Ready-to-Eat Broth Market: A 2026 Strategic Briefing from PW Consulting

As we enter 2026, food manufacturers, private-label owners, ingredient suppliers, and strategic investors face a market where convenience, wellness, and regulatory scrutiny are colliding to reshape competitive advantage in the ready-to-eat (RTE) broth category. PW Consulting’s latest Ready To Eat Broth Market report synthesizes five years of historical performance with a seven-year forecast, equipping leaders with the frameworks and practical playbooks needed to convert market signals into defensible growth. This briefing summarizes the strategic value of that analysis for decision-making in 2026 — while preserving the full granular intelligence for readers who access the complete report.

Ready To Eat Broth Market

Market snapshot: a resilient, steadily expanding category

The RTE broth market has demonstrated steady expansion through the early 2020s and is projected to continue growing at a mid-single-digit compound annual growth rate (CAGR) over the coming forecast window. By the end of the report’s base year the global market reached a multi-billion-dollar scale (USD, revenue basis) and our scenario modelling indicates progressive growth toward the end of the forecast period. This trajectory reflects a blend of sustained at-home consumption, growth in on-the-go and health-oriented usage occasions, and product innovation across formats and ingredient claims.

Ready To Eat Broth Market

Two consequences follow for 2026 planners: first, volume-driven strategies remain viable where scale reduces per-unit cost; second, margin-enhancing product differentiation (e.g., functional claims, premium sourcing) is required to outperform the headline category growth.

Ready To Eat Broth Market

Why 2026 is a strategic inflection point

- Input cost divergence: Commodity dynamics are bifurcating margins. Poultry supplies are broadly available and should exert downward pressure on broiler pricing into early 2026, whereas beef costs are under upward pressure with wholesale price increases projected. This asymmetry will materially affect mix economics for companies with exposure to both proteins.

- Regulatory tightening: Proposed changes to front-of-package nutrition labelling — categorizing nutrients as Low, Med, or High for saturated fat, sodium, and added sugars — plus ongoing Nutrition Facts label updates mean packaging, claims, and reformulation plans require immediate attention. Early alignment with expected label regimes reduces rework costs and protects time-to-shelf.

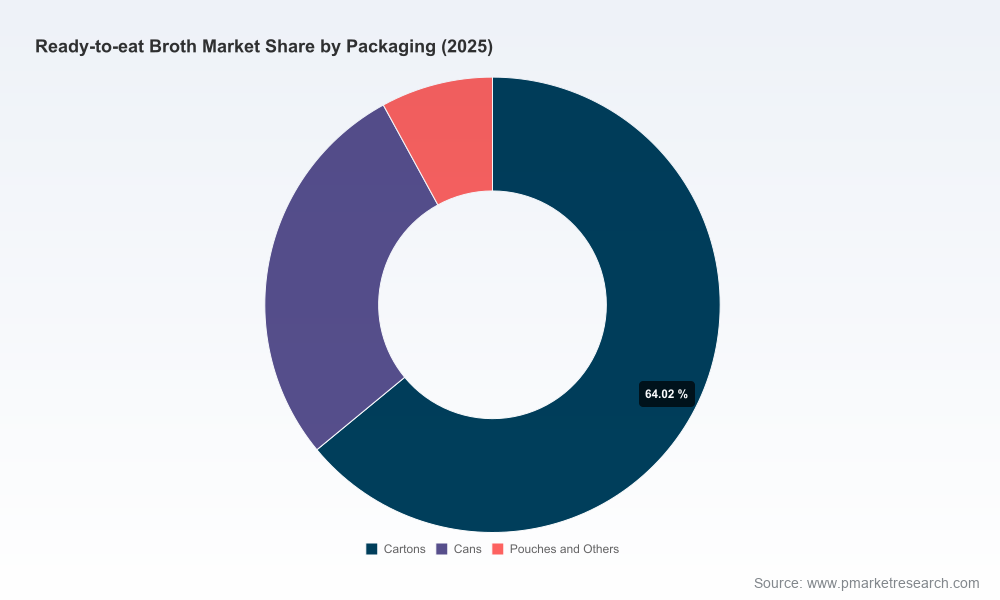

- Consumer health expectations: Demand for low-sodium, clean-label, organic and bone-broth style products continues to shape assortment strategies. Incumbents and challengers are expanding options that straddle culinary and wellness use-cases (sipping, soups, cooking bases), creating SKU proliferation that must be managed to avoid margin leakage.

- Channel evolution: Growth in direct-to-consumer, subscription services, and refrigerated/frozen hybrid channels creates new routing options — and new costs — for distribution and sampling strategies.

What PW Consulting’s report delivers

Our report is designed as an operator’s manual for 2026 decisions. It contains:

- Robust forecasting and scenario models: Base, upside, and downside cases driven by commodity price sensitivities, label/regulatory adoption timelines, and consumer adoption curves. Each scenario includes the implied revenue and margin path to assist capital allocation and inventory planning.

- Practical go-to-market playbooks: Channel-specific tactics for retail, e-commerce, foodservice, and D2C including assortment rationalization matrices, pricing ladder recommendations, and promotional cadence optimized to preserve margins while growing velocity.

- Portfolio and innovation frameworks: A decision tree for prioritizing SKU launches (e.g., functional formats, low-sodium reformulations, premium bone broths), and a prototyping scorecard that links R&D effort to expected net-present-value outcomes.

- Supply chain and procurement playbooks: Hedging and contracting templates, contingency plans for protein-cost spikes, co-manufacturer selection criteria, and a capacity-mapping tool to align manufacturing footprint with forecasted demand.

- Label and regulatory compliance toolkit: Implementation timelines, sample label mock-ups aligned with proposed front-of-package rules, and risk-check matrices for claims and nutrient thresholds to prevent regulatory back-and-forths.

- Competitive battlecards: Actionable intelligence on leading brands and challengers, their positioning, likely near-term moves, and vulnerability vectors—designed to power commercial conversations and M&A diligence without disclosing proprietary client data.

Competition: dynamics to watch in 2026

The category is concentrated around several global and specialist brands, with a meaningful middle tier of premium and health-focused challengers. Market concentration metrics indicate a top-tier cluster that controls a sizable share of the category, while a broader set of specialty players is carving out profitable niches.

Key firms to monitor include legacy consumer packaged goods companies with scale and distribution reach, such as global soup and condiment manufacturers, alongside emerging specialists focused on bone broths and clean-label propositions. These players are not just competing on flavor and price — they are differentiating on sourcing stories (organic, grass-fed), formulation (no-additives, low-sodium), and format convenience (cartons, pouches, and shelf-stable sipping cups). Recent examples underscore divergent approaches: boutique brands are launching no-salt-added organic broths to capture wellness channels, while larger incumbents are introducing new flavor lines to reignite mainstream demand.

Strategic imperatives for 2026

- Prioritize label-first reformulations: With front-of-package labelling proposals looming, reformulation to achieve favorable nutrient banding (especially sodium) will be a top value-creation lever. Early movers will benefit from prominent shelf presence when labels shift.

- Balance portfolio between value and premium: Maintain core, lower-cost SKUs to protect volume while selectively expanding premium, high-margin offerings that meet wellness or provenance claims. Use channel-specific assortments rather than universal SKU proliferation.

- Hedge protein exposure tactically: Where feasible, re-engineer recipes and supplier contracts to reduce simultaneous exposure to both rising beef costs and more stable poultry prices. Consider ingredient blends and plant-forward options to stabilize input cost elasticity.

- Invest in packaging that reduces friction: Convenience-driven formats that support sipping and snacking occasions (single-serve, resealable pouches) can materially increase purchase frequency. Packaging decisions should be tested against total landed cost and sustainability premiums consumers will pay.

- Use data-driven SKU rationalization: Trim slow-moving SKUs and redeploy marketing resources to high-contribution items. Our SKU profitability matrix enables rapid identification of candidates for delist, reformat, or premiumization.

- Consider bolt-on M&A and co-manufacturing partnerships: For companies seeking rapid entry into specialty niches (bone broth, organic, kosher), M&A remains an efficient path to acquire brand equity and co-packer relationships without long R&D cycles.

Operational risk and mitigation

Two operational risks dominate 2026 planning: input price volatility (especially beef) and compliance missteps as labelling rules change. Mitigation tactics include multi-year supply agreements with indexation clauses, strategic inventory buffers sized by scenario stress-tests, and pre-emptive label audits with staged rollouts. Our report includes templated contract language and an implementation calendar to accelerate these mitigations.

How the competitive landscape will evolve

Expect a dual-track evolution: incumbents will lean on distribution and promotional muscle to defend mainstream channels, while specialist brands will deepen ties with wellness communities and premium foodservice customers. Private-label programs will continue to pressure price tiers, but they also create opportunities for contract manufacturers and brand owners to secure stable volume via scale partnerships.

What we recommend executives do next (90-day playbook)

- Run a quick-scan of your SKU portfolio using our profitability matrix to identify top candidates for reformulation or delisting.

- Initiate sodium and nutrient-band stress-tests on top-selling SKUs against the proposed front-of-package rules to determine required reformulation delta and cost impact.

- Engage procurement to stress-test supplier contracts against beef and poultry price scenarios and secure optionality for alternative proteins or concentrated bases.

- Prioritize one pilot launch (new format or claim) in a controlled geography or channel to validate pricing elasticity and margin outcomes.

Closing—why our intelligence matters

For 2026, the Ready-to-Eat Broth category offers predictable headline growth but contains ample opportunity for share-shifting and margin expansion. Our report translates macro trends — commodity divergence, regulatory change, and shifting consumer expectations — into executable playbooks and measurable actions. It is designed to be immediately operational: forecasting models you can plug into your P&L, label mock-ups you can test, and negotiation playbooks you can use with suppliers and co-manufacturers.

To access the complete segmentation, regional breakdowns, SKU-level pricing matrices, and the confidential appendices that power our recommendations, please consult the full PW Consulting Ready To Eat Broth Market report on our website. The granular datasets and scenario spreadsheets are intentionally reserved for report subscribers to preserve competitive confidentiality while enabling rigorous strategic decision-making.

PW Consulting — preparing food industry leaders for the practical realities of 2026.

For detailed analysis of this topic, please visit the official page:Ready To Eat Broth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com