Future of Turkey Meat Products Market: Global Trends and Consumption Patterns

Food |

2026-05-18 17:09:26

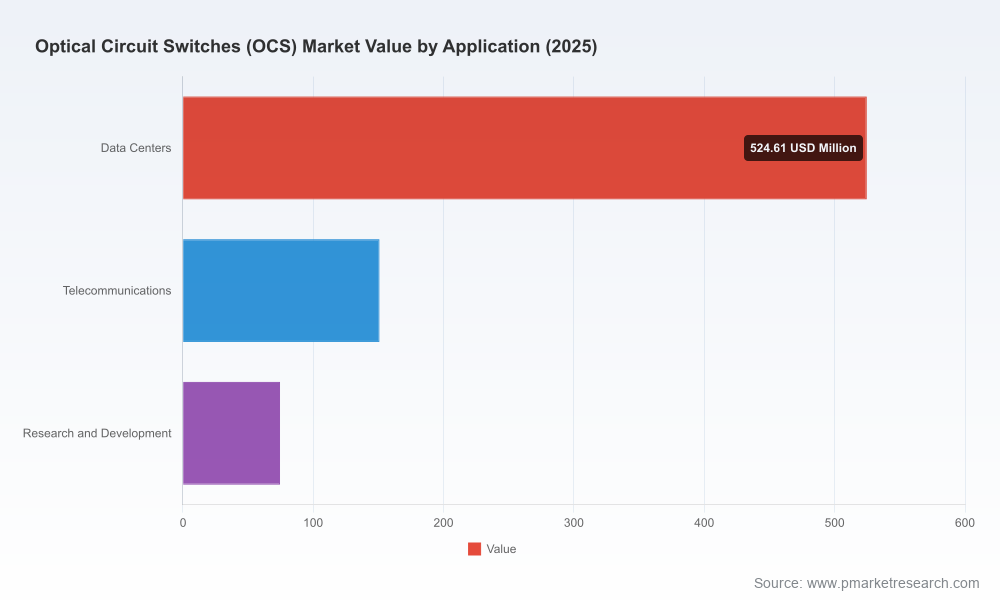

PW Consulting’s latest market study, with a 2025 base year and a historical window covering 2020–2025, delivers a pragmatic, market-tested view of Optical Circuit Switches (OCS) as they move from laboratory curiosity to operational fabric technology for AI-scale data centers. Our bottom-up sizing and scenario-driven forecasts show the OCS market expanding at a compound annual growth rate (CAGR) of 20.5% through the 2026–2032 forecast horizon, rising from a 2025 baseline of USD 750.0 Million (revenue unit: Million USD) to a multibillion-dollar opportunity by 2032. This brief summarizes the tactical insights in the report that matter to CIOs, data center architects, infrastructure investors and procurement teams preparing strategic decisions in 2026 — while reserving detailed segment-level figures and vendor share tables for the full report.

Optical Circuit Switches Ocs Market

AI-driven traffic patterns and larger GPU clusters are stressing electrical switching fabrics. OCS offers a pathway to lower-latency, lower-power, protocol-agnostic interconnects that can materially alter rack- and pod-level network economics.

Optical Circuit Switches Ocs Market

Energy and infrastructure pressures are acute. Electricity can represent a very large portion of a hyperscale site’s operating budget; U.S. data centers consumed ~176 TWh in 2023 and continued electricity demand growth driven by AI is reshaping TCO calculations. OCS adoption is increasingly treated as an energy-arbitrage decision as much as a networking one.

Optical Circuit Switches Ocs Market

Standards and interoperability are moving fast. The Open Compute Project’s OCS sub-project and vendor demonstrations at industry forums have accelerated the practical path to multi-vendor integration — altering vendor selection risk for early adopters.

Market momentum is clear: historical growth from 2020 through 2025 accelerated markedly, and projected growth through 2032 underscores that piloting or planned adoption in 2026 is a time-sensitive decision for organizations planning AI infrastructure refreshes.

Robust sizing and forecasting methodology that ties demand to AI workload trajectories, rack-level topology choices and regional infrastructure constraints. The model is scenario-ready and includes sensitivity to energy prices and utilization assumptions.

Decision frameworks and TCO templates: vendor-neutral calculators that compare electrical switching fabrics vs. OCS across CapEx and OpEx dimensions, factoring in realistic insertion loss, reliability, and maintenance windows.

Deployment playbooks: step-by-step guides for pilot scoping, integration testing, orchestration and incremental scaling from pod-level pilots to rack-aggregate fabrics.

Vendor assessment matrices and procurement templates: technical checklists, integration test scripts and contract clauses to mitigate delivery, IP and lifecycle risks.

Technology deep dives: comparative analysis of MEMS, liquid-crystal-on-silicon (LCoS), silicon photonics PICs and robotic all-fiber patch panels — including operational trade-offs (latency, power, scalability, serviceability).

Standards and regulation tracker: a curated map of OCP activity, national renewable-energy procurement rules affecting data center siting, and power-availability constraints with direct line items that matter to site selection and project finance.

Plan pilot programs now. Given the market’s rapid expansion (20.5% CAGR) and accelerating vendor product roadmaps, organizations that begin controlled pilots in 2026 will be better positioned to avoid disruptive forklift upgrades in the 2027–2029 window.

TCO inflection exists at scale. Energy cost assumptions and GPU-cluster utilization drive the inflection point where OCS becomes the lower-cost option; our report supplies the templated models to run that analysis against your operational data.

Vendor risk is shifting from single-product performance to ecosystem interoperability and manufacturing scale. Silicon photonics and foundry partnerships are moving toward pre-production — a structural change that affects lead times and supply risk.

Standards participation reduces lock-in. Active engagement with OCP and interoperability testbeds materially lowers migration risk and should be a procurement prerequisite where multivendor fabrics are expected.

Regulatory and regional power policies will alter siting calculus. Renewable procurement requirements and grid-connection rules are increasingly binding constraints on new builds and expansions — make them part of network architecture decisions.

Adopt a staged architecture strategy. Incremental deployment — starting with AI scale-up fabrics and highly utilized east-west traffic domains — preserves optionality while capturing early energy savings.

The OCS vendor field is diverse, with distinct platform archetypes emerging. Our research profiles leading suppliers, maps their technology differentiators, and assesses which buyer needs each archetype best addresses. High-level notes on core vendors covered in the report:

Lumentum Holdings Inc. — MEMS-based platforms focused on high-port devices (examples include high-radix R-series models). Lumentum’s collaborations with optics and switch-system partners have created practical rack-level integrations demonstrated at industry events.

Coherent Corp. — LCoS-based optical circuit switches emphasizing low latency and reliability for AI fabrics where deterministic performance matters.

Molex — Recent launches of high-radix OCS platforms indicate a roadmap prioritizing scale and dynamic reconfiguration for hyperscale GPU clusters.

DiCon Fiberoptics — Value-focused MEMS offerings that balance proven reliability with cost-conscious deployment economics, targeting data-center operators seeking lower-cost entry points.

HUBER+SUHNER Polatis — Beam-steering and DirectLight approaches offering low-loss matrices and a history of systems-level deployments in automated data center environments.

Telescent Inc. — Robotic, all-fiber patching and automation tailored to ultra-high port counts and very low-loss reconfiguration requirements.

Calient.AI (Calient Technologies) — MEMS-based all-optical OCS aimed at dynamic interconnection and test automation, with a protocol-agnostic posture.

iPronics — Silicon photonics OCS entries focused on low-power, low-latency programmable fabrics; their approach signals the longer-term cost trajectory for integrated PIC-based switching.

Omnitron Sensors — Component-level MEMS mirror technology that enables very-high-channel-count switches; often a strategic supplier to systems integrators.

Recent vendor developments — product launches, demonstrations and foundry partnerships — signal a maturation of both capability and supply chains. Notable movements in early 2026 include high-radix platform introductions, value-focused MEMS models, integrated rack demonstrations with silicon optics, and manufacturing partnerships advancing PIC production toward pre-production readiness. These signals compress the window for early adopters to secure favorable commercial terms.

Integrate orchestration planning early. OCS requires software-layer integration to realize fabric agility; orchestration needs should be part of procurement RFPs and acceptance testing.

Design for cabling and optics lifecycle. Physical re-cabling, patching regimes and repair workflows change under OCS; operations teams must re-skill and re-tool maintenance playbooks.

Mitigate manufacturing and supply risk. Foundry partnerships and component shortages can affect lead times; include supply-contingent clauses and multi-sourcing options in vendor contracts.

Quantify energy sensitivity. Use the report’s TCO templates to stress-test projects against utility price trajectories and site-specific renewable procurement rules.

Authorize a focused pilot for 1–2 pod-level AI clusters and scope it with explicit TCO and performance acceptance gates.

Run the report’s TCO templates against your operating data to identify the scale at which OCS becomes accretive.

Update RFPs to require OCP interoperability test participation and to capture lifecycle service and spares strategies.

Engage with foundry and silicon-photonics roadmaps if long-term volume and cost targets are material to your capital-planning model.

PW Consulting’s Optical Circuit Switches OCS Market report provides the analytical foundation, practical templates and supplier intelligence to convert interest into deployment plans. We have intentionally withheld detailed segment share tables and line‑item splits from this brief to ensure that qualified buyers receive the full dataset, scenario files and vendor scorecards available in the complete report package.

To access the full report, supporting models and our executive briefing slots for 2026 implementation planning, visit the PW Consulting research portal. Our analysts are scheduling confidential briefings to walk procurement and architecture teams through the forecast scenarios and hands-on TCO tools — essential inputs for decisions that will determine deployment timing and procurement strategy in the AI era.

For detailed analysis of this topic, please visit the official page:Optical Circuit Switches Ocs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com