Production of Lentiviral Vectors Market — Strategic Briefing for 2026 Decision-Makers

PW Consulting’s latest market study on the Production of Lentiviral Vectors (base year 2025, forecast 2026–2032) synthesizes commercial, technical and regulatory intelligence to equip executives making investment, sourcing, and partnership decisions in 2026. At a macro level, the market reached approximately USD 1,340.4 Million in 2025 and is forecast to expand to more than USD 4,403.1 Million by 2032, reflecting a compound annual growth rate (CAGR) of 18.52%. This briefing highlights the strategic takeaways from the full report, outlines actionable playbooks for different stakeholders, and previews competitive dynamics — while deliberately reserving our full segment-level modelling and proprietary scores for subscribers.

Production Of Lentiviral Vectors Market

Why this market matters in 2026

Lentiviral vectors (LVVs) sit at the operational heart of many cell and gene therapy (CGT) programmes, particularly autologous and allogeneic CAR-T approaches and several in vivo gene therapy efforts. As clinical pipelines mature toward late-stage studies and commercial launches, demand for GMP-grade LVVs is moving from episodic, project-based engagements to predictable, high-volume supply contracts. That transition underpins the strong mid-to-long-term growth profile and creates a clear strategic inflection point for manufacturers, CDMOs, biotechs and investors.

Production Of Lentiviral Vectors Market

Market dynamics shaping near-term decisions

- Demand surge versus capacity build-out: The growth trajectory embedded in our forecast is driven by convergent forces: increasing numbers of late-stage CGT assets, higher per-patient vector requirements for some programmes, and broader geographical rollouts. Organisations must reconcile accelerating demand with lead times for regulated manufacturing capacity expansion.

- Raw material economics: Our cost modelling confirms that plasmid DNA remains a dominant contributor to LVV production material costs; peer-reviewed analyses show GMP-grade plasmids account for a substantial share of upstream raw material spend. Transient four-plasmid transient transfection workflows continue to be widely used today, keeping plasmid dependency high, while investments in stable producer cell lines are accelerating as a route to materially reduce plasmid exposure.

- Regulatory evolution: Recent regulatory shifts are meaningful. In 2026, US regulators signalled more flexibility around manufacturing and control strategies to enable innovation in early-phase CGT studies, while reinforcing expectations that analytical methods must be demonstrably fit-for-purpose at IND initiation and progressively qualified for later phases. This combination rewards sponsors and CDMOs with robust CMC strategies and adaptive analytical platforms.

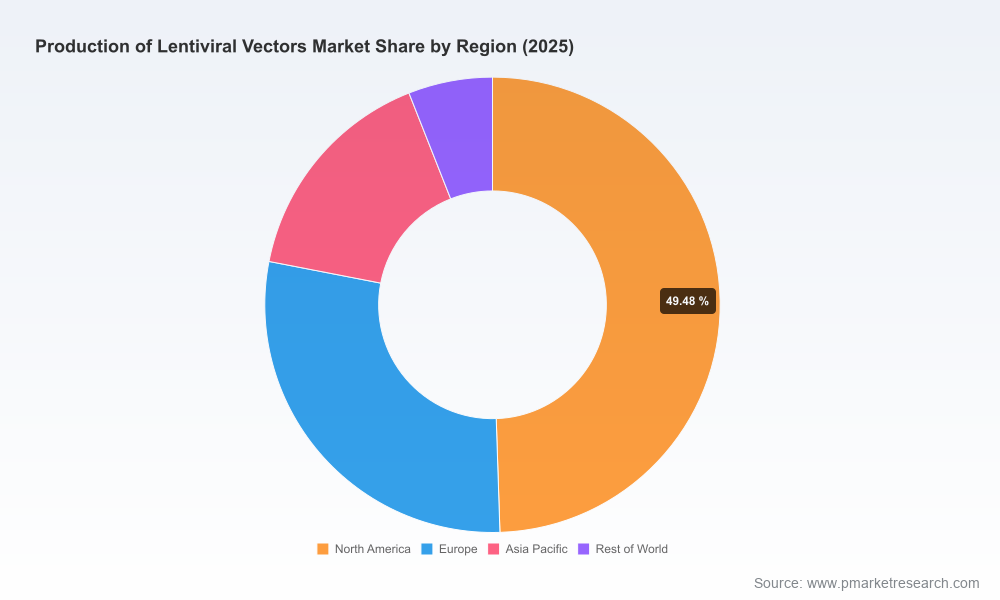

- Concentration and competitive windows: The market exhibits moderate concentration among top suppliers, with the three largest players accounting for a material share of capacity and the top five being a clear influence in pricing and supply dynamics. This creates strategic space for specialist regional and niche players to secure programmes through speed, technical differentiation or contractual structuring.

Competitive landscape — what we found

Our competitor assessment categorises providers across four archetypes: global multi-service CDMOs, regional full-service players, specialised LVV-only CDMOs, and vertically integrated clinical manufacturing platforms. Representative firms across these archetypes include established global CDMOs that offer end-to-end portfolios, and specialised players that focus exclusively on LVV excellence.

Production Of Lentiviral Vectors Market

- Global multi-service CDMOs: Large, integrated operators provide scale and cross-therapy experience, helping sponsors de-risk global supply chains and complex fill-finish logistics. They are positioned to capture large, multi-national commercial contracts given their geographic footprint and regulatory track records.

- Regional and specialist CDMOs: Several Europe- and US-based specialists deliver focused LVV capacity and often differentiate through facility design, rapid turnaround, and bespoke process development services. These players are attractive to companies seeking agility or regional supply redundancy.

- New capacity entrants: Recent facility openings and acquisitions have shifted the competitive map. Notable commercial developments in the recent 18 months — including strategic facility acquisitions, new manufacturing centre openings, and supply agreements — are already influencing procurement strategies and pricing expectations.

Key company examples (non-exhaustive) illustrate how strategy translates into market advantage: established CDMOs with global footprints and multiple validated facilities can underwrite large-scale commercial supply; specialised LVV-only firms compete on technical depth and facility availability; and emerging entrants are leveraging greenfield capacity to win early-stage and regional business. The full report contains a vendor scorecard, capacity tracker, and win-loss analysis that map these strengths to pipeline needs.

Recent deal activity and operational signals to watch

- Multi-year commercial supply agreements and acquisitions of commercial-scale sites point to a shift from trial-oriented work to recurring, higher-volume manufacturing commitments.

- Flagship facility openings and scheduled service launches demonstrate how timing of capacity availability will be a gating factor for programme timelines in 2026.

- Academic–industry collaborations on CAR-T LVVs and expanded service toolboxes at specialised facilities reveal where innovation and practical scale-up know-how are concentrated.

What the report provides — practical deliverables

Designed as an operational playbook for 2026, the report delivers:

- Macro market sizing and trend narratives from 2020–2032, with scenario cases calibrated to regulatory and technology inflection points.

- A capacity and utilisation tracker (live to 2025, with 2026 build-out timelines) that flags potential shortfalls and geographical supply imbalances.

- Supplier matrix and procurement negotiation templates, including term-sheet checklists for capacity reservation, quality release criteria, and tech-transfer milestones.

- Technology and cost models comparing transient transfection versus stable producer cell lines, with sensitivity analyses on plasmid pricing, yield improvements and downstream recovery.

- Regulatory scenario planning: staged CMC decision trees aligned to IND, pivotal, and commercial phases to support risk-adjusted manufacturing strategies.

- M&A and partnership screening tools: quick STP (strategic-thesis-qualification) frameworks to evaluate bolt-ons, greenfield builds or tolling agreements.

- Investment and ROI templates for capex decisions, including break-even horizons and demand thresholds for commercial-scale facilities.

Actionable strategies for 2026 stakeholders

- For pharma and biotech sponsors: Prioritise CMC readiness and early alignment with CDMOs on analytical strategy. Secure medium-term capacity via flexible offtake arrangements (options, capacity rights) while qualifying redundant suppliers for late-stage programmes. Evaluate early investments in plasmid supply agreements or in-staff plasmid production partnerships to insulate programmes from material cost volatility.

- For CDMOs and manufacturers: Differentiate through validated analytical platforms, demonstrated regulatory dossiers, and flexible commercial models (e.g., guaranteed throughput with performance-based pricing). Where feasible, pursue selective scale-up through acquisitions or greenfield builds timed to programme cliffs rather than speculative capacity expansion.

- For investors and private-equity sponsors: Look for targets with proven scale-up track records, defensible client pipelines, and technical differentiation (e.g., robust analytics, stable cell-line platforms). The current competitive structure favours roll-up strategies that combine regional specialists into capable global networks.

Risks and red flags

- Over-reliance on transient plasmid supply without transition pathways to less plasmid-intensive workflows.

- Underestimating regulatory timelines for analytical method qualification and facility readiness in pivotal programmes.

- Capacity misalignment arising from optimistic commercial ramp assumptions — especially where new capacity comes online after programme milestones.

- Concentration risk where a small number of suppliers hold pivotal slots for key programmes.

How to use this intelligence in 90, 360 and 1,000 day plans

- 90 days: Conduct a CMC and supplier stress-test for priority programmes; secure interim plasmid and fill-finish capacity; assemble regulatory gap list for analytical readiness.

- 360 days: Finalise medium-term offtake agreements or capacity expansion plans; implement cost-savings pilots (plasmid pooling, yield improvements); begin tech transfer to secondary supplier(s).

- 1,000 days: Execute strategic capacity builds or acquisitions if warranted by pipeline and contracted demand; transition high-volume programmes to optimised manufacturing platforms (e.g., stable cell lines) and migrate analytical assays to validated, scalable workflows.

Where this briefing points next

PW Consulting’s full report contains the proprietary segmentation tables, facility-level capacity maps, vendor performance scores and deal-playbook templates that are intentionally omitted here to preserve client value and to encourage direct engagement. These hidden deliverables include granular modelling by workflow, application and region that underpin the headline growth pathway and concentration metrics presented above.

For organisations that must make near-term manufacturing commitments or capital allocation decisions in 2026, this report functions as both a risk-mitigation manual and a commercial playbook. To access the complete dataset, scenario models and supplier scorecards, please visit PW Consulting’s report page or contact our industry team for a tailored executive briefing.

For detailed analysis of this topic, please visit the official page:Production Of Lentiviral Vectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com