Hybrid Image Intensifier Market Analysis(2024-2034)

Other |

2026-03-23 06:58:39

PW Consulting’s latest market study on the Angiography Contrast Media market provides an evidence-based roadmap for executive teams preparing strategic decisions in 2026. Our proprietary model shows the market expanded from roughly USD 1.66 billion in 2020 to approximately USD 2.19 billion in 2025, and is forecast to reach about USD 3.25 billion by 2032, reflecting a compounded annual growth rate of 5.82% across the 2026–2032 forecast window. These headline dynamics conceal important inflection points — from regulatory shifts and clinical safety drivers to device–agent integration — that will determine winners and losers in the coming 18–36 months.

Angiography Contrast Media Market

Timing of capital allocation. The market’s steady mid-single-digit growth masks pockets of accelerated adoption tied to imaging platform refresh cycles and procedural migration (e.g., growth of CT angiography versus legacy modalities). Teams deciding on R&D budgets, M&A targets, or manufacturing investments need forward-looking scenario analysis to avoid misallocating capital into low-velocity subsegments.

Angiography Contrast Media Market

Regulatory and reimbursement inflection points. Recent and imminent regulatory guidance — including agency statements on gadolinium safety for renally impaired patients and 2026 updates to CPT coding for diagnostic angiography — materially change clinical choice architecture and reimbursement pathways. These changes affect formulary positioning, clinical trials design, and pricing strategies.

Angiography Contrast Media Market

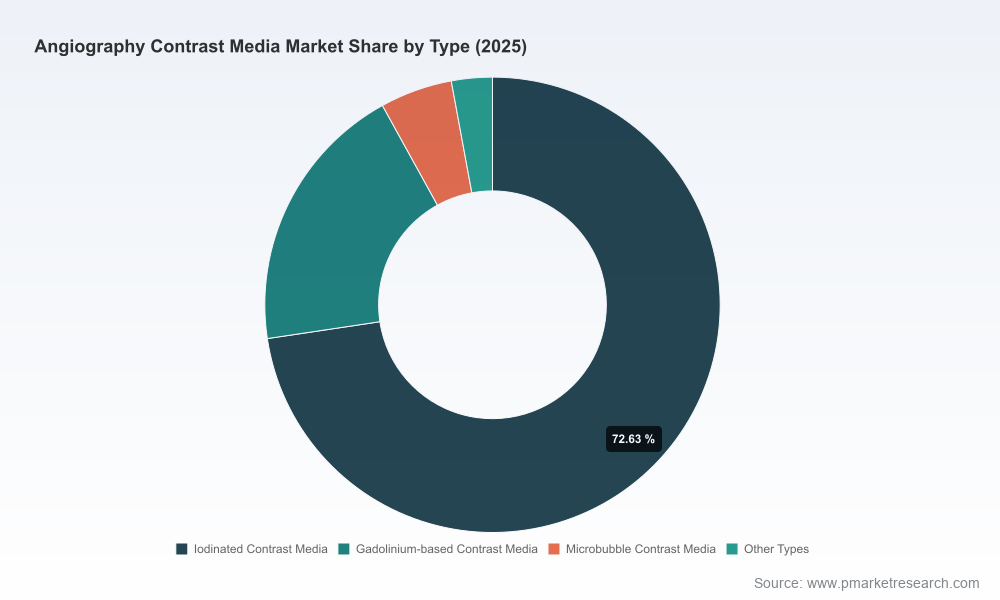

Concentration and competitive posture. The market is materially concentrated: our concentration metrics indicate the top three players control a dominant share, and the top five an even larger proportion. This structure favors incumbents but also creates strategic windows for niche specialists and device-integrated solutions.

Market sizing and growth scenarios. A transparent, audited model that maps historical performance and three forward scenarios (base, upside, downside) to support stress-tested planning and sensitivity analysis for 2026 budgeting cycles.

Commercial playbooks. Go-to-market blueprints for five archetypal companies (incumbent global supplier, regional manufacturer, device partner, specialty biotech, and new entrant), including sales channel optimization, clinical evidence sequencing, and contracting tactics tailored to payer mixes.

Regulatory & reimbursement matrix. A rolling map of regulatory constraints and reimbursement levers — with practical checklists for filing strategies, label extensions, and coding opportunities tied to angiography procedures.

Technology & integration assessment. A vendor-agnostic evaluation of injector compatibility, contrast delivery platforms, and software-enabled dosing protocols to prioritize partnerships that improve clinical throughput and reduce contrast-related adverse events.

Supply chain and manufacturing playbook. Risk heatmaps and mitigation strategies that reconcile raw-material exposure, fill–finish capacity constraints, and price-optimization under rising input costs.

M&A and partnership screening. A data-driven shortlist of strategic targets and deal archetypes, with valuation sensitivities and synergies quantified at the business-case level.

Prioritize compatibility and co-marketing with device OEMs. Recent regulatory clearances that formalize compatibility between contrast agents and injection systems show the commercial upside of device–agent partnerships: tighter clinical workflows, shared procurement conversations, and premium contracting opportunities.

Invest selectively in clinical safety data for renal- and allergy-risk populations. With regulators and specialty societies emphasizing patient safety (notably around gadolinium and iodinated agents in renally impaired patients), differentiated evidence can unlock formulary preferences and justify price premiums.

Deploy granular pricing and contracting playbooks for hospital systems. Given the market’s concentration, leading buyers wield significant negotiating power. Sophisticated rebate and bundling constructs — linked to performance metrics such as reduced contrast volume per procedure or improved throughput — are increasingly decisive.

Strengthen manufacturing resilience through dual-sourcing and capacity hedging. A short interruption at a concentrated supplier can ripple across the market; proactive capacity investments or toll-manufacturing arrangements reduce that risk.

Target bolt-on acquisitions that add device compatibility, regional manufacturing scalability, or niche safety formulations. These deals can accelerate access to clinical customers and create entry barriers for pure-play generics.

Our strategic assessment profiles the primary global players and the structural roles of regional manufacturers and device partners. A few themes stand out:

Incumbent portfolios and brand equity. Established firms with broad portfolios and long-standing agent brands maintain clinical trust and deep distribution relationships. These incumbents can leverage integrated commercial teams to defend share and cross-sell into interventional suites.

Device–agent convergence is accelerating. Recent regulatory events have underscored the commercial and clinical benefits of validated compatibility between contrast agents and injection platforms. Such integrations improve imaging consistency and create joint value propositions for hospitals seeking predictable workflows.

Regional producers remain important price and supply players. Companies manufacturing at regional scale are pivotal in cost-sensitive markets and can be attractive partners (or acquisition targets) for global firms seeking to localize supply chains.

Representative company positions we analyze in the report include:

GE HealthCare — a broad portfolio player with clinically established iodinated agents and deep ties into imaging systems and service networks, enabling cross-sell to radiology and cardiology units.

Bayer AG — active on both the agent and device compatibility fronts; recent regulatory recognition of multi-agent compatibility with advanced injection systems illustrates the company’s strategic focus on systems-level solutions.

Bracco and Guerbet — specialist contrast firms with strengths in agent innovation and clinician familiarity; they compete on formulation performance and clinical evidence.

Device and systems specialists (including ulrich and major imaging OEMs) — increasingly influential in shaping contrast choice through injector capabilities, workflow features, and validated compatibility claims.

Regional manufacturers (e.g., Taejoon, J.B. Chemicals, Sanochemia) — important for capacity, price competition, and localized distribution, particularly where tender-driven procurement dominates.

Safety guidance on contrast agents — especially around gadolinium use in patients with severe renal impairment — will steer clinical protocols and formulary decisions. Preference for lower-risk agents can shift demand patterns even without pricing changes.

Reimbursement coding updates that clarify pathways for CT angiography and diagnostic angiography influence the economics of adopting higher-cost but workflow-enhancing contrast-delivery solutions.

Professional society guidelines continue to emphasize judicious use of iodinated contrast, including premedication regimens for allergy-prone patients; these operational requirements affect per-procedure economics and product selection.

Our findings are built from a triangulation of primary interviews with hospital procurement and clinical leaders, quantitative demand-side modelling, pricing-floor analysis, and a supplier-side assessment of manufacturing capacity and new product pipelines. Every headline forecast is accompanied in the full report by sensitivity bands and a clear statement of assumptions to support board-level scrutiny and investment committee reviews.

For commercial teams: use the playbooks to align product, clinical, and contracting strategies around device compatibility and patient-safety differentiation.

For corporate development: apply the M&A screening and valuation sensitivities to prioritize targets that de-risk supply and accelerate device partnerships.

For operations and supply chain: implement the manufacturing resilience checklist and cost-to-serve analysis to protect margins in 2026 procurement cycles.

PW Consulting’s full Angiography Contrast Media Market report contains the granular segment-level forecasts, company scorecards, and the proprietary dataset behind the scenarios summarized here. The brief above is deliberately a strategic “trailer” — designed to surface the most consequential decision levers while preserving the detailed intelligence that powers executable plans. For access to the complete report, datasets, and an executive briefing tailored to your organization’s stakeholder map, visit our report landing page or contact our advisory team.

For detailed analysis of this topic, please visit the official page:Angiography Contrast Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com