Maskless Lithography Systems for Semiconductor Packaging: Strategic Imperatives for 2026 Decision-Makers

As semiconductor packaging evolves from incremental optimization to architectural reinvention, maskless lithography is moving from niche prototyping to a foundational enabler of heterogeneous integration, chiplets and high-performance compute packaging. PW Consulting’s latest market study — released with a 2025 base and a 2026–2032 forecast horizon — quantifies this shift and translates it into actionable guidance for corporate leaders, investors and engineering heads planning capex, partnerships and product roadmaps in 2026.

Maskless Lithography System For Semiconductor Packaging Market

Why 2026 is a Pivotal Year

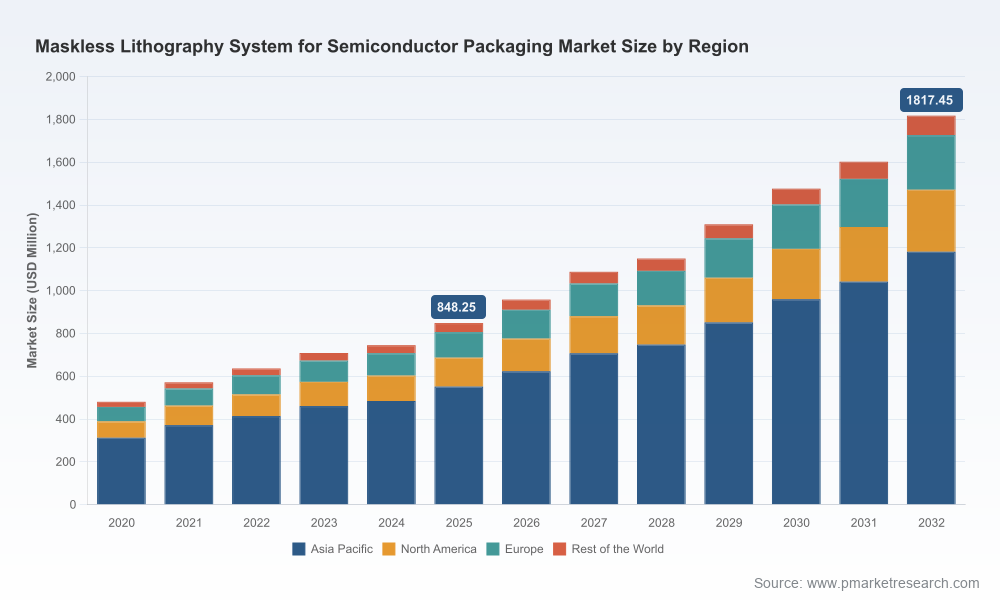

Our analysis shows the market entering an accelerated phase of commercial adoption. From an established base in 2025, the addressable market is forecast to expand at a compound annual growth rate of 11.48% over the 2026–2032 period, reaching new scale by the end of the forecast window. That trajectory reflects a convergence of several inflection points: chiplet-driven multi-die assemblies, panel-level ambitions to lower per-unit cost, and back-end process innovations that increasingly demand maskless flexibility to address die shift, substrate warpage and large-substrate patterning.

Maskless Lithography System For Semiconductor Packaging Market

What the Report Delivers (Practical, Executable Intelligence)

- Clear market sizing and scenario modeling — with base-year calibration and upside/ downside scenarios tied to adoption curves, yield improvements and throughput scaling assumptions.

- Technology roadmap and feature prioritization — mapping laser direct imaging (LDI), spatial light modulators (SLM), digital micromirror devices (DMD) and hybrid approaches to packaging use-cases and throughput thresholds.

- Vendor benchmarking and capability heat maps — not only head-to-head equipment specs, but also real-world indicators: integration readiness, field service footprint, software/toolchain maturity, and systems-level integration for hybrid bonding and inspection.

- Go-to-market playbooks — procurement timing, pilot-to-production gating criteria, supplier qualification checklists, and contract terms optimized for mixed-volumes and evolving process windows.

- Supply chain and geopolitical risk matrix — practical mitigations for export control friction, secondary sourcing strategies, and inventory/capacity playbooks for 2026–2028.

- Investment and M&A signal framework — value drivers for strategic acquisition or minority investments, with capital allocation templates showing expected payback ranges and tech-de-risk milestones.

Macro Drivers and Dynamics Shaping Adoption

- Heterogeneous integration and chiplet architectures: Maskless systems uniquely address the need for late-stage design changes, localized reticles and die-shift compensation — features essential when assembling diverse die types on a single substrate.

- Panel-level economics vs. wafer-level engineering: The industry’s push to larger substrates raises new distortion and warpage challenges; maskless digital exposure with on-the-fly correction reduces mask inventory and accelerates cycle time for design iterations.

- Throughput scaling and manufacturing readiness: Recent commercial introductions and throughput-focused upgrades indicate that maskless platforms are moving from low- to mid-volume production viability toward broader high-volume manufacturing applicability.

- Environmental and operational cost considerations: Solid-state light sources and SLM-based architectures lower recurring mask costs, reduce chemical waste associated with mask management and simplify changeover—an increasingly important factor for sustainability targets and TCO calculations.

Competitive Landscape: Who Matters and Why

The competitive landscape is defined by specialist lithography vendors, established capital-equipment integrators, and regionally strong suppliers. The full report includes a vendor scorecard with quantified capability indices; below we summarize strategic positioning and actionables for 2026.

Maskless Lithography System For Semiconductor Packaging Market

- Heidelberg Instruments (Heidelberg, Germany) — Offers mature maskless aligner platforms tailored to wafer-level packaging with strong die-shift compensation and mid-to-high volume configurability. Strategic implication: ideal partner for OEMs seeking controlled scale-up with proven alignment workflows; consider pilot programs to validate integration with existing back-end lines.

- EV Group (EVG) (St. Florian, Austria) — Focused on high-throughput maskless exposure and stitch-free full-wafer patterning; recent highlights underline strong throughput roadmaps for heterogeneous integration. Strategic implication: shortlist for chiplet and panel-level pilots where throughput is a primary gate for adoption.

- Nikon Corporation (Tokyo, Japan) — Introduced a digital lithography system targeted to large substrates and advanced packaging, emphasizing high-resolution SLM projection and warpage correction. Strategic implication: valuable where sub-micron L/S and large-field projection must be reconciled with existing process control environments.

- SCREEN Holdings (Kyoto, Japan) — Delivers LDI and maskless systems oriented toward IC package substrates with a balance between resolution and throughput. Strategic implication: consider for 5G and IoT packaging lines where throughput at modest resolution is prioritized.

- SÜSS MicroTec, In-Vision, Applied Materials (with partners), and regional players — These suppliers add differentiated approaches — from specialty projection optics to digital light engines and large-glass patterning solutions — offering choices across the resolution/throughput/tco spectrum. Strategic implication: evaluate hybrid sourcing strategies to de-risk supply and capture niche capability.

Recent Market Movements to Watch

- Nikon’s commercial availability announcements have moved the technology closer to mainstream procurement cycles, prompting OEMs to revisit procurement timelines and qualification programs.

- EVG’s public throughput claims and trade-show demonstrations signal that vendors are prioritizing HVM throughput scaling, which has knock-on effects for line-capacity planning and FAB-to-back-end co-optimization.

- Heidelberg’s application-focused updates underscore an emphasis on field-proven corrections for die shift and warpage — exactly the pain points cited by advanced packaging integrators.

Actionable Recommendations for 2026

For executives deciding on strategy this year, the report crystallizes a small set of high-impact moves that balance speed-to-adoption with risk control:

- Initiate dual-track qualification: run parallel technical pilots with at least two architecture approaches (e.g., SLM/DMD vs. LDI) to compare yield sensitivity, changeover time and software ecosystems under your specific substrates and die mixes.

- Time capital deployment to throughput inflection points: prioritize investments in lines where vendor roadmaps show clear, validated throughput gains rather than speculative performance claims. Use milestone-based capex tranches tied to vendor delivery and acceptance tests.

- Lock in upstream and downstream integration partnerships: secure co-development or early-access engineering arrangements with pick vendors to align correction algorithms, metrology integration and process recipes before broader roll-out.

- Build supply-chain redundancy for critical modules (SLMs, light engines, projection optics): the industry is still maturing; second-source plans and spare-part strategies materially reduce disruption risk.

- Embed regulatory and export-control scenarios into supplier selection: choose vendors and contractual terms with contingency for cross-border servicing and parts shipment constraints.

- Use the report’s M&A signal matrix: consider bolt-on acquisitions of software IP (alignment/compensation algorithms) or minority stakes in regional vendors that deliver feedstock to your manufacturing geography.

How the Report Helps Executives De-Risk Decisions

Beyond headline sizing, the strength of the PW Consulting study is its linkage between quantified growth scenarios and operational decision points. We translate a market CAGR and adoption curve into procurement timing, FTE and tooling cost implications, and ROI sensitivity to yield improvements and throughput scaling. The report provides a prioritized checklist of qualification tests and a supplier-readiness rubric that procurement and engineering teams can apply out of the box.

Governance, Sustainability and Compliance Considerations

Maskless technologies bring operational sustainability benefits — reduced mask waste and simplified changeover — but they also concentrate dependency on advanced optical modules and software ecosystems. Our regulatory and compliance chapter outlines export-control risk scenarios, recommended clauses for service-level agreements, and sustainability KPIs to include in vendor scorecards.

Conclusion — Strategic Value for 2026

For companies making strategic choices in 2026 — whether expanding packaging capacity, pivoting to chiplet-enabled products, or seeking defensive supply assurance — maskless lithography represents both an opportunity to shorten time-to-market and a new axis of supplier dependency. PW Consulting’s report converts market-scale forecasts (anchored to 2025 baselines and a clear CAGR for the 2026–2032 window) into procurement timetables, vendor selection frameworks and investment staging that executives can operationalize immediately.

Next Steps

To access the detailed segmentation, regional and application breakdowns, vendor scorecards with capability indices, and the step-by-step procurement playbooks referenced above, please consult the full PW Consulting report. The report contains the granular data and templates your teams will need to translate strategic intent into executable programs in 2026.

For detailed analysis of this topic, please visit the official page:Maskless Lithography System For Semiconductor Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com