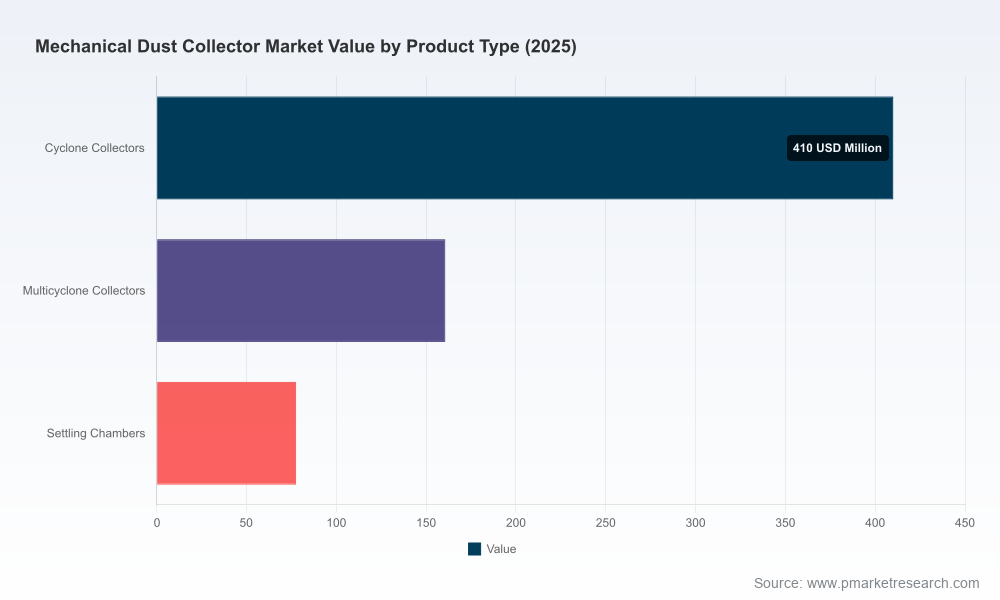

Mechanical Dust Collector Market: Strategic Imperatives for 2026 — PW Consulting Insights

PW Consulting today publishes a forward-looking briefing drawn from our comprehensive Mechanical Dust Collector Market report (base year 2025, forecast 2026–2032). The market reached roughly USD 648.2 Million in 2025 and is projected to grow at a compound annual growth rate of approximately 4.8% through 2032, when the model points to an overall market approaching USD 900 Million. These headline metrics frame a sector in which regulatory pressure, materials-cost volatility, and rapid product innovation converge to create both risk and opportunity for manufacturers, systems integrators, end users and investors.

Mechanical Dust Collector Market

Why this analysis matters for 2026 decision-making

- Regulatory-driven capex cycles: Stricter emission and safety standards are forcing near-term upgrades and retrofits. Facilities that delay compliance-oriented investments risk operational interruptions and higher retrofit costs.

- Cost-structure sensitivity: Rising fabrication input costs and higher maintenance labor rates are compressing margins for OEMs that cannot pass through inflation or capture aftermarket service revenue.

- Technology differentiation: Advances in filter media, cartridge designs and energy-efficient cyclone architectures are creating new performance tiers—and price premiums—within a historically commoditized product set.

- M&A and consolidation potential: Low concentration at the top of the market is creating a fertile environment for strategic acquisitions and roll-ups aimed at scale, service networks and proprietary technologies.

Market dynamics shaping 2026 strategies

- Compliance intensity: Regulatory updates, including stringent emission standards that mandate near-total particulate capture for specific metal-processing applications, are accelerating replacement cycles and premium-system demand.

- Safety as a purchase driver: Combustible-dust directives and explosion-proof requirements are not just compliance items; they are value drivers that justify upgrades, engineering services, and certification-related premiums.

- Raw material and labor pressures: Fabrication-cost inflation and rising technician wages are altering supplier economics—shifting ROI calculations toward designs that minimize installed steel, lower service frequency, or enable remote/automated cleaning.

- Product innovation: Expect continued emphasis on compact cartridge systems, high-efficiency pleated media, and energy-optimized cyclone geometries, plus smarter controls and predictive maintenance offerings to reduce lifetime cost-of-ownership.

Competitive landscape — what differentiates winners in 2026

The mechanical dust collector market combines legacy OEMs serving heavy industry with niche players focused on high-efficiency or custom applications. Market concentration remains relatively low, reflecting a fragmented ecosystem of regional vendors, specialty fabricators and international groups. This structure creates tactical windows for both organic growth and acquisitive scale.

Mechanical Dust Collector Market

- Donaldson Company, Inc. (Torit brand) — A broad product portfolio and deep channel relationships make Donaldson a go-to supplier for large industrial customers. Strengths: scale, filter-media R&D, and brand trust in metal and woodworking markets. Recent trade-show activity highlights iterative performance upgrades for metal-fabrication workflows.

- Camfil APC — Differentiates on cartridge and pleated-media technologies, explicitly targeting pharmaceutical and food-grade environments where filtration efficiency and hygiene certification command premiums. Recent product launches emphasize higher-efficiency pleat geometries for fine particulates.

- Nederman — Strong in localized capture and welding-fume solutions, pairing cyclonic separation with smart cleaning systems. The firm’s trade-show activity underscored energy-efficiency as a primary selling point for industrial customers.

- RoboVent — A specialist in high-efficiency collectors tailored to automotive and aerospace, leveraging modular, compact designs and high-performance filtration media. Its positioning favors OEMs and Tier 1 suppliers that prioritize particle control in tightly controlled manufacturing environments.

- Wheelabrator (Archetype) — Focuses on surface-prep and abrasive-blast applications, where reverse-pulse baghouse and cartridge solutions must withstand dust with high abrasive loading.

- Ceco Environmental (Peerless) — Offers systems designed for high-temperature and heavy-duty processes—an important niche for cement, steel and power-generation customers.

- Schust Engineering & Aget Manufacturing — Represent the custom and agricultural/woodworking ends of the market, respectively, and demonstrate the ongoing relevance of bespoke engineering and localized manufacturing footprints.

Together, these vendors illustrate market segmentation along product robustness, regulatory certification, aftermarket service capability and technical specialism. The competitive playbook for 2026 will reward firms that combine product performance with service-led revenue models and certification-backed value propositions.

Mechanical Dust Collector Market

What the PW Consulting report delivers (practical, actionable content)

- Data-driven market modelling: Historical base (2020–2025) and scenario-based forecasts (2026–2032), with sensitivity tables for steel-price and labor-rate inputs that materially affect unit economics.

- Decision frameworks: Buyer personas, procurement RFP templates and a compliance-risk matrix to accelerate capital-allocation and specification decisions.

- Competitive playbooks: Supplier scorecards, go-to-market archetypes, and an acquisition-target screener tuned to scale, technology and service-network gaps.

- Operational tools: Capex sizing guides, expected payback windows for retrofit vs. replacement, and a maintenance-cost calculator to support lifecycle-cost comparisons.

- Scenario analysis: Upside and downside pathways driven by policy enforcement timelines, input-cost inflation and acceleration of aftermarket-service models.

To preserve competitive advantage, we present high-level segmentation insights and strategic implications here while reserving full region-, product- and end-use breakouts for the report package and accompanying data workbook.

Strategic recommendations for 2026

- Prioritize compliance-enabled solutions: For OEMs and integrators, develop certified packages that simplify end-customer compliance journeys—bundled engineering, installation and certification services command higher margins.

- Expand aftermarket and service offerings: With labor and certification costs rising, recurring maintenance contracts and predictive-maintenance subscriptions are critical to stabilizing revenue and offsetting new-equipment cyclicality.

- Invest in filter-media and energy outcomes: Innovation that demonstrably lowers energy consumption or extends service intervals will win procurement reviews and enable price differentiation.

- Hedge supply-chain exposure: Locking favorable sheet-steel terms, qualifying alternate material sources, and localizing critical fabrication can reduce margin volatility tied to raw-material swings.

- Use M&A to build scale where needed: Target acquisitions that fill capability gaps—certification labs, regional service networks, or niche high-efficiency technologies—to improve CR performance and accelerate cross-sell.

Investor & executive outlook

Investors should view the market as a steady-growth industrial segment with idiosyncratic pockets of premium demand tied to regulatory tightening and high-efficiency product adoption. Margin stability will increasingly correlate with aftermarket share and the ability to demonstrate certified performance under evolving standards. Executives should model scenarios that capture the effects of near-term input-cost inflation and staggered regulatory enforcement, and prioritize investments that shorten payback times and deepen service engagement.

Next steps

PW Consulting’s Mechanical Dust Collector Market report provides the executable intelligence required for 2026 planning: the full dataset, granular segmentation tables, competitor profiles, and a downloadable Excel model for custom scenario analysis. For procurement leaders, product strategists, and M&A teams seeking the underlying tables and detailed company benchmarking, our report and data pack are the essential next step.

Contact PW Consulting or visit our report page to access the full study, the interactive model, and a bespoke briefing tailored to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Mechanical Dust Collector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com