Budesonide Inhaler Market: Insights and Competitive Analysis

Other |

2026-05-04 08:45:39

PW Consulting’s latest market study, One Stop Collaboration Platform For Enterprise Market (base year 2025), delivers a forward-looking, practitioner-focused roadmap for enterprise leaders making platform, vendor and architecture decisions in 2026. Our analysis shows the market roughly doubling in size over the 2020–2025 period and, with a compound annual growth rate (CAGR) of 12.48% across the 2026–2032 forecast window, continuing to expand materially through the end of the decade. By 2025 the global market reached an institutional scale measured in tens of billions of USD, and our models project it will more than double again by 2032 as cloud-native, AI-enabled and hybrid collaboration workflows become embedded across enterprise operations.

One Stop Collaboration Platform For Enterprise Market

Procurement clarity under tightening compliance: New privacy and data-protection mandates (including the expanded California privacy regime effective January 1, 2026, and ongoing U.S. state-level initiatives) mean sourcing, contract language and data flow architectures must be revisited before any large-scale consolidation or migration.

One Stop Collaboration Platform For Enterprise Market

AI is now a platform decision: Leading vendors are embedding AI across meetings, documentation, task automation and search. Understanding vendor roadmaps and the practical implications for governance, MLOps and data residency is mission-critical for 2026 rollouts.

One Stop Collaboration Platform For Enterprise Market

Cost modeling in an era of variable cloud pricing: Rising public cloud consumption and evolving IaaS/PaaS economics require tighter TCO/variable-cost modeling when comparing cloud-native vs hybrid/on-premise deployment scenarios.

Vendor consolidation vs best-of-breed trade-offs: With concentration metrics showing a clear top-tier influence, organisations must weigh the operational simplicity of consolidation against the innovation advantages of specialised point solutions.

Hybrid and distributed work design: Meeting room hardware, room orchestration, and integration with collaboration stacks must be treated as an enterprise architecture decision rather than a facilities or AV issue alone.

This study is built for executives, IT architects, procurement teams and product leaders who need not only to understand market direction, but to act. The report combines quantitative modeling with playbooks and artifacts you can use immediately:

Market sizing and forecast: rigorous top-down and bottoms-up models, transparent assumptions, sensitivity analyses and scenario projections calibrated to macro cloud-spend trends and enterprise adoption curves.

Buyer personas and journey maps: procurement, IT, security, HR and business-unit personas with decision criteria, typical procurement timelines, and stakeholder matrices to accelerate internal alignment.

Vendor profiles and strategic positioning: independent assessments of product capabilities, roadmap direction, integration openness, pricing models and enterprise support. Profiles cover the largest global suppliers and rising challengers.

Go-to-market and partnership frameworks: how platform vendors, system integrators and hardware partners can create mutually reinforcing offers; partner incentive structures that reliably increase win rates; and channel playbooks for enterprise penetration.

Implementation playbooks and RFP artifacts: templated RFP language, checklist-driven evaluation scorecards, phased migration plans, and governance templates tailored to cloud, hybrid and on-premise rollouts.

Security, privacy and compliance toolkits: detailed checklists to comply with emerging state- and country-level privacy laws, contractual clauses for data processing and cross-border transfers, and a pragmatic approach to ADMT (automated decision-making technology) auditability.

TCO and ROI models: configurable calculators that reflect license fee structures, cloud hosting costs, integration and change management costs, and productivity uplift scenarios.

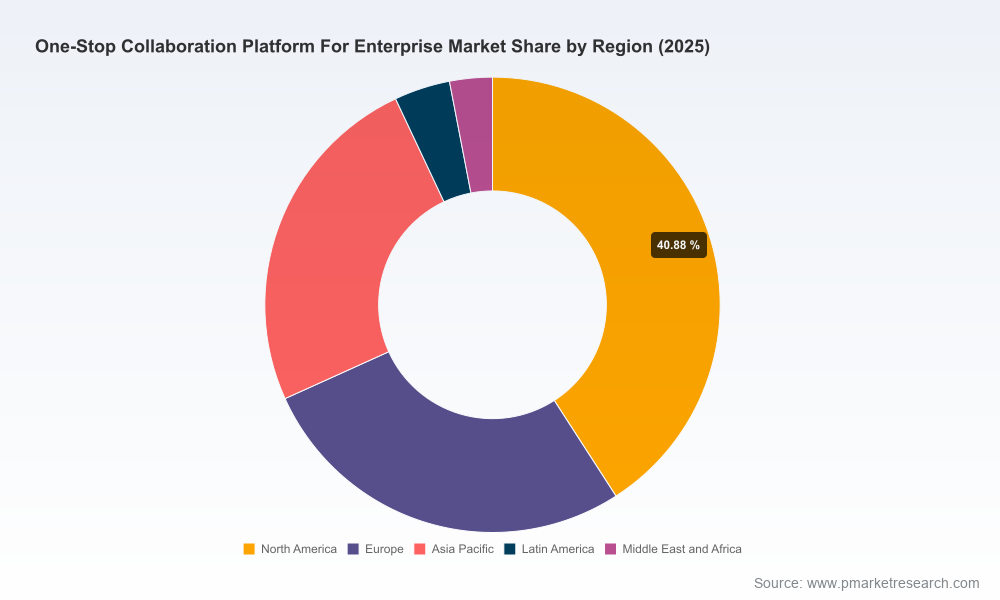

The market exhibits a clear tiering: a dominant group of vendors drives platform consolidation while a competitive cohort of specialist and integrated-suite providers pushes rapid feature innovation. Concentration is meaningful — our market concentration metrics indicate that the top three players capture a majority share, and the top five are substantially more dominant — a dynamic that shapes pricing power, partner ecosystems and innovation trajectories.

Microsoft continues to position Teams as the enterprise collaboration hub, deepening Copilot and cross-application AI to automate meeting workflows and knowledge capture. Enterprises evaluating long-term consolidation must assess Microsoft’s roadmap for both governance and extensibility.

Slack (Salesforce) is being integrated more tightly into CRM-oriented workflows. For sales- and service-led organisations, the Slack + Salesforce construct offers a compelling case for customer-facing collaboration use cases.

Zoom has remained focused on communication breadth — meetings, webinars, phone and contact-center integrations. Its differentiation rests on reliability at scale and ease of use for distributive communication patterns.

Google Workspace continues to push a cloud-native document-first collaboration experience; strength lies in low-friction co-editing and search, with AI-enhancements solidifying its productivity value.

Cisco Webex competes on security and hybrid meeting experiences, increasingly marrying AI features with an audiovisual-first approach suitable for regulated and large-scale enterprises.

Atlassian, Wrike, Asana, ClickUp, Bitrix24 and other work-management providers are aggressively expanding platform capabilities to capture project and knowledge workflows that historically lived outside unified collaboration suites.

Salesforce, Zoho, RingCentral and others differentiate through vertical integrations — tying collaboration into CRM, contact center, and business applications to improve frontline productivity.

Recent vendor moves in late 2025 and early 2026 underscore these trends: major AI feature rollouts, productization of AI agents, modular room systems that integrate with collaboration suites, and increased hybrid-work tooling. These tactical advances are material to procurement timelines in 2026: they alter the feature baseline and the negotiation reference points for licensing and managed services contracts.

Privacy and compliance: Expanded privacy regimes — including the California changes effective January 1, 2026 — heighten requirements for risk assessments, consent management and opt-outs for automated decision-making. Buyers must bake compliance checks into supplier scorecards and data flow diagrams early in procurement.

Cloud economics: Global public cloud spending remains a primary driver of hosting and platform economics. Rising IaaS/PaaS consumption affects run-rate costs and the variable portion of TCO; our models show cloud cost variability materially influences lifecycle cost estimates for multi-year deployments.

Data protection enforcement: Ongoing GDPR and equivalent enforcement in multiple jurisdictions is increasing the operational burden on vendors and buyers alike. Contractual safeguards, vendor lock-in risks and cross-border transfer architectures must be part of the negotiation playbook.

Use the RFP templates and vendor scorecards to reduce evaluation time by up to 40% versus ad-hoc procurement approaches.

Run the TCO/ROI scenarios with your finance and cloud teams to test near-term migration vs extend-and-integrate decisions under three cloud-cost scenarios.

Deploy the security and privacy checklists as a gating mechanism before any proof-of-concept to prevent post-deployment rework tied to compliance gaps.

Leverage the vendor roadmap review module to align your 24–36 month automation and AI adoption timelines with supplier capabilities and release cadences.

In this preview we surface the strategic implications and the operational artifacts that matter for 2026. To preserve the report’s utility as a decision-enabling asset, detailed subsegment tables, granular regional and vertical splits, and full vendor scorecard data are available exclusively in the complete report. These proprietary data and model files contain the precise inputs you will want when building procurement cases, budgeting multi-year migrations, or evaluating vendor negotiations.

Executives moving from exploratory pilots to enterprise-scale rollouts in 2026 must balance three imperatives: secure and privacy-preserving data architectures, AI readiness across collaboration workflows, and pragmatic cost discipline that acknowledges variable cloud economics. Our findings show the market’s scale and trajectory create significant opportunity for outcome-driven consolidation and platform-led productivity gains — but only when procurement, security and architecture are tightly coordinated. PW Consulting’s One Stop Collaboration Platform For Enterprise Market report equips leaders with the narratives, the numbers and the playbooks to make those decisions with confidence.

To access the full market models, vendor scorecards, implementation templates and our proprietary TCO calculators, visit PW Consulting’s report landing page and download the complete study.

For detailed analysis of this topic, please visit the official page:One Stop Collaboration Platform For Enterprise Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com