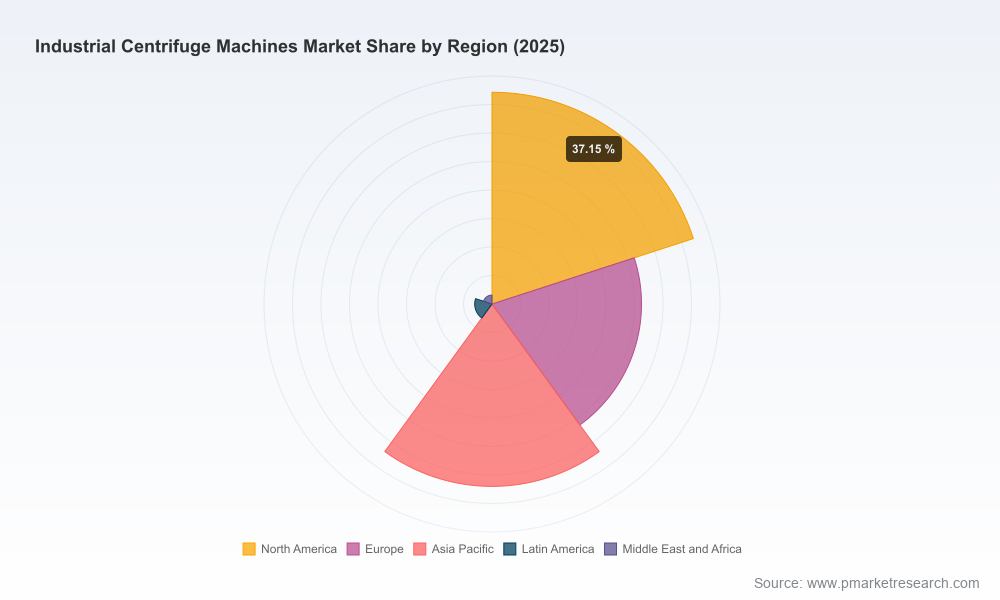

Industrial Centrifuge Machines Market: Strategic Imperatives for 2026 Decision‑Makers

PW Consulting today releases a forward‑looking industry brief accompanying our full Industrial Centrifuge Machines Market study. Synthesizing five years of historical data and a seven‑year forecasting horizon, the study puts the 2025 global market at approximately USD 9.53 Billion and projects compound annual growth of roughly 5.12% across 2026–2032, with the market approaching the mid‑teens in USD billions by the end of the forecast window. This press narrative surfaces the high‑value insights that should shape procurement, product, and M&A decisions in 2026—while reserving detailed segmentation tables, vendor scorecards and proprietary scenario outputs for the full report.

Industrial Centrifuge Machines Market

Why this study matters for 2026 planning

- Translates macro demand trajectories into actionable capital‑planning timelines for OEMs and end users.

- Quantifies the strategic return on digital and product investments (e.g., high‑speed separators, decanter upgrades, condition monitoring) through modeled TCO and payback scenarios.

- Identifies pragmatic levers to mitigate raw‑material and tariff exposure that are already affecting stainless‑steel and nickel supply chains.

- Provides a repeatable procurement playbook for long‑lead equipment with embedded scenario pricing to support multi‑year CapEx approvals.

Market trajectory and principal drivers

The market’s steady expansion from the early‑2020s into mid‑decade reflects durable industrial demand across wastewater treatment, chemical processing, food & beverage, pharmaceutical/biotech and metal/mining applications. Growth is not uniform—technology substitution, regulatory tightening on effluent quality, and accelerated adoption of biotech‑scale centrifugation for alternative proteins and high‑density fermentation are reshaping equipment mix and aftermarket opportunities.

Industrial Centrifuge Machines Market

Key demand drivers observed in our analysis:

Industrial Centrifuge Machines Market

- Application intensification: Higher throughput and tighter separation specifications in bioprocessing and wastewater are shifting procurement toward higher‑specification decanters and disc‑stack separators.

- Service and digitization premium: Smart sensors and condition‑based maintenance are emerging as margin multipliers for suppliers that can offer predictive uptime guarantees and remote service capabilities.

- Cost and supply pressure: Elevated input costs and persistent specialty‑steel volatility are prompting both OEMs and buyers to revisit design choices, material sourcing strategies, and total lifecycle cost (LCC) models.

Market concentration is moderate. The top three and top five vendors together account for a meaningful but not dominant share of global revenue, leaving room for regional specialists, niche OEMs and aftermarket service players to expand through targeted technology or service propositions.

What the full report delivers (practical content preview)

Clients rely on this report for executable outputs, not just observation. The full deliverable includes:

- Transparent market sizing and methodology (historical series, 2020–2025) and scenario‑based forecasts to 2032.

- Capital and operational cost models for typical centrifuge configurations, enabling unit‑level ROI and payback analysis for retrofit vs. greenfield decisions.

- Vendor benchmarking and procurement scorecards with weighted criteria across performance, service footprint, digital readiness, and total cost of ownership.

- Supply‑chain heat maps identifying single‑source exposures for key components and recommended mitigation playbooks (supplier diversification, hedging strategies, near‑shoring triggers).

- Regulatory and ESG impact assessment, with compliance cost estimates and retrofit prioritization for emissions/water‑quality standards.

- Case studies and implementation roadmaps (on‑site trials, skid deployment, factory acceptance testing protocols) drawn from recent projects.

- M&A and partnership screen: targets by capability gap (e.g., smart sensors, process development centers, rental/servitization platforms) and high‑probability integration scenarios.

Competitive landscape—strategic takeaways

Our vendor analysis synthesizes product roadmaps, recent corporate moves, and observable market signals. Highlights for strategic planners:

- Alfa Laval AB (Lund, Sweden) — Maintains leadership through rapid product refreshes aimed at biotech and food processing. Recent launches emphasize high‑speed separators and hermetic designs for sensitive fermentations. Expect Alfa Laval to continue leveraging R&D and aftermarket services to defend premium positions.

- GEA Group AG (Düsseldorf, Germany) — Demonstrating a strategy of capability augmentation through tuck‑in acquisitions and smart‑sensor integration to win in water and wastewater segments. Their approach is instructive for buyers seeking integrated control and analytics with equipment purchases.

- ANDRITZ AG (Graz, Austria) — A strong play in heavy industries and mining, with an emphasis on robust decanter solutions. ANDRITZ is a natural partner for large miners and chemical producers focusing on throughput and abrasive duty cycles.

- Flottweg SE (Vilsbiburg, Germany) — Recent investment in a process center signals a focus on application‑specific validation and shortening sales cycles for complex separations. This capability differentiates vendors that can co‑develop solutions with end users.

- Regional and niche OEMs — Companies such as Western States Machine, Mitsubishi Kakoki Kaisha, FLSmidth, Hiller, Pieralisi and several specialist firms maintain strong footholds in legacy use cases, regional service networks and specific industries (e.g., olive‑oil, sugar, marine). Their agility and local service density are distinct competitive advantages.

Our full vendor scorecards identify specific strengths and improvement areas for each manufacturer—ranging from digital maturity, spare‑parts logistics, service SLAs, to modular product architectures. Those performance differentials inform supplier selection and partnership strategies in the complete report.

Supply‑chain and cost resilience considerations

Input‑cost dynamics and trade policy remain the most immediate operational stressors. Our analysis documents several implications for 2026 planning:

- Design for material efficiency and targeted substitution: Where corrosion resistance requirements allow, alternate alloys or protective coatings can materially reduce bill‑of‑materials cost without sacrificing lifecycle performance.

- Strategic procurement: Multi‑year supply agreements, indexed pricing mechanisms, and dual‑sourcing strategies are effective to insulate CapEx programs from short‑term commodity shocks.

- Local value optimization: For large projects, near‑sourcing critical assemblies can shorten lead times and reduce exposure to tariffs and freight volatility—especially relevant for operators with concentrated production footprints.

Technology and services where to place your 2026 bets

We identify four investment themes with immediate impact on competitiveness and margin:

- Digital retrofits and predictive maintenance: Rapidly convert installed bases into recurring‑revenue service platforms using non‑intrusive sensors, edge analytics and remote diagnostic services.

- High‑throughput, high‑density separators: Capital investments in these designs unlock value across bioprocessing and alternative‑protein production—an area already showing product activity from lead OEMs.

- Modular, skid‑based solutions: Shorter lead times and easier commissioning reduce project risk for EPCs and strategic buyers; suppliers that standardize modular offerings can accelerate penetration.

- Servitization and rental models: For customers with project‑level variability, equipment‑as‑a‑service can turn CapEx into predictable Opex while giving OEMs higher lifetime value per installed unit.

Six strategic recommendations for executives

- For OEMs: Prioritize digital service offerings and process validation centers; product differentiation will increasingly be delivered as combined hardware+service propositions.

- For procurement leads: Institute LCC procurement rules that incorporate spare‑parts availability, remote‑service capability and upgrade paths, not just initial price.

- For investors: Screen targets for aftermarket revenue potential and digital maturity—these attributes materially affect multiple valuation levers.

- For plant operators: Run pilot digital retrofits on high‑value trains first to build the business case for broader rollouts and to validate OEE improvements.

- For strategic planners: Scenario‑proof CapEx by stress‑testing projects against commodity and tariff scenarios; our scenario outputs speed this through quantified P&L impacts.

- For M&A teams: Prioritize tuck‑ins that add complementary service capabilities (process centers, analytics platforms, rental fleets) over broader horizontal scale in a fragmented market.

Concluding guidance and next steps

Industrial centrifugation is no longer a purely mechanical procurement decision. In 2026, success will accrue to organizations that combine equipment selection with digital services, supply‑chain resilience, and a clear roadmap for lifecycle cost reduction. PW Consulting’s full report delivers the segment‑level granularity, vendor scorecards, and executable playbooks necessary to convert these strategic imperatives into measurable outcomes. Because our aim is to equip decision‑makers, the complete set of detailed segmentation tables, proprietary unit‑cost models and vendor benchmarks are accessible in the paid report.

To access the full intelligence package including downloadable models, supplier checklists and tailored advisory options, please visit PW Consulting’s Industrial Centrifuge Machines Market page or contact our strategy team for a briefing and bespoke scenario analysis.

For detailed analysis of this topic, please visit the official page:Industrial Centrifuge Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com