Automotive Occupant Sensing Systems and Whiplash Protection: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive snapshot

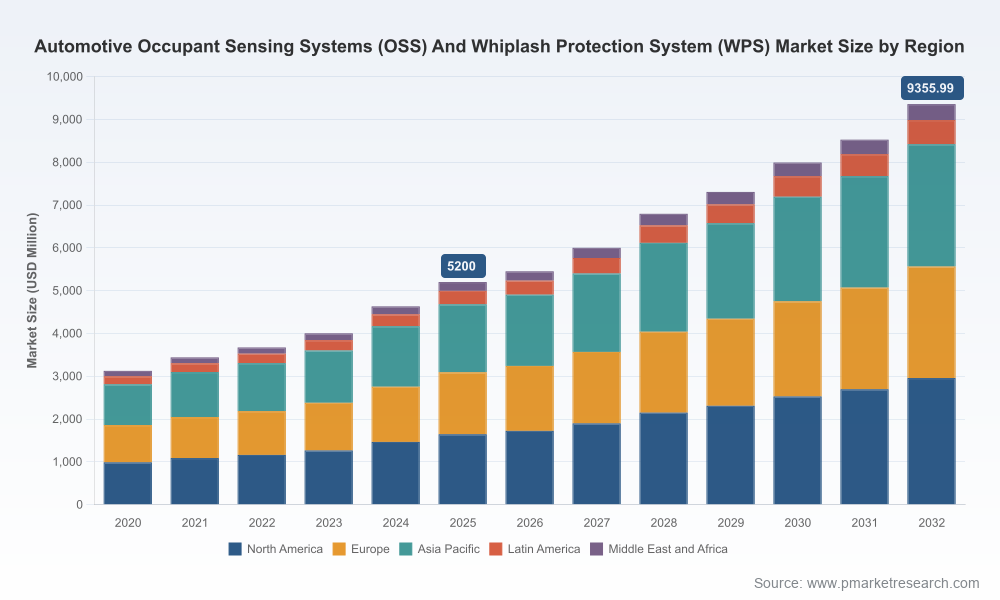

PW Consulting’s latest market study on Automotive Occupant Sensing Systems (OSS) and Whiplash Protection Systems (WPS) translates accelerating regulatory demand, technological convergence, and OEM program dynamics into an actionable strategic playbook for 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report quantifies an industry expanding at a compound annual growth rate (CAGR) of 8.75%. The global market crossed a major inflection point in 2025 (base year) and is projected to approach the mid‑nine‑thousand range (USD Million) by 2032 under base-case assumptions.

Automotive Occupant Sensing Systems Oss And Whiplash Protection System Wps Market

Why this matters for 2026 decision-makers

- Regulatory inflection: New Euro NCAP and IIHS protocols, together with EU General Safety Regulation requirements, have turned occupant classification and whiplash mitigation from optional differentiators into procurement imperatives for many OEMs.

- Technology convergence: Camera, radar, pressure-based sensing and seat-integrated systems are converging with AI-based occupant classification and fusion software — creating opportunities for systems integrators and risks for point-sensor players.

- Commercial timing: The 2026–2028 OEM program cycles are now shaping supplier selection and R&D roadmaps; firms that align product roadmaps with updated test protocols and vehicle launch timelines will capture disproportionate value.

Market trajectory — a data-driven view (high level)

Across the historical window (2020–2025) the market moved from a specialist safety niche into broad interior-sensing adoption, driven by expanding safety protocols and the integration of sensing into comfort and convenience features. The base year (2025) reflects this transition point. From 2026, our model projects steady compounding demand through 2032 underpinned by: regulatory enforcement, higher electronics content per vehicle, and increased adoption of multi‑modal sensing for occupant classification, child presence detection, and whiplash mitigation. The market’s mid-single-digit to high-single-digit CAGR reflects both replacement cycles and accelerating content per vehicle.

Automotive Occupant Sensing Systems Oss And Whiplash Protection System Wps Market

Primary growth drivers and headwinds

- Regulatory push: Euro NCAP’s 2026 protocols and IIHS’s updated whiplash prevention test issued in late 2025/early 2026 raise the bar for restraint adaptivity and seat/head restraint performance, creating new product requirements for sensor accuracy and system response.

- Safety‑to‑value span: OEMs increasingly require occupant sensing solutions that deliver both regulatory compliance and value-added features (occupant monitoring, drowsiness detection, child presence alerts), expanding addressable content.

- Sensor fusion & software: The shift from single-modality to fused systems (camera + radar + seat sensors + pressure mats) increases development complexity but also raises barriers to entry for pure-play hardware vendors lacking system integration capabilities.

- Semiconductor and supply chain constraints: Continued demand for MCUs, vision processors and radar front-ends will pressure sourcing, favoring suppliers with secure procurement and supplier diversification strategies.

- Testing and validation: New IIHS and Euro NCAP test protocols emphasize seat and restraint performance under varied occupant postures; this raises development and validation costs, disproportionately affecting smaller suppliers.

Competitive landscape — structure and strategic positioning

The OSS & WPS value chain is dominated by incumbent Tier‑1 safety suppliers, seat specialists, and diversified automotive systems integrators. Market concentration metrics indicate that the top three suppliers control a substantial portion of the industry’s revenue stream, with the top five extending that reach further — a structure that favors scale, certification track records and deep OEM relationships.

Automotive Occupant Sensing Systems Oss And Whiplash Protection System Wps Market

- Autoliv Inc. (Stockholm): Global leader in occupant sensing for airbag suppression/classification and integrated whiplash protection. Autoliv’s recent showcase of a holistic “Omni Safety” concept underlines its strategy to combine mechanical restraint innovations with integrated sensing and pelvis restraint concepts.

- Robert Bosch GmbH (Gerlingen): Advanced occupant protection electronics and interior sensing (camera/radar) expertise positions Bosch as a systems architect for OEMs seeking turnkey sensing and control modules.

- Continental AG (Hanover): Focused on cabin sensing stacks, Continental aims to marry detection/classification with vehicle-level safety orchestration, leveraging strong software and domain-control capabilities.

- Magna International (Aurora): Recent announcements show Magna winning multiple OEM programs for integrated camera+radar interior sensing, particularly for child presence detection — illustrating its role in cross-domain integration beyond traditional body/seat systems.

- ZF Friedrichshafen, Lear Corporation, Hyundai Mobis, Joyson Safety Systems, Grammer AG: These players cover the spectrum from restraint hardware and seat-integrated sensing to dedicated occupant-monitoring sensors, each competing on differentiation — whether through seat expertise (Grammer, Lear), electronics and control (ZF, Hyundai Mobis), or sensing algorithms (Joyson).

Recent market signals to act on in 2026

- Magna’s mid-2025 product awards for multi‑modal interior sensing programs indicate OEM preference for integrated suppliers capable of supplying complete sensing stacks — a trend that will influence RFP outcomes in 2026 programs.

- IIHS’s updated whiplash prevention evaluation released in early 2026 raises testing complexity for seats and head restraints; suppliers should prioritize validation investments and test‑guided design updates.

- Autoliv’s late‑2025 demonstrations emphasize collaborative restraint concepts and signal continuing innovation in mechanical and sensor-integrated solutions that meet evolving test protocols.

- Regulatory momentum (Euro NCAP, EU GSR) is accelerating interior sensing adoption for both safety and driver-monitoring mandates — converting what were optional luxury features into baseline safety requirements over the next two model cycles.

Strategic imperatives for suppliers, OEMs and investors

For organizations making resource-allocation decisions in 2026, PW Consulting identifies five actionable imperatives:

- Build system-integration competency: Success increasingly depends on sensor fusion, certified algorithms and vehicle-level safety orchestration. Suppliers should invest in software IP, cross-domain integration teams, and end-to-end validation capabilities.

- Align R&D with test protocols: Design de-risking against IIHS and Euro NCAP protocols should be a non-negotiable item in product roadmaps; early alignment accelerates OEM approvals and shortens qualification cycles.

- Secure critical component supply: Prioritize long‑lead semiconductor sourcing and diversify tier‑2 relationships for radar and vision modules to avoid program slippage.

- Pursue strategic partnerships and M&A selectively: Consider bolt‑on acquisitions for algorithmic capabilities, machine‑vision expertise, or specialized seat‑integrated sensing to close capability gaps quickly and credibly for OEMs.

- Commercial model innovation: OEMs and Tier‑1s will prefer suppliers that can demonstrate cost‑competitive, scalable production and validated software lifecycles; explore subscription/OTA update models for occupant monitoring feature upgrades.

What PW Consulting’s report delivers — practical, transaction‑ready outputs

This study is designed as a decision-ready tool for 2026 planners. Key deliverables include (select highlights):

- Market sizing and scenario-based forecasts through 2032 (base year 2025), including sensitivity runs tied to regulatory adoption rates and sensor-cost trajectories.

- Technology deep dives detailing sensor modalities, fusion architectures, algorithmic performance benchmarks, and engineering trade-offs for integration into seats, B‑pillars and overhead modules.

- Regulatory impact assessment mapping IIHS, Euro NCAP and EU GSR test vectors to component and system requirements — with practical compliance checklists for supplier and OEM design teams.

- Go‑to‑market playbooks: OEM procurement timelines, RFP positioning, pricing strategy considerations, and recommended partnership structures for Tier‑1s and specialist vendors.

- Commercial intelligence: validated supplier profiles, capability matrices, and a proprietary assessment of market concentration (top-tier concentration indices), enabling targeted M&A and partnership scouting.

- Implementation blueprints: test-lab setups, validation protocols, and recommended KPIs to measure program readiness against evolving whiplash and occupant classification test regimes.

Using this intelligence in the next 12 months

Leaders who translate insights into executed initiatives in 2026 will secure first-mover advantages as OEMs finalize mid‑cycle platform and safety content updates. Key near-term actions:

- Fast-track validation investments to demonstrate test‑protocol compliance ahead of OEM milestones.

- Execute targeted partnerships or JV discussions to bridge software/hardware gaps without diluting core engineering resources.

- Reassess procurement and cost models to reflect higher electronics content and potential pricing pressure amid semiconductor volatility.

- Prioritize programs where multi‑modal sensing and whiplash protection generate clear regulatory or content uplift, improving win probabilities.

Why PW Consulting

Our analysis blends bottom‑up supplier intelligence, OEM program tracking, and scenario-based financial modeling to deliver recommendations that are immediately actionable for 2026 budgets and program plans. We maintain a neutral, transaction‑oriented perspective that aligns engineering feasibility with commercial viability — enabling clients to prioritize investments, structure partnerships, and position bids with clarity and speed.

Next steps and access

This release is a strategic preview designed to show depth while reserving granular segment-level data and programmable spreadsheets for licensed report access. For procurement teams, corporate development groups, product leaders and investors seeking the full dataset, supplier scorecards and scenario models, PW Consulting invites engagement through our research portal and advisory services. The full report contains the granular tables, OEM program trackers and annexed validation frameworks required to convert insight into executed outcomes.

Contact PW Consulting’s Automotive Safety team to schedule a briefing, obtain tailored forecast extracts, or commission a bespoke workshop that maps the findings to your 2026 roadmap.

For detailed analysis of this topic, please visit the official page:Automotive Occupant Sensing Systems Oss And Whiplash Protection System Wps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com