary growth drivers include: digitization of fleet operations, rising demand for predictive maintenance to reduce downtime, regulatory requirements that increasingly mandate environmental and health monitoring, and the proliferation of mixed‑fleet management needs on large construction and mining projects.

At the same time, constraints persist: integration complexity with legacy ECUs, seasonal capex variability in end‑use industries, and supply‑chain exposure for critical components such as GPS modules, vibration and environmental sensors, and telematics control units. These component dependencies shape supplier strategies and price sensitivity across regions.

Important contextual signals we track closely: the introduction of ISO 23725 on autonomous systems and fleet interoperability (2024) and ISO 23875 addressing air quality in operator cabins — both of which materially increase interoperability and environmental monitoring requirements. Additionally, revised occupational exposure limits for crystalline silica in mining require engineering controls and real‑time monitoring that integrate with heavy equipment telematics. These regulatory developments convert what was a performance improvement market into one with compliance obligations embedded in procurement criteria.

The market is characterized by a blend of large OEMs, telematics and platform specialists, and focused hardware suppliers. OEMs with integrated service ecosystems (productized hardware plus software and service bundles) continue to leverage installed bases and dealer networks to deepen customer value propositions. Specialist telematics and software providers focus on neutral, mixed‑fleet visibility and third‑party integrations to capture customers with heterogeneous equipment portfolios.

OEM incumbents: Major equipment manufacturers provide end‑to‑end offerings that bundle telematics hardware, machine health diagnostics, and data platforms. These players possess the advantage of direct vehicle integration and dealer servicing channels, enabling higher attach rates for long‑term service contracts.

Platform and telematics specialists: Vendors focused on fleets and platform software differentiate on interoperability standards, mixed‑fleet analytics, and scalable SaaS capabilities. Their strategic pull is strong among contractors who prioritize cross‑OEM visibility and rapid deployment.

Hardware and rugged device suppliers: There remains a distinct market for IP‑rated telematics devices and edge controllers designed for harsh operating environments. These suppliers underpin the data capture layer and can influence total cost of ownership through durability and integration simplicity.

Representative vendors profiled in the report include established OEMs with telematics suites, large systems integrators and software platform vendors, and specialist hardware providers. Each profile includes strategic positioning, go‑to‑market routes, strengths and exposure to shifting value pools (hardware, software, services), and an assessment of their readiness to compete in subscription and services models that are rapidly displacing one‑time hardware sales.

Market concentration metrics indicate a market where a handful of firms account for a meaningful share of revenue, while a long tail of regional specialists and niche players remains influential. This structure creates dual strategic paths: scale‑driven consolidation opportunities for buyers and software‑led disruption for nimble vendors that can deliver rapid ROI across mixed fleets. Our strategic playbooks outline acquisition targets, potential partnership models, and scenarios where channel exclusivity with dealer networks produces sustained competitive advantage.

Beyond market sizing and high‑level forecasts, PW Consulting’s report is designed as a practical decision tool for procurement teams, product leaders, investors, and fleet operators preparing 2026 roadmaps. Key deliverables include:

Actionable implementation playbooks for pilot design, data architecture, and roll‑out sequencing that minimize operational disruption.

Vendor benchmark framework covering technology fit, deployment risk, and commercial models (hardware sale vs. device leasing vs. SaaS), with scoring that emphasizes interoperability and lifecycle TCO.

Compliance matrix mapping regulatory requirements to monitoring features and sensor suites, enabling quick gap analysis for safety and environmental teams.

Financial models and ROI calculators tailored to fleet sizes and usage profiles, to support CAPEX vs. OPEX decisioning and service‑level negotiations.

M&A and partnerships heatmap highlighting consolidation corridors, white‑space segments, and likely targets for strategic investment.

In keeping with our "prequel" approach, this public summary highlights themes and strategic conclusions while withholding the full set of segmented tables, vendor scorecards and proprietary scenario outputs. These detailed exhibits are accessible in the full report and data appendices on PW Consulting’s portal.

Recent product and trade show activity signal where competition and customer expectations will concentrate in 2026. Examples include the unveiling of advanced 3D machine control and AI‑based awareness systems at major industry events, and OEM showcases that emphasize integrated jobsite telematics and new‑energy powertrain monitoring. These innovations accelerate the migration from single‑use tracking telematics toward comprehensive site productivity and compliance platforms.

For executives planning 2026 actions, we recommend the following tactical priorities:

Fleet operators: Prioritize interoperability in procurement. Run two parallel pilots — one focused on predictive maintenance and one on environmental/compliance monitoring — and compare vendor TCO and data portability over a 12‑ to 18‑month horizon.

OEMs: Transition commercial models toward recurring revenue with modular software tiers and outcome‑based service agreements; protect margins by investing in edge compute capabilities and dealer enablement for aftersales services.

System integrators and software specialists: Differentiate on mixed‑fleet analytics and rapid integrations to standards such as AEMP and the ISO family; build partnerships to offer bundled deployment and compliance assurance.

Private equity and corporate development teams: Screen targets that provide either unique sensor IP, durable hardware with high attachment rates, or software platforms with sticky subscription economics; prioritize targets that reduce integration risk for large contractors.

Risk & compliance teams: Map existing fleet telematics against regulatory obligations (e.g., occupational exposure limits and cabin air quality requirements) and prioritize sensor upgrades in high‑risk assets first.

The market trajectory and regulatory backdrop create a compelling case for strategic action in 2026. Companies that lock in interoperable architectures, invest in edge analytics, and reconfigure commercial models to favor recurring revenue will secure disproportionate long‑term value. Conversely, players that defer integration and compliance investments will face rising retrofit costs and increasing customer churn as fleet owners demand platform‑level outcomes rather than isolated device purchases.

PW Consulting’s Heavy Equipment Monitoring System Market report gives decision‑makers the situational awareness, vendor intelligence, and executable playbooks required to act decisively. For access to the full segmented datasets, vendor scorecards, financial models, and implementation templates referenced in this briefing, visit the PW Consulting report page to download the complete study.

For detailed analysis of this topic, please visit the official page:Heavy Equipment Monitoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com