How Precision Machining Market Share Asia-pacific Demand Surges

Other |

2026-05-25 11:17:22

PW Consulting today releases a comprehensive market intelligence brief that reframes how corporate leaders should think about disposable alcohol wipes entering the next strategic cycle (2026–2032). Built from a five-year historical view and a detailed forward-looking forecast, the report synthesizes market sizing, competitive dynamics, regulatory vectors and supply‑chain stress‑tests into a decision-grade playbook for CEOs, commercial heads, and procurement teams.

Disposable Alcohol Wipes Market

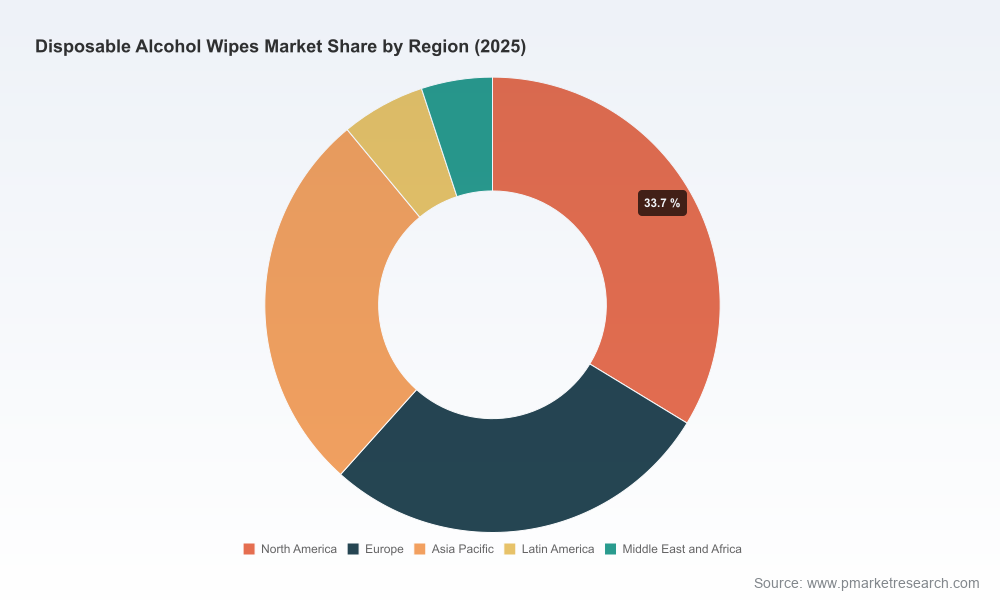

The disposable alcohol wipes market is re-establishing itself as a durable, innovation-driven category after early‑decade volatility. Our analysis uses 2025 as the anchoring base year and projects a steady compound annual growth rate (CAGR) of 5.48% through 2032. By 2032, the global market is forecast to surpass the billion‑dollar threshold (USD, revenue unit: Million), underscoring a predictable expansion window for companies that resolve near‑term operational and regulatory frictions.

Disposable Alcohol Wipes Market

For executive teams, three implications follow immediately:

Disposable Alcohol Wipes Market

This is not a descriptive survey. The report is structured to arm decision-makers with tools they can deploy in the next 90–360 days:

The competitive field is anchored by legacy players with scale manufacturing, broad distribution, and institutional customer footprints, complemented by specialized OEMs and nimble innovators. Key archetypes we profile in detail include:

Our company profiles go beyond publicly available narratives: each includes independent assessments of regulatory readiness, formulation pipelines, manufacturing redundancy, and commercial elasticity. Importantly, concentration metrics in the report indicate moderate market aggregation—enough scale to matter, and enough fragmentation to allow agile entrants to capture share.

Three recent developments illustrate the near‑term shaping forces:

Raw material costs remain the principal near‑term disruptor. IPA accounts for a material share of formulation cost and has experienced meaningful year‑over‑year price swings—creating episodic margin pressure. Non‑woven substrates, mostly petroleum‑derived, represent a second material cost category vulnerable to polymer price moves and logistics disruptions.

The report provides procurement playbooks: multi‑sourcing, index‑linked contracts, on‑site IPA storage economics, and substitution pathways (including validated ethanol sources and plastic‑free pulp substrates) that preserve efficacy while improving supply resilience.

Regulatory complexity is a differentiator. Disinfectant wipes that make pathogen‑kill claims are regulated as antimicrobials by the EPA and require registration; certain prep pads and sterile wipes fall under FDA OTC/medical device oversight. Our regulatory roadmap clarifies timelines, required clinical/efficacy evidence, label claim strategies, and disposal/handling obligations to avoid enforcement and reputational risk.

PW Consulting’s analysis yields a prioritized set of actions for companies seeking to convert market growth into durable advantage.

Given moderate concentration and persistent technical entry barriers, our M&A scorecard prioritizes targets with certified manufacturing (cGMP), validated EPA/FDA dossiers, and excess capacity. Strategic alliances with ethanol producers or non‑woven innovators reduce input exposure and unlock co‑development of next‑generation substrates.

PW Consulting’s Disposable Alcohol Wipes Market report is designed as an executable guide for 2026 planning. The public summary establishes the strategic context; the full report contains the confidential, proprietary component-level cost models, regional and application split analyses, company scorecards, procurement contract templates, and a supplier directory that together enable immediate implementation.

For teams planning capital allocation, supply agreements, product launches, or M&A targeting in 2026, the report is the operational roadmap to translate a steady market CAGR into predictable, defendable profit growth. To access the full intelligence pack (including the granular regional and application splits withheld from this release), visit the PW Consulting report page or contact your PW Consulting account representative.

This brief draws on PW Consulting’s proprietary data collection (covering 2020–2025 historical performance), primary interviews across the value chain, regulatory filings, and scenario modeling for 2026–2032. The report quantifies the market’s recovery and growth potential in a way that balances strategic visibility with the selective withholding of segmentation details to protect client value and encourage direct engagement for full insight.

For detailed analysis of this topic, please visit the official page:Disposable Alcohol Wipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com