Noninvasive Cardiac Output Monitoring Devices Market Demand, Share, and Forecast 2031

Health |

2026-05-08 11:04:33

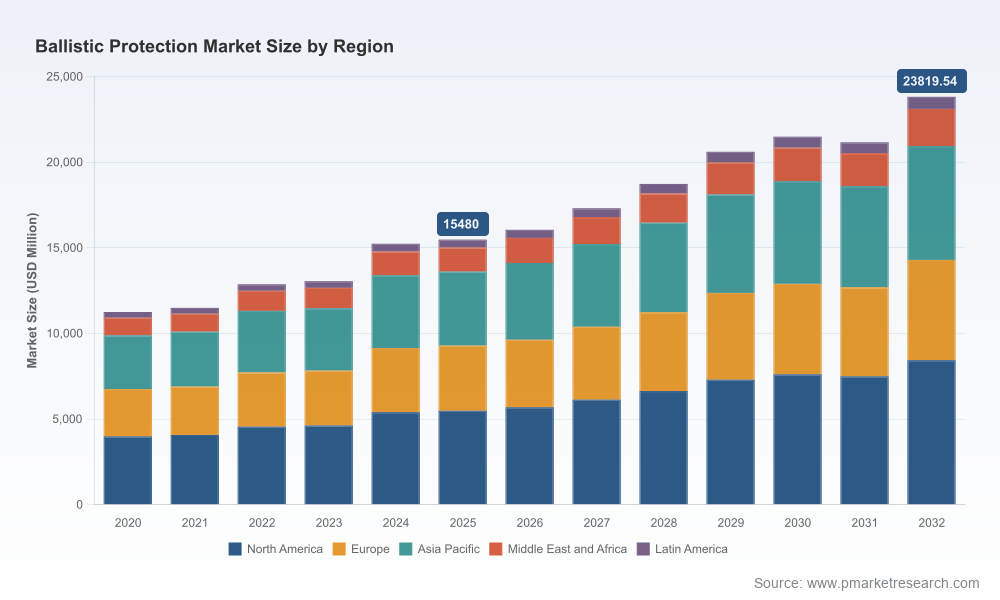

Global demand for ballistic protection is on a sustained growth trajectory. Our new market model shows the industry expanding from a multi-billion dollar base in 2020 to an estimated USD 15.48 billion in 2025, and projecting to approach USD 23.82 billion by 2032 — a compound annual growth rate (CAGR) of 6.35% across the 2026–2032 forecast window. That macro momentum reflects a confluence of operational modernization across defense and law enforcement, materials-driven performance gains, and regulatory refresh cycles that are accelerating replacement and upgrade programs worldwide.

Ballistic Protection Market

Timing and certification are now strategic levers: Updated standards and testing protocols are triggering replacement cycles and creating first-mover advantage for manufacturers who can certify new platforms quickly.

Ballistic Protection Market

Material substitution is reshaping product roadmaps: Lightweight, higher-performance fibers are changing product architectures and procurement requirements — with direct implications for R&D prioritization, supplier selection, and product positioning.

Ballistic Protection Market

Supply-chain risk has real value: Raw-material cost volatility and concentrated upstream production mean sourcing strategies and contractual protections materially affect margins and delivery timelines.

Regulatory inflection points. Transition to updated standards — notably the U.S. NIJ 0101.07 and revisions to NATO STANAGs — has compelled many procurement authorities to accelerate upgrade programs and to require new certification pathways (including sizing and ergonomics for women). For manufacturers, the cost of certification and the timeline to market are now central components of go-to-market calculus.

Materials transition and R&D pressure. Advances in ultra-high-molecular-weight polyethylene (UHMWPE) and new unidirectional hard materials are enabling meaningful weight reductions in plates and laminates; other fiber technologies and ceramics continue to improve multi-threat performance. These technology shifts are not only product differentiators but also create opportunities for incumbents and new entrants to reposition value propositions around weight, protection level, and cost per use.

Upstream cost and capacity dynamics. Para-aramid feedstock and other polymer inputs experienced price pressure in recent cycles, elevating the importance of raw-material hedging, supplier diversification and long-term off-take agreements. Concurrently, strategic capacity investments — shown by recent manufacturer expansions — underline rising emphasis on localized manufacturing to de-risk logistics and meet sovereign procurement preferences.

Commercialization and modularity trends. Customers increasingly demand modular, multi-threat, and ergonomic systems — from personal protective equipment to vehicle and platform armor — driving suppliers to integrate materials science, systems engineering and accessory ecosystems (communications, mounting, and modular add-ons) into single offerings.

This report is designed as an operational toolkit for 2026 planning. It blends rigorous market modelling with practical, executable assets that senior leaders can apply immediately:

Validated market-sizing and topline forecasts (2020–2032) with scenario branches for high- and low-demand paths, enabling stress-testing of capital plans and product launches.

Competitive scorecards and capability maps that differentiate material suppliers, platform integrators and niche specialists — covering technology readiness, certification footprint, manufacturing scale, and margin dynamics.

Procurement playbook templates: contract clauses, supplier risk-rating frameworks, and negotiation levers tailored to ballistic materials and finished systems.

Supply-chain risk matrix and mitigation blueprints: raw-material shock scenarios, onshoring/nearshoring decision frameworks, and inventory/lead-time optimization tools.

Regulatory and certification roadmap: step-by-step planning for NIJ and NATO-aligned approvals, including timelines, testing requirements and cost-to-certify models.

M&A and partnership heatmaps: targets and strategic fit analyses for scale vs. capability plays, along with integration risk checklists.

CapEx and manufacturing expansion models: ROI calculators for facility investments, tooling, and automation tailored to armor production economics.

Commercial GTM playbooks: tender response templates, pricing strategies by channel, and segmentation-based go-to-market priorities (kept high-level to preserve commercial leverage).

The market structure blends large systems integrators, specialized body-armor manufacturers, and material science leaders. Our concentration analysis shows a market that is consolidated enough for scale to matter, but with significant room for differentiated technology plays: the three-largest firms account for a meaningful but far-from-dominant share, while the top five collectively represent a clear majority of market influence. This posture enables both consolidation plays and focused niche strategies.

Across the ecosystem, players fall into three strategic archetypes:

Integrated defense system suppliers (e.g., leading multi-domain platforms) that bundle armor as part of broader survivability suites and whose advantage lies in platform-level integration, defense contracting relationships, and aftermarket services.

Specialist body-armor and helmet manufacturers that compete on product performance, certifications, and procurement agility for law enforcement and soldier systems.

Advanced materials manufacturers that supply fibers, laminates and ceramics — the source of fundamental performance gains — and that increasingly compete upstream through licensing and co-development with OEMs.

Recent industry moves illustrate these dynamics: product launches touting ultra-lightweight helmet and plate systems, hard-material innovations that claim substantial weight reductions, and investment rounds expanding manufacturing capacity in key markets. For executives, the takeaway is clear — materials innovation and certification velocity materially influence competitive advantage.

Prioritize certification velocity. Build dedicated pathways and cross-functional teams to accelerate approvals under new standards; early certification can win procurement waves tied to regulatory refresh cycles.

Revisit materials strategy. Combine performance testing with total-cost-of-ownership models to evaluate UHMWPE, aramid blends, ceramics and hybrids across threat scenarios and lifecycle costs.

Hedge raw-material exposure. Structure multi-year off-take agreements, dual-sourcing strategies, and, where feasible, upstream equity or strategic partnerships to secure feedstock and protect margin.

Pursue selective nearshoring. For suppliers serving sovereign buyers, local manufacturing capacity is increasingly a procurement prerequisite; evaluate brownfield expansions versus greenfield investments using our CapEx ROI toolkit.

Design modular product portfolios. Invest in modularity that enables platform commonality and reduces certification burden across different system configurations.

Scan for acquisition targets that add certified technologies, proprietary materials, or manufacturing footprint — not just revenue scale.

Embed ergonomics and inclusivity in R&D. Updated testing standards emphasize fit and female-specific considerations; early compliance can be a competitive differentiator in law-enforcement and civil markets.

For boards, corporate strategy teams and procurement leaders, the report functions as both a forecast and an execution manual. Use it to stress-test budgets, set R&D velocity targets, structure supplier partnerships and build the operational capabilities required to compete in an era of material innovation and tighter regulatory scrutiny.

PW Consulting’s full Ballistic Protection Market report contains the underlying model, granular scenario outputs, and downloadable playbooks referenced here. The public preview you are reading intentionally showcases the framework and strategic line-of-sight that will inform 2026 planning while reserving the full subsegment tables, regional and application breakdowns, and proprietary supplier scoring matrices for our subscribers and report purchasers. For complete data, step-by-step templates, and access to our interactive dashboard, please visit the report page.

2026 will be a year of choices that lock in competitiveness for the next business cycle: choices about materials, certification timelines, supplier structures and manufacturing footprint. Organizations that convert the macro trends outlined here into concrete operational plans — supported by hedging, certification, and product modularity — will convert market growth into sustainable advantage.

For detailed analysis of this topic, please visit the official page:Ballistic Protection Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com