Pallet Volume Calculator for Freight & Warehouse Logistics | One Union Solutions

Other |

2026-05-23 18:01:49

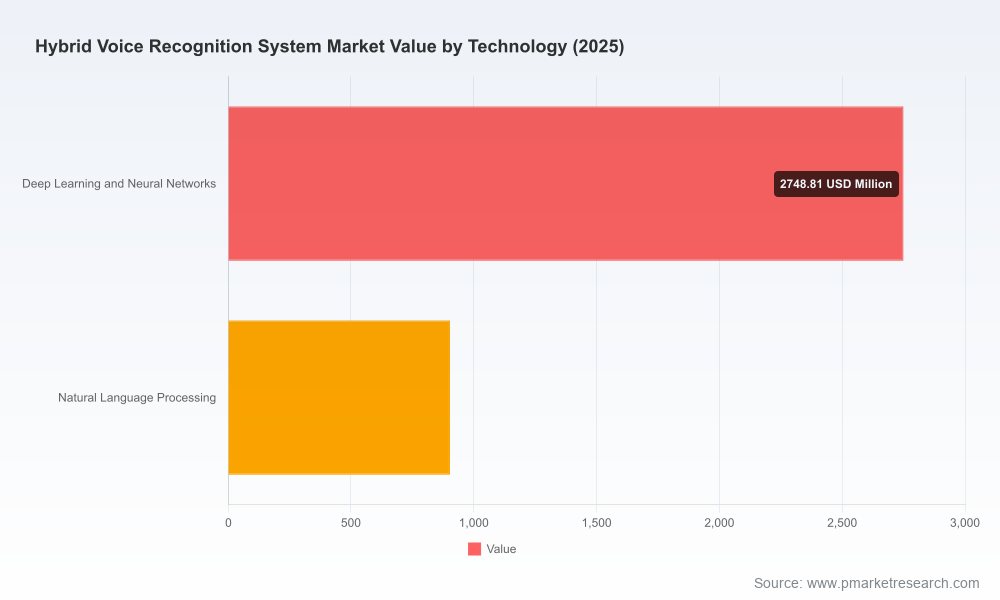

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a concise strategic brief drawn from our full market research report on Hybrid Voice Recognition Systems. The hybrid voice recognition market is entering a phase of rapid scaling and structural consolidation: our analysis shows a compound annual growth rate (CAGR) of 23.95% across the forecast horizon, building from a 2025 base and accelerating toward a materially larger market size by 2032. For executives planning 2026 investments—whether in product architecture, M&A, partnerships, or regulatory compliance—this brief synthesizes the report’s most consequential insights while preserving the granular tables and segmentation that we reserve for the full release.

Hybrid Voice Recognition System Market

Acceleration and optionality: Hybrid architectures—mixing on-device/edge processing with cloud neural models—are becoming the default design pattern for organizations that require low-latency interactions, privacy-preserving data flows, and scalable model training.

Hybrid Voice Recognition System Market

Market scale and runway: With a near-24% CAGR through our forecast period, vendors and adopters should treat 2026 as a pivot year: choices made now about architecture, data governance, and go-to-market will compound rapidly.

Hybrid Voice Recognition System Market

Concentration and competitive dynamics: The market shows moderate concentration (CR3 ~42.15%, CR5 ~58.4%), creating opportunities for focused challengers and strategic niche plays even as large cloud and automotive incumbents extend their reach.

Edge-first meets cloud-scale: The dominant product architectures are hybrid designs that push latency-sensitive inference to the edge while leveraging cloud resources for continual model improvement, personalization, and compliance auditing. Organizations should adopt an “edge-aware cloud” strategy rather than treating edge or cloud as mutually exclusive choices.

Industry-specific vectors: Healthcare, automotive, and enterprise contact centers are driving differentiated requirements—precision on domain lexicons, deterministic latency, and provable data controls. Vendors that offer verticalized datasets and compliance toolkits will capture higher-margin deployments.

Regulatory and trust premiums: GDPR, HIPAA-related expectations, and third-party certifications increasingly shape procurement. Compliance readiness (SOC 2 Type II, ISO 27001, and demonstrable data-minimization practices) has become a procurement filter rather than a checkbox.

Platformization vs. specialization: While hyperscalers provide extensible hybrid stacks, a cluster of specialists continues to win on domain expertise and embedded systems. Your choice of partner should map to whether you require a platform partner (scale, integrations) or a specialist (latency, domain accuracy).

The competitive field combines hyperscalers, automotive specialists, speech-focused AI vendors, and national champions. Key players exhibit distinct strengths and strategic postures:

Nuance Communications — hybrid cloud-edge portfolios and deep automotive and healthcare relationships position Nuance as a go-to for regulated verticals seeking turnkey integrations.

Google (Alphabet) — brings broad cloud-scale speech services and advanced multilingual models, and is accelerating edge partnerships to exploit 5G-enabled low-latency use cases.

Microsoft — Azure Speech Services emphasizes enterprise controls and on-prem/edge deployment options, appealing to customers wanting tight integration with enterprise identity and compliance stacks.

AWS (Amazon Web Services) — combines scalable transcription and a suite of complementary AI services, making it an attractive option for cloud-native enterprises prioritizing operational scale.

Apple — on-device privacy-centric processing is a meaningful differentiator in consumer devices and privacy-sensitive deployments.

IBM — focuses on industry-specific deployments with strong tooling for regulated terminology and enterprise governance.

Automotive specialists (e.g., Cerence) — deliver embedded, vehicle-grade solutions optimized for in-car latency and natural language understanding.

Regional and language specialists (e.g., iFLYTEK, Baidu, Speechmatics) — provide superior language coverage and domain adaptation in specific geographies or sectors.

Focused innovators (e.g., SoundHound, Sensory) — target low-power, embedded inference and sophisticated NLU partnerships for IoT and voice-enabled devices.

Recent industry moves reinforce these trends: a leading automotive-targeted product launch by Nuance (Jan 2025), Speechmatics’ rollout of healthcare-focused multilingual engines (Mar 2025), and strategic telco-edge partnerships announced by Google to exploit 5G edge compute (Feb 2025). These events exemplify the race to marry vertical expertise, regulatory readiness, and edge-cloud orchestration.

Data protection frameworks such as GDPR and HIPAA are active constraints shaping system architectures—explicit consent flows, data minimization, and strong encryption are non-negotiable for enterprise deployments.

NIST’s AI Risk Management Framework and industry-standard certifications are increasingly required to demonstrate governance over lifecycle risks, including bias, drift, and adversarial threats.

Architectural choices should incorporate auditability: immutable logging of model inputs/outputs (where allowed), model versioning, and data lineage are essential to support incident response and regulatory inquiries.

Our full report is built as a toolkit for 2026 decision-makers. Highlights include:

Market sizing and scenario-based forecasts with sensitivity analyses to inform capital allocation and go-to-market timing.

Vendor scorecards and a procurement checklist that evaluates vendors on latency, accuracy in noisy environments, compliance readiness, TCO, and integration effort.

Architecture playbooks comparing edge-first, cloud-first, and hybrid reference designs, complete with cost/latency tradeoffs and an implementation roadmap.

Regulatory compliance templates and data governance checklists mapped to GDPR, HIPAA, SOC 2 Type II, and ISO 27001 requirements.

Decision frameworks for build vs. buy, including a modular vendor compatibility matrix and ROI modeling templates that accommodate recurring model update costs.

Scenario-based M&A and partnership playbooks designed to identify bolt-on acquisition targets or strategic alliance candidates in prioritized verticals.

These deliverables are tailored to C-suite leaders, product and platform VPs, procurement teams, and compliance officers who need operationally useful guidance rather than abstract market commentary.

Adopt a phased hybrid architecture: prioritize edge inference for latency-sensitive paths and reserve cloud cycles for personalization, heavy retraining, and analytics.

Institutionalize compliance-by-design: include privacy impact assessments and certification roadmaps when scoping pilots to avoid costly rework during scale-up.

Partner strategically: hyperscalers offer scale, while specialists offer domain accuracy—combine both through negotiated SLAs that align incentives for data sharing, model updates, and latency guarantees.

Design procurement around TCO and model lifecycle costs, not just per-inference pricing—account for data labeling, continuous evaluation, and edge hardware refresh cycles.

Build multilingual and low-resource strategies early: deploying in linguistically diverse markets will require targeted data collection and domain transfer learning techniques rather than one-size-fits-all models.

Monitor M&A and regional champions: the market concentration metrics suggest room for consolidation—evaluate acquisition targets that bring proprietary domain datasets or embedded systems capabilities.

Use the report to convert strategic intent into tactical programs: run a 90-day pilot using our architecture playbook, align procurement KPIs to the vendor scorecard, and map regulatory milestones against product development sprints. For boards and CxOs, the market-scale projections and concentration analysis provide the context to approve mid-sized investments that can secure first-mover advantages in your vertical.

PW Consulting’s full Hybrid Voice Recognition Systems Market report contains the complete modeling, vendor benchmarks, and downloadable tools referenced above. This brief is designed to orient your 2026 planning with high-confidence insights while preserving the detailed datasets, segmentation, and benchmark tables for subscribers.

For organizations ready to move from strategy to execution, we recommend commissioning a targeted consulting engagement to map these findings directly to your product portfolio, regulatory posture, and partner ecosystem.

For detailed analysis of this topic, please visit the official page:Hybrid Voice Recognition System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com