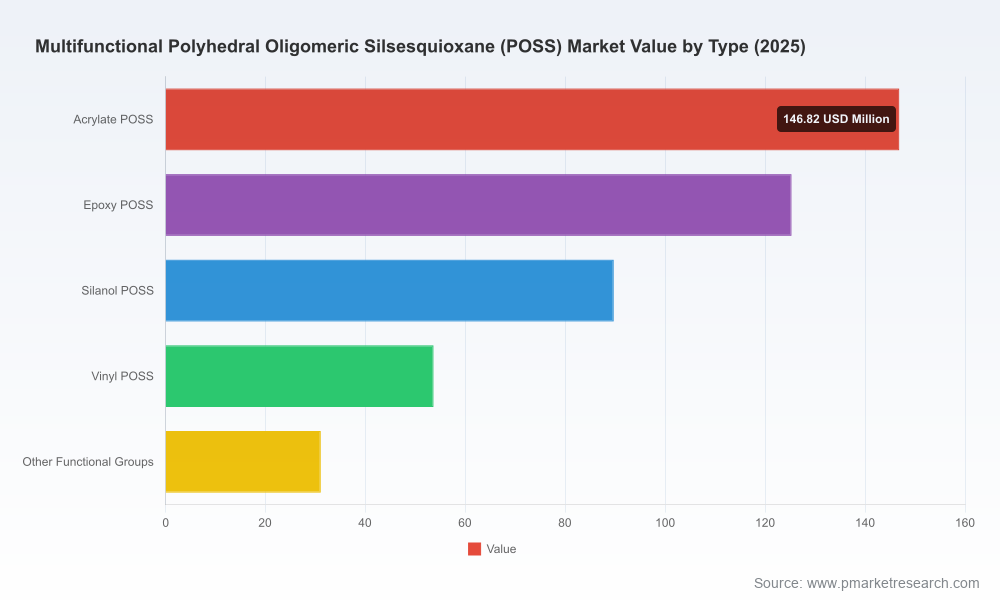

Multifunctional Polyhedral Oligomeric Silsesquioxane (POSS) Market — Strategic Intelligence to Shape 2026 Corporate Decisions

PW Consulting today releases an executive briefing drawn from our new full-length market research report on Multifunctional Polyhedral Oligomeric Silsesquioxane (POSS). Designed as a strategic playbook for corporate leaders, investors, and R&D heads, this briefing highlights the report’s unique value for decisions you must make in 2026 — from capital allocation and M&A screening to product roadmaps and sourcing strategies. The analysis blends rigorous market-sizing with supplier-level insight and practical, executable recommendations while deliberately withholding the granular subsegment tables reserved for the full report.

Multifunctional Polyhedral Oligomeric Silsesquioxane Poss Market

Why this report matters for 2026

POSS has moved from a specialty laboratory curiosity toward a commercial material platform with clear application-led traction. Between 2020 and 2025 the global POSS market expanded materially, and our base-year assessment (2025) frames the sector at the cusp of broader industrial adoption. Our forecast through 2032 incorporates a compound annual growth rate of 9.55%, reflecting both continued technology maturation and multiple adoption pathways across coatings, electronics, aerospace, biomedical and polymer systems.

Multifunctional Polyhedral Oligomeric Silsesquioxane Poss Market

For 2026 decision-makers, this momentum translates into distinct strategic imperatives:

Multifunctional Polyhedral Oligomeric Silsesquioxane Poss Market

- Prioritize supplier and feedstock security: as volumes rise, downstream manufacturers will need robust commercial contracts to de-risk production ramps.

- Accelerate application de-risking: the next 12–18 months are the critical window to convert laboratory formulations into validated industrial-scale offerings.

- Recalibrate pricing and commercial models: historical scale-up has already driven cost improvements; firms should adopt dynamic procurement and tiered pricing linked to volume exposure.

- Refine M&A and partnership criteria: early exposure to multifunctional POSS confers barrier-to-entry benefits—target selection should emphasize manufacturing scale, IP ownership, and customer validation.

What the PW Consulting report delivers (operational content)

The full report is structured to be a working guide for strategy and execution. Highlights include:

- Market sizing and growth dynamics: a verified historical series and a forward-looking model through 2032, enabling scenario stress-tests for strategic planning.

- Segment-level demand drivers (by functionality, application cluster, and region) with ranked growth levers and adoption inhibitors—note: the briefing intentionally omits granular subsegment tables to preserve the full report’s value.

- Supply-side mapping: supplier capacity maps, synthesis route comparisons (organosilane vs silica-based feedstocks), and a timeline of Chinese capacity expansions impacting global availability.

- Commercial intelligence: customer procurement profiles, pricing benchmarks, and negotiation playbooks for volume contracts and long-term supply agreements.

- Technology and product roadmaps: maturity matrices for major POSS chemistries, scale-up risk matrices, and a three-tier R&D prioritization framework.

- Regulatory and safety assessment: implications of non-halogenated flame retardant positioning, environment-health-safety (EHS) considerations, and compliance checklists for regional standards.

- M&A and partnership toolkit: acquisition screening filters, synergy quantification templates, and an actionable shortlist methodology for targets aligned to scale and IP ownership.

- Financial models and worksheets: modular Excel models for revenue, margin and capex planning that you can adapt to internal assumptions and procurement scenarios.

Competitive landscape — strategic takeaways

The POSS supplier ecosystem is a mixture of legacy innovators, regional volume players, and specialist distributors. Our analysis emphasizes strategic positioning rather than absolute market shares, while the report quantifies concentration at the market level (top 3 firms control a meaningful majority and the top 5 an even larger share, underscoring a moderate-to-high concentration environment that affects pricing leverage and M&A dynamics).

- Hybrid Plastics, Inc. — As the original creator and a primary manufacturer of POSS materials, Hybrid Plastics retains advantages in proprietary chemistry, breadth of multifunctional grades and an entrenched R&D customer base. For licensors and OEMs, their portfolio represents a low-friction path to scale-tested variants.

- Qingdao Hengda Chemical / Hengda Silane — With manufacturing capacity in China, Hengda exemplifies the regional scale playbook: cost-competitive production and close integration with upstream silicon chemistry expansions. For buyers prioritizing volume and competitive pricing, suppliers with integrated Chinese manufacturing demand attention.

- Baoxu Chemical — Specialist positioning in flame retardant grades and heat/hydrolysis-resistant variants makes Baoxu a high-value partner for polymer formulators chasing regulatory-compliant, non-halogen solutions.

- Merck KGaA, Gelest, Alfa Chemistry and others — These organizations serve as critical distribution and research-grade channels, accelerating adoption among laboratory users and specialty formulators. Their role in enabling sample-to-scale transitions is frequently underestimated.

- Smaller suppliers and regional players — A diverse set of niche producers and distributors can provide rapid prototyping access, local regulatory navigation and lower minimum order quantities, useful in early-stage application validation.

Strategic implication: buyers and investors should calibrate partner selection to intended pathways. If route-to-market depends on rapid volume, prioritize suppliers with established capacity and integrated feedstock exposure. If product differentiation and IP control are critical, opt for firms with deep R&D heritage and proprietary chemistries.

Supply chain, raw materials and regulatory tailwinds

POSS synthesis remains rooted in silicon chemistry — typically produced via hydrolytic condensation of organosilanes or silica-based feedstocks. Recent capacity expansions in China have meaningfully influenced cost curves and availability, supporting the transition from niche to commercial-scale deployments. Historical scale-up has already driven price improvements, and our models anticipate further cost reductions as adoption broadens.

On the regulatory front, POSS’s high thermal stability and role as a non-halogenated flame retardant align well with evolving environmental standards in polymers and coatings. This positioning creates a durable demand vector in sectors where halogen-free solutions are mandated or preferred, such as electronics and select industrial end-markets.

Scenarios and risks for 2026–2028

We model three primary scenarios that managers should incorporate into 2026 planning cycles:

- Base Case (Core forecast) — Continued steady adoption with the market growing inline with the 9.55% CAGR embedded in our central model. Suppliers with ready-to-scale production capture the initial commercial volumes.

- Accelerated Adoption — Regulatory accelerants and breakthrough performance demonstrations (e.g., in electronics encapsulation or aerospace composites) drive faster penetration, favoring vertically integrated producers and prompting earlier consolidation.

- Constrained Supply / Feedstock Shock — Upstream silicon feedstock shortages or trade disruptions introduce price volatility and project delays; buyers with diversified sourcing and hedging strategies maintain advantage.

Top risks to monitor include: feedstock price volatility, alternative chemistries that could displace specific POSS variants, and uneven quality control during rapid scale-up. Our report provides mitigation playbooks (contract structures, dual-sourcing templates, and qualification milestones) tailored to each scenario.

Actionable recommendations for executives in 2026

- Embed POSS into product roadmap pilots now: prioritize two high-value applications for 2026 piloting to capture early adopter advantage and to inform pricing strategies.

- Negotiate staged supply agreements: combine capacity reservation with performance-based pricing to align supplier incentives during scale-up.

- Pursue strategic partnerships with distribution and formulation specialists to shorten commercialization cycles in regulated industries.

- Scan for targeted acquisitions selectively: prioritize assets that provide immediate capacity, proprietary functional groups or validated OEM contracts rather than speculative technology bets.

- Invest in downstream validation labs and accelerated aging protocols to reduce time-to-specification and to strengthen claims for marketing and regulatory submissions.

What we intentionally hold for the full report

Consistent with the “trailer” principle, this briefing highlights the strategic contours and the operational value of our analysis while reserving the full dataset and subsegment tables for the comprehensive report. The full deliverable includes:

- Granular regional and application-by-type demand tables and forecast curves

- Supplier scorecards with capacity, product catalogs and qualitative strength/weakness matrices

- Complete financial models and scenario worksheets in editable format

- Appendices with primary-source interview notes and supplier contact lists

Access to these materials provides the empirical foundation required for binding commercial decisions and M&A diligence. The summary here is designed to establish credible context and immediate next steps, and to motivate retrieval of the full intelligence set for transaction-level or operational execution.

Conclusion — the strategic edge for 2026

Multifunctional POSS is no longer an experimental material; it is a modular technology family presenting multiple entry points for value capture across coatings, polymers, electronics, and high-performance composites. With the market demonstrating sustained expansion and a forecast CAGR of 9.55%, 2026 is the year to convert strategic intent into commercial action. Whether your priority is securing feedstock, accelerating product certification, or sourcing acquisition targets, the decisions you make in 2026 will materially shape competitiveness through the end of the decade.

PW Consulting’s full report equips executives with the data, vendor insights and execution tools required to make those decisions with confidence. For access to the complete dataset, supplier scorecards, and operational templates, please visit our report page to request the full deliverable and accompanying analyst support.

For detailed analysis of this topic, please visit the official page:Multifunctional Polyhedral Oligomeric Silsesquioxane Poss Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com