Powdered Disposable Gloves Market Size, Share, and Growth Opportunities

Other |

2026-06-26 14:32:18

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a strategic preview of our Multi-Parameter Monitoring Equipment Market study. This briefing distills the report’s most decision-relevant insights for leadership teams preparing capital allocations, product roadmaps, and M&A strategies in 2026 — while intentionally withholding the full breakouts and granular commercial data reserved for the full report.

Multi Parameter Monitoring Equipment Market

The multi-parameter monitoring market has been on a steady growth trajectory through the first half of the decade. From our baseline in 2025, the global market sits at an estimated USD 5.65 billion and is forecast to expand at a compound annual growth rate (CAGR) of approximately 5.82% through the 2026–2032 horizon, reaching a projected market scale north of USD 8.3 billion by 2032. That expansion reflects a combination of demand renewal in acute care, rising adoption of continuous monitoring outside traditional inpatient settings, and the gradual monetization of software and service layers attached to hardware platforms.

Multi Parameter Monitoring Equipment Market

Capital allocation: The mid-single-digit CAGR signals durable, investable growth but also increasing expectations for product differentiation and lifecycle economics. Decisions to expand manufacturing lines or to fund new platforms must be weighed against faster-growing adjacencies such as remote monitoring services and software-enabled analytics.

Multi Parameter Monitoring Equipment Market

Portfolio prioritization: Vendors and OEM suppliers must decide whether to double down on high-acuity platforms, pursue volume plays in mid/low-acuity segments, or accelerate hybrid offers combining hardware with subscription-based analytics. Each path carries distinct margin, regulatory, and go-to-market tradeoffs.

M&A and partnership timing: Market concentration metrics in our model indicate a moderately consolidated landscape among top vendors — an environment conducive to bolt-on acquisitions and technology partnerships to secure differentiation in AI-driven early warning, wearables, and interoperability solutions.

Supply chain resilience: Material cost inflation (notably in medical-grade silicones and polycarbonates) and episodic recalls underscore the need for sourcing redundancy and design-for-serviceability to protect margins and delivery promises.

Shift from product to platform economics: Leading suppliers are rapidly moving beyond device sales to capture recurring revenue through connectivity, remote monitoring, and predictive analytics. Investment choices made in 2026 around cloud architecture, device telemetry, and regulatory pathways for software-as-a-medical-device will determine who captures the software-inflected value pool.

Decentralization of monitoring: Continuous monitoring is migrating from ICU and OR to step-down units, ambulatory settings, EMS transport, and home care. This expands addressable markets but requires rethinking durability, battery life, wireless integration, and remote support models.

Modularity and integration: Modular designs that enable plug-and-play integration with ventilation, infusion pumps, and hospital information systems are becoming table stakes for hospitals seeking consolidated device ecosystems and lower total cost of ownership.

Regulatory and standards pressure: Devices continue to be regulated under established pathways (e.g., FDA Class II 510(k) in the U.S.) and must adhere to standards such as ISO 80601-2-61 for pulse oximetry performance. Regulatory strategy must now account for data privacy, cybersecurity, and SAMA rotation related to AI features.

Service and lifecycle economics: Aftermarket services — calibration, consumables, remote diagnostics — are essential margin engines. Organizations that systematically design for field serviceability and predictive maintenance can materially outperform peers on operating margins.

The vendor ecosystem blends global medical device incumbents, regional volume players, and adjacent-tech entrants. In our coverage, we profile established firms that exemplify different strategic postures:

Philips (Amsterdam) — Known for the IntelliVue family, Philips emphasizes integrated monitoring platforms and software-enabled early warning capabilities. Recent software updates showcase the firm’s focus on embedding AI-driven clinical decision support into monitoring workflows.

GE Healthcare (Chicago) — With modular CARESCAPE and B40 lines and a push into wearable mobility, GE continues to bridge high-acuity capability with mobility use-cases. The firm’s recent introductions underscore hospital mobility and continuous wearable monitoring as high-opportunity areas.

Dräger (Lübeck) — Dräger’s modular Acute Care series balances ventilation integration with multi-parameter monitoring; regulatory clearances in late 2024 position the company favorably for accelerating product placements in regulated markets.

Mindray (Shenzhen) — Competing on cost-performance, Mindray has been successful securing large-scale hospital contracts, particularly in markets where procurement is price-sensitive yet demands robust clinical features.

Nihon Kohden (Tokyo) — With a strong high-acuity lineage and advanced waveform analytics, Nihon Kohden remains a go-to for institutions prioritizing deep physiologic monitoring fidelity.

Masimo, Spacelabs, Baxter (Hillrom), Zoll, Schiller, Contec, and Edan — These players collectively round out the competitive set, bringing strengths across non-invasive sensing, transport/EMS solutions, bed-integrated monitoring, MRI-compatibility, and price-led offerings for clinics and home care.

Recent market moves — from Dräger’s regulatory clearances and GE’s wearable launches to Mindray’s contract wins and Philips’ AI-driven software updates — illustrate two concurrent dynamics: incumbents protecting core installed bases through incremental innovation, and nimble competitors scaling via price performance and targeted commercial executions.

Regulatory pathway discipline: For 2026 product launches, firms must map 510(k) timelines (or equivalent regional pathways) and integrate evidence generation early. The regulatory bar for AI/analytics features is rising, and premarket engagement accelerates time-to-market and reduces rework risk.

Reimbursement alignment: Providers will evaluate monitoring investments against clinical workflows and reimbursement constructs; critical care monitoring time is captured under established CPT/Medicare rules in several markets. Vendors should model reimbursement sensitivity across buyer segments when pricing integrated solutions.

Material supply volatility: Component cost inflation and periodic supply constraints require multi-sourcing strategies and design choices that limit reliance on scarce materials. Contracts combining price hedging and service-level commitments will be differentiators in procurement processes.

Quality legacy risk: Past remediation events (e.g., foam-related recalls) have lengthened buyer due diligence cycles. Manufacturers that can demonstrate rigorous post-market surveillance and transparent remediation processes will enjoy competitive advantages.

PW Consulting’s full report is designed as a working toolset for Boards, strategy teams, and deal teams. Key deliverables include:

A calibrated market model and forecast through 2032, with scenario analyses reflecting alternative adoption rates, pricing mixes, and software monetization assumptions.

Competitive benchmarking and proprietary scoring across product capability, channel strength, regulatory readiness, and service economics.

Go-to-market playbooks for incumbent and challenger players outlining channel mixes, pricing approaches, and hospital procurement tactics by buyer archetype.

Supplier risk heatmaps and recommended mitigation actions (dual sourcing, design substitutions, and inventory strategies).

M&A screening framework and a shortlist of strategic targets aligned to different corporate objectives (tech acceleration, geographic expansion, service consolidation).

Regulatory and reimbursement roadmaps tailored to the U.S., EU, and select APAC markets, including a checklist for premarket evidence and post-market surveillance obligations.

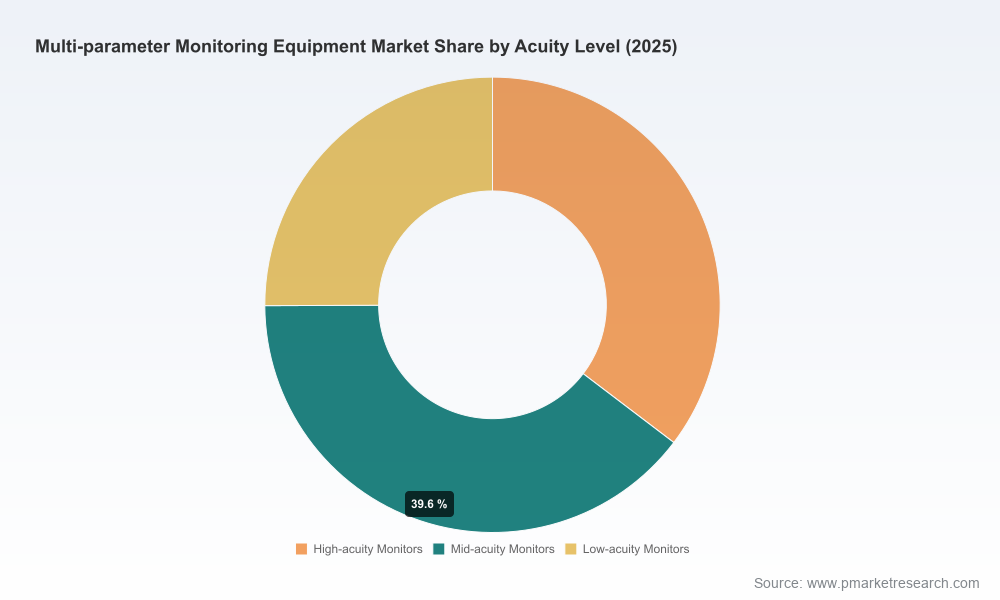

Note: To preserve the strategic “preview” posture of this release, we have not included the granular regional, acuity-level, or end-user revenue splits here. Those segment-level tables, unit forecasts, and price assumptions are fully documented in the full PW Consulting report and underpin our strategic recommendations.

Accelerate platform upgrades that unlock recurring revenue (connectivity, cloud services, analytics). Prioritize investments that improve lifetime customer value rather than one-off device sales.

Rebalance R&D to modular, upgradable hardware architectures that reduce replacement cycles and enable faster regulatory submissions for incremental features.

Strengthen service capability and remote support to convert higher uptime into premium pricing and retention advantages.

Pursue selective tuck-ins to acquire specific capabilities (AI/analytics, wearable sensors, EMS transport solutions) rather than broad, capacity-heavy acquisitions.

Lock in supply resilience through contract terms that address material cost volatility and create options for localized assembly in strategic markets.

Engage early with regulators on AI/analytics pathways and shape evidence generation programs that reduce approval risk and accelerate commercialization.

2026 will be a year of consolidation and clarification. The market’s steady growth provides a reliable backdrop for value creation, yet the winners will be companies that transform monitoring products into interoperable, service-rich platforms. PW Consulting’s full Multi-Parameter Monitoring Equipment Market report supplies the models, competitive intelligence, and implementation playbooks that leadership teams need to convert market trends into measurable strategic outcomes.

For Boards, investors, and commercial leaders evaluating product investment, M&A, or go-to-market pivots in 2026, the full report is the decision-grade resource that bridges high-level trends with transaction-ready detail. To access the complete dataset, segmented forecasts, and our bespoke strategic recommendations, please visit the PW Consulting report page for download and inquiry.

For detailed analysis of this topic, please visit the official page:Multi Parameter Monitoring Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com