Decorative Stained Glass Panels Dubai: Elegant Custom Designs for Modern Interiors

Other |

2026-06-22 20:50:35

PW Consulting today releases an executive preview of our new market research report covering the global K‑12 education furniture market through 2032. This briefing distills the report’s strategic value for executive teams planning resource allocation, product strategy, and M&A activity in 2026. It highlights the macro trajectory — and the operational levers that will determine winners — while reserving the granular regional and segment splits for the full report.

K 12 Education Furniture Market

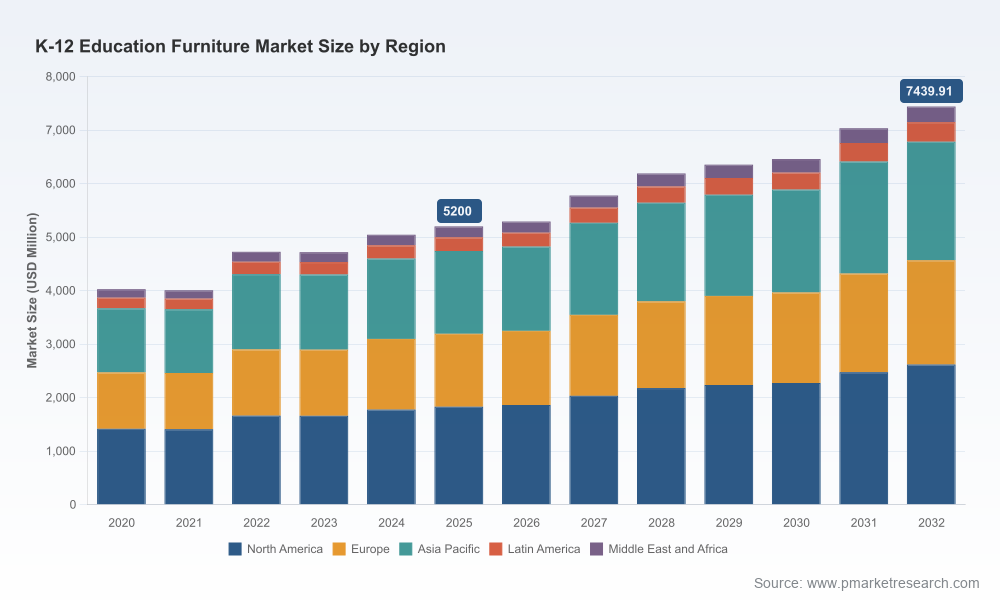

The K‑12 education furniture market has shown resilient expansion since 2020, moving from roughly USD 4.0 billion at the start of the decade to approximately USD 5.2 billion in 2025. Our forecast model, built on multi‑scenario demand drivers and cost inputs, projects a compound annual growth rate (CAGR) of 5.25% across the 2026–2032 forecast period. Under the base scenario, the market is expected to approach approximately USD 7.4 billion by 2032.

K 12 Education Furniture Market

That headline growth masks important structural shifts: procurement cycles are lengthening for large public projects, private‑sector buyers are demanding modularity and sustainability, and school districts are investing in furniture as a component of broader learning‑space transformation rather than as commoditized capital goods. These shifts change how revenue is won, how margins are preserved, and how capacity should be allocated in 2026 and beyond.

K 12 Education Furniture Market

Investment prioritization: The report translates the macro growth path into practical mid‑term scenarios so executives can prioritize capex, facility expansions, or factory rationalizations under differing demand, tariff, and material‑cost conditions.

Procurement playbooks: We provide procurement and bid‑response frameworks tailored to school district buying behaviours and the procurement timelines that dominate 2026 public tenders.

Product and service roadmaps: The analysis links demand drivers (flexible learning, inclusivity, whole‑child support) to portfolio choices – which product attributes to scale, which to phase out, and which service add‑ons (installation, refurbishment, financing) meaningfully improve lifetime value.

Risk and resilience: A calibrated supply‑chain stress test quantifies the downstream impact of tariff shocks and raw‑material price volatility — essential for contract renegotiation and hedging strategies.

Executive summary and three investment scenarios (base, upside, downside) with trigger conditions and decision points for 2026.

Top‑line market sizing and a seven‑year forecast model (2026–2032) with downloadable inputs for client stress testing.

Demand‑driver mapping that connects pedagogical trends (active learning, inclusive design) to product specifications and procurement language.

Supply‑chain heatmaps highlighting critical nodes, key supplier categories, and supplier concentration risks.

Pricing and margin playbooks with scenario pricing for raw‑material shocks and logistics cost impositions.

Commercial go‑to‑market templates for public‑sector bids, private school channels, and institutional partnerships.

M&A and partnership screening criteria with target archetypes and synergy valuation heuristics.

Implementation checklists and KPIs for a 12‑month strategic program (product, operations, commercial).

The market remains moderately consolidated: the top three firms account for under 30% of market revenue, and the top five capture roughly 39% — a structure that supports both scale advantages and opportunities for nimble challengers. Our competitive assessment synthesizes public filings, recent corporate announcements, and primary interviews to build a decision‑useful view of who can scale and why.

Virco Manufacturing Corporation (Torrance, CA): A long‑standing US manufacturer with deep K‑12 distribution channels and trade‑show visibility. Expect Virco to double down on relationships with large districts and emphasize durability and lifecycle cost in bid responses.

KI Furniture (Krueger International, Green Bay, WI): Known for adaptable seating and table systems, KI’s recent facility expansion and new Cognetic Technology seating demonstrate a product‑innovation playbook and capacity investment consistent with taking share in flexible learning environments.

Artcobell (Temple, TX): A legacy domestic manufacturer focusing on durable, made‑in‑USA appeal — positioned to capture tenders valuing domestic production and short lead times.

Paragon Furniture (Arlington, TX), Allied School Furniture (Jacksonville, FL), Smith System (Plano, TX), and HON: These firms compete on design, breadth, and total cost of ownership, often pairing product lines with installation and services to increase stickiness.

Herman Miller and VS America: Bring design and research heft; their strength lies in premium solutions where ergonomics, evidence‑based design, and campus planning packages justify price premiums.

School Specialty and other national distributors: Serve as critical channel partners, particularly for mid‑market buyers and small district consolidation plays.

Recent industry activity reinforces these strategic axes: KI’s manufacturing expansion (announced September 2025) and product launches in early 2026 signal supplier confidence in the flexible‑learning segment. Visibility at trade events (e.g., Virco at FETC 2026) shows suppliers investing in direct engagement with procurement authorities and end‑users. Meanwhile, trend research emphasizing inclusivity, flexibility, and whole‑child design is shifting RFP language and bid evaluation criteria.

Raw‑material and tariff pressures: Elevated Section 232 tariffs on steel and aluminum and increased duties on softwood lumber have already pushed input costs higher. Our scenario models quantify margin erosion and suggest practical countermeasures such as strategic hedging, supplier diversification, and product re‑engineering to reduce metal and wood dependency.

Regulatory compliance: Expect procurement teams to require documented compliance with fire safety, low‑VOC materials, and ergonomic standards — a compliance burden that benefits manufacturers with tested, certified portfolios.

Pedagogical alignment: Districts are specifying furniture attributes that support active, collaborative, and inclusive learning; suppliers that can rapidly demonstrate evidence‑based benefits will win procurement points beyond price.

Perform a 90‑day supply‑chain stress test focused on steel, aluminum, and softwood lumber exposure; secure alternative suppliers and partial forward contracts where appropriate.

Reprice contracts with margin‑protection clauses tied to commodity indices; incorporate phased price‑adjustment mechanisms into multi‑year public bids.

Prioritize modular, serviceable product lines that reduce total cost of ownership and support refurbishment services — an opportunity to expand aftermarket revenue.

Accelerate product certification (low VOC, flammability, ergonomics) to convert compliance into commercial advantage in public tenders.

Evaluate strategic factory investments only under clear demand triggers; consider contract manufacturing partnerships or regional capacity leases to retain flexibility.

Pursue tuck‑in acquisitions to fill capability gaps (e.g., finishes, IoT sensors, refurbishment capability) and to shore up regional distribution networks.

Develop pilot programs with school districts to capture outcome data (student engagement, space utilization) and use that evidence to change bid evaluation criteria.

Our report blends primary market research, supplier diligence, and a closed‑form scenario model that converts macro assumptions into operational decision points. For leadership teams, it functions as both a strategy brief and an implementation kit: not only explaining where the market is headed, but laying out how to act in order to preserve margin, accelerate growth, and mitigate supply‑chain shocks.

We present the analytical architecture — forecasting models, procurement playbooks, unit‑economics templates, and an M&A screening matrix — while intentionally withholding the full set of granular regional and application splits in this preview. That level of segmentation is available in the full report and through our client advisory engagements, where we customize forecasts and recommendations to your product mix, manufacturing footprint, and go‑to‑market capabilities.

For decision teams preparing budgets, board materials, or M&A pipelines in 2026, our K‑12 Education Furniture report converts market outlooks into board‑level actions. PW Consulting offers tailored briefings and model‑customization workshops to align forecasts with your enterprise plans. Contact PW Consulting to schedule a briefing or to access the full report and the downloadable forecast model.

For detailed analysis of this topic, please visit the official page:K 12 Education Furniture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com