Pseudoboehmite Market 2026: Strategic Imperatives for Procurement, R&D and M&A — PW Consulting Release

Executive summary

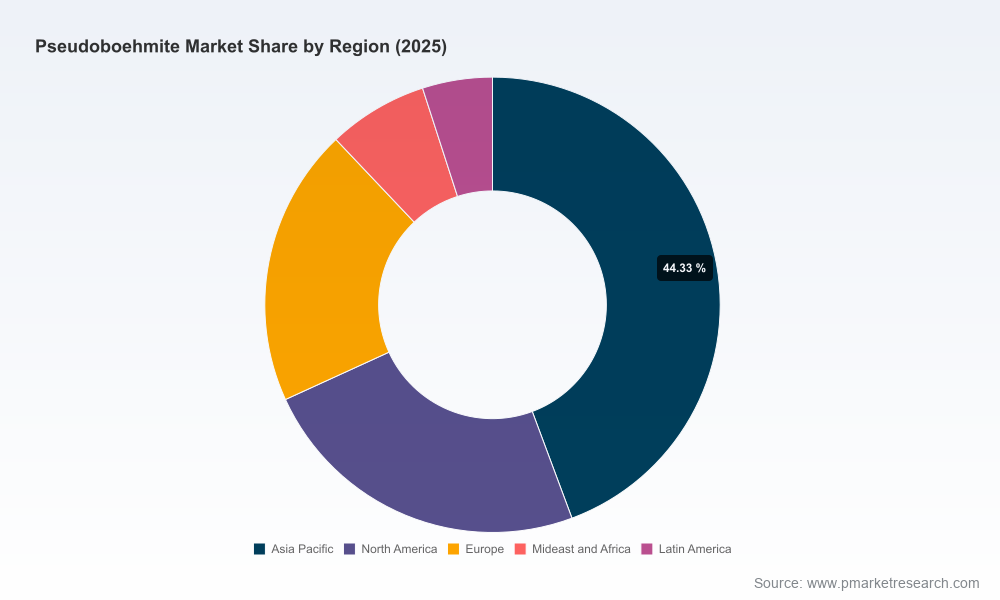

PW Consulting’s newest Pseudoboehmite Market report (base year 2025, forecast 2026–2032) provides a pragmatic, decision-focused roadmap for companies operating across catalyst, adsorbent, refractory and specialty-material value chains. The global market is projected to expand from a 2025 revenue base of approximately 654.6 Million USD to roughly 934.7 Million USD by 2032, representing a compound annual growth rate (CAGR) of 5.22% across the 2026–2032 forecast window. Market concentration remains meaningful—CR3 and CR5 metrics indicate that leading groups retain a substantial share of the value pool—underlining the importance of supplier strategy and partnership selection for buyers and investors alike.

Pseudoboehmite Market

Why this matters for 2026 corporate decision-making

- Procurement: Price volatility in upstream feedstocks and the uneven pace of downstream demand recovery require refined hedging and sourcing playbooks.

- Product strategy: Incremental performance gains in catalyst carriers and adsorbents translate to measurable operational upside for end-users; selecting the right pseudoboehmite grade and supplier can become a competitive differentiator.

- Capacity & M&A: With top-tier producers maintaining significant share, 2026 is a pivotal year for bolt-on acquisitions, JV negotiations and brownfield investments to secure feedstock access and technical IP.

- Compliance & ESG: Certification and environmental permitting are now foundational to commercial scale-up, influencing project timelines and off-take credibility.

Key macro takeaways (high level)

Our synthesis of historical data (2020–2025) and forward-looking scenarios (2026–2032) shows a steadily growing market driven by continued demand in petrochemical catalysts and selected specialty applications. The CAGR of 5.22% reflects structural demand for alumina-based intermediates in refining, gas processing and specialty materials, while also accommodating cyclical pressures tied to upstream commodity cost swings and regional demand variability.

Pseudoboehmite Market

Industry dynamics shaping supplier and buyer strategies

- Raw-material price signals: Aluminum hydroxide and bauxite price trajectories are already reshaping margin profiles for producers and pass-through mechanisms for buyers. For example, recent price moves in Northeast Asia and Europe indicate softer demand and easing feedstock costs; U.S. import indices for bauxite also reflect longer-term input price normalization. These trends materially affect short-term commercial negotiations and longer-term capex planning.

- Capacity upgrades and certifications: Major project approvals and certifications—such as environmental and social impact assessments and ISO accreditations—are accelerating the commercial maturity of larger-volume lines and enhancing bankability of projects seeking export and global supply contracts.

- Concentration and competitive positioning: The market’s CR3 and CR5 levels point to a moderately consolidated supply base where a small number of global and regional producers influence pricing, lead times and technical service levels.

- Downstream sensitivity: Demand from refinery hydroprocessing, adsorbent manufacturers and specialty ceramics remains the single largest aggregate driver; therefore, shifts in refining throughput, petrochemical margins or end-market polymer demand rapidly cascade into pseudoboehmite procurement strategies.

Competitive landscape — what to watch in 2026

Our report profiles legacy multinationals, large integrated producers and specialist regional manufacturers. The competitive battlefield is defined by three vectors: product purity and dispersion capability, scale and geographic reach, and the strength of technical services tied to catalyst formulation or adsorbent conditioning.

Pseudoboehmite Market

- Sasol Limited — Known for high-purity, highly dispersed products (including recognized brands) developed via alkoxide hydrolysis; strong footprint supplying catalyst carriers to petrochemical and refining customers with advanced application support.

- CHALCO / Chalco Shandong Advanced Material — A major integrated player that has recently progressed significant production upgrades (including a major change project for a PHS-series line) and has invested in environmental and social due diligence to support larger-volume hydrocracking applications.

- Honeywell UOP — Offers branded alumina families that span pseudoboehmite and related phases; advantage lies in deep process know-how and tight integration with refining and gas-processing licensors.

- Nabaltec, Almatis, BASF — Specialty and legacy chemical groups supplying tailored grades for flame retardants, catalysts and advanced materials; competitive strengths include technical application development, global marketing networks and quality assurance.

- Regional specialists (e.g., multiple Shandong-based manufacturers, Japan’s Taimei, Russia’s KNT and smaller US-based specialty suppliers) — These vendors compete on cost, niche-grade innovation and proximity to specific end-markets, forming the backbone of regional supply chains.

For buyers and investors, the critical takeaway is to evaluate suppliers not only on price and capacity but also on traceability, technical service capabilities, project accreditations, and contingency plans for raw-material disruptions.

Raw-material and regulatory context

Input-cost dynamics are pivotal. Recent data shows meaningful regional variance in aluminum-hydroxide pricing and continued stability in certain bauxite benchmarks. For procurement teams, this means that forward contracts, regional sourcing diversification and feedstock-linked price clauses must be part of standard contracting playbooks in 2026. Additionally, regulatory and ESG diligence—already a gating factor for large-volume capacity expansions—has become table stakes for project financing and long-term offtake contracts.

Notably, advanced production projects are undergoing environmental and social impact evaluations alongside internationally recognized management system certifications, signaling that compliance milestones will increasingly influence time-to-market and preferred supplier lists.

What the PW Consulting report delivers (practical, actionable content)

Designed as a working tool for strategy teams, procurement leaders, R&D heads and corporate development groups, the report includes:

- Proprietary market-sizing and trend models (historical 2020–2025 and forecast 2026–2032) with flexible scenario toggles to stress-test demand under recessionary, baseline and upside cases.

- Supply-side mapping down to plant level, highlighting recent capacity upgrades, permit statuses and commissioning timelines where publicly available.

- Supplier scorecards combining technical capability, ESG credentials, geographic reach and commercial terms to inform shortlist creation and negotiation strategy.

- A dynamic pricing framework that integrates upstream feedstock indices, freight sensitivity and regional demand elasticity to model price pass-through and margin exposure.

- Strategic playbooks — for procurement (sourcing bundles, hedging), for R&D (grade selection and testing pathways), and for corporate development (M&A screening criteria, JV structures and integration risks).

- Case studies that translate market intelligence into executable actions: e.g., optimizing catalyst carrier sourcing for a refinery turnaround, or structuring a multi-year offtake with embedded quality and volume flex provisions.

To preserve competitive value, the report’s full segmentation tables, application-by-region demand breakdowns, unit price curves and vendor-level volume forecasts are intentionally excluded from this press release and are available only in the primary report.

How to apply these insights in 2026 planning cycles

- Short-term procurement (0–12 months): Lock favorable terms where feedstock pass-through is minimized, use flexible delivery windows and include material substitutions clauses tied to defined performance metrics.

- Medium-term operations & R&D (12–36 months): Prioritize qualification of alternative grades and suppliers; invest in joint-development agreements to co-develop higher-dispersion or lower-impurity products that unlock downstream performance.

- Strategic investments & M&A (18–48 months): Target acquisitions or partnerships that close critical gaps—feedstock security, certified capacity, or proprietary dispersion processes—especially in regions where regulatory approvals are a gating factor.

- Risk & compliance: Build ESG-ready supplier checklists and require third-party verification for any major capacity expansions or greenfield projects to avoid regulatory slippage and reputational risk.

Concluding perspective

The pseudoboehmite market in 2026 sits at the intersection of stable structural demand and evolving supply-side complexity. For decision-makers, the window to act on procurement redesign, technical partnership formation and selective capacity moves is now. PW Consulting’s Pseudoboehmite Market report is structured to convert market intelligence into boardroom-ready decisions—while deliberately withholding granular segmentation tables here to protect the commercial integrity of our clients’ benchmarking exercises.

Next steps

Executives seeking a tailored briefing, supplier heatmaps for a specific geography, or scenario-model access for capital allocation decisions are invited to contact PW Consulting’s advisory team to arrange a confidential strategy session and obtain the full report, which contains the comprehensive datasets and supplier-level analyses referenced above.

For detailed analysis of this topic, please visit the official page:Pseudoboehmite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com