Web Hosting Services Market Key Trends and Innovations

Networking |

2026-03-24 08:00:32

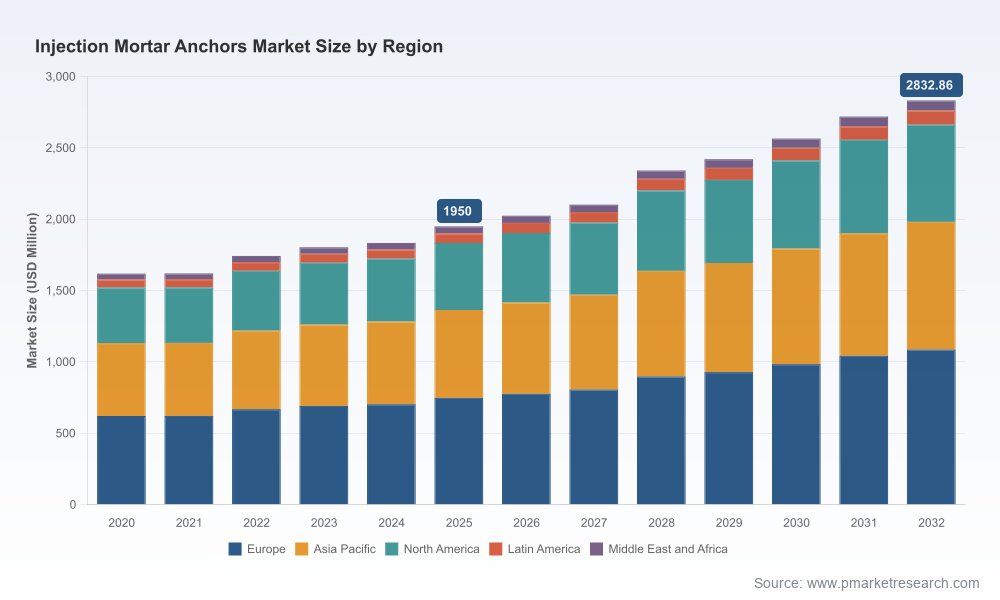

PW Consulting today releases a forward-looking industry brief that frames the strategic choices facing suppliers, distributors and infrastructure owners as the Injection Mortar Anchors market transitions from recovery into a period of steady expansion. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, our analysis quantifies a market that expanded from roughly USD 1.62 billion in 2020 to USD 1.95 billion in 2025 and is forecast to enter 2026 at about USD 2.02 billion. With a compound annual growth rate (CAGR) of 5.48% across the forecast window, PW Consulting projects the market to approach approximately USD 2.83 billion by 2032. This press release highlights the report’s strategic value for decisions to be taken in 2026 while preserving the granular segmentation and proprietary models that are reserved for report subscribers.

Injection Mortar Anchors Market

Actionable market sizing and tempo: Our models reconcile macro demand drivers — infrastructure renewal, retrofitting of aging stock, seismic and fire-resistant design requirements — with supplier-side capacity to produce and certify high-performance injectable mortars. The result is a practical sizing framework that informs near-term investment sizing and capacity planning.

Injection Mortar Anchors Market

Competitive positioning under consolidation: The market exhibits moderate concentration at the top. The three largest players control a notable share, and the top five firms account for just over half of the market — important context when evaluating scale-driven R&D, distribution reach and go-to-market leverage.

Injection Mortar Anchors Market

Cost and margin sensitivity: We pair volume forecasts with a raw-material scenario suite that shows how regional epoxy price dispersion and supply chain shocks can compress margins or create arbitrage opportunities for vertically integrated or geographically diversified players.

Regulatory and approval risk/reward: Detailed mapping of EAD/ETA pathways and low-emission certifications clarifies the time and capital required to win seismic and drinking-water approvals — a key differentiation in public infrastructure procurement.

Demand continues to be driven by two interlocking trends: large-scale infrastructure renewal and a wave of targeted retrofits and strengthening projects in seismic regions. These drivers favor higher-specification products (epoxy and vinyl ester systems with Option‑1 style approvals for cracked concrete, seismic performance and post-installed rebar), while also expanding the addressable market for fast-curing hybrids and stainless-steel-compatible chemistries used in aggressive environments.

On the supply side, raw-material volatility matters. Early-2026 observations indicate regional epoxy resin cost differentials in the order of a few hundred dollars per metric ton across major sourcing hubs — a spread large enough to influence landed cost decisions for cartridge-fillers and private-label manufacturers. For procurement teams, the implication is clear: lockable forward contracts, multi-sourcing and strategic hedging are now core procurement playbooks, not optional optimizations.

Regulatory dynamics are a gating factor. European Technical Assessment (EAD 330499 / ETAG-based pathways) and analogous approvals elsewhere remain prerequisite for structural anchoring use cases. Products that secure the widest option approvals (including seismic classifications) command preferential specification in public projects. Parallel to approvals, low-emission formulations (styrene-free, NSF/ANSI certifications for potable water contact where required) are raising the bar for indoor and sensitive-environment applications.

Our competitive framework groups the market into multinational branded innovators, private-label specialists and regional technical players. Below are strategic characterizations of the leading names analyzed in the report and what their moves signal for 2026 strategies.

Hilti Corporation — A technology-forward integrator known for end-to-end system thinking (anchoring cartridges, tools and specification support). Recent product extensions toward stainless-steel dual-action systems reflect a push into corrosive-environment and high-spec structural niches. Strategic implication: incumbents with bundled tool-product ecosystems can grow share in infrastructure contracts where specification continuity and service matter.

fischerwerke — Strong in approvals-driven productization (vinyl ester and epoxy systems) with recent updates expanding post-installed rebar positionings. Strategic implication: regulatory-approved system solutions continue to win in engineered retrofit and seismic projects.

Sika AG — Broad chemical portfolio with emphasis on high-performance epoxy anchors and approvals for potable-water and fire-resistant applications. Strategic implication: multi-certification strategies unlock public and utility procurement channels.

Simpson Strong‑Tie — Focused on faster-curing hybrid chemistries and structural connector integration; well-positioned in the North American commercial construction and repair market. Strategic implication: speed-to-cure and installation ergonomics drive contractor preference in time-sensitive projects.

2K Polymer Systems, Good Use, Fosroc, ATC and regional specialists (e.g., CELO, Bossong, MKT, Rawlplug, Klimas) — A mix of private-label capacity, regional approvals expertise and cost-competitive resin systems. Strategic implication: these firms are acquisition targets for multinationals seeking scale or for distributors seeking differentiated private-label offerings.

DEWALT (Stanley Black & Decker) — Moves to integrate chemical anchors with power-tool ecosystems indicate a convergence play: fastening system + tool + consumable. Strategic implication: expect more product bundles that streamline contractor workflows and lock-in consumables.

Recent product and certification moves — hybrid/acrylic fast-cure systems, stainless-steel 316 dual-action anchors, and re-positioning of vinyl ester approvals — point to three clear R&D priorities for market leaders in 2026: (1) broadened approval sets for seismic/post-installed rebar, (2) faster-cure chemistries for extreme environments, and (3) low-emission/styrene-free formulations for indoor projects.

Portfolio rationalization: Prioritize investments that combine approvals and installation productivity. For incumbents, maintain a two-track portfolio: high-margin certified systems for critical infrastructure and cost-competitive resins for less-demanding retrofit and MRO channels.

Certification roadmap: Allocate resources to secure Option‑1 style approvals (or regional equivalents) where seismic and post-installed rebar demand is material. The time-to-approval and test data are often the gating steps for project inclusion.

Procurement and raw-material strategy: Implement multi-year epoxy supply agreements or regional sourcing hubs to insulate margins from sharp resin price moves. Consider toll-filling partnerships in low-cost geographies for non-sensitive SKUs.

Go-to-market and channel expansion: Invest in contractor training, on-site technical support, and digital specification tools that reduce installation risk and improve repeat purchase. For distributors, creating “spec packages” that pair anchors with approved fasteners and installation tools increases stickiness.

M&A and alliances: Target private-label manufacturers and regional specialists with strong local approvals and channel access. Consider bolt-on acquisitions of dispensing-tool or cartridge manufacturers to capture more of the per-install value chain.

Sustainability and substitutes: Advance styrene-free and low-VOC formulations, and prepare for increasing buyer scrutiny on indoor-air-quality metrics in public and commercial buildings.

Based on deal‑level screening and competitive capability mapping, PW Consulting identifies the following near-term targets for strategic buyers and PE sponsors: private-label resin manufacturers with established filling capacity, regional players holding ETA/ETAG approvals in seismic hearts, dispensing and cartridge-system manufacturers, and providers with differentiated application engineering services. These asset classes shorten time-to-market for approvals, reduce capital intensity for new entrants and can immediately enhance channel coverage.

Executive summary and investment thesis for 2026–2032

Market-size reconciliations (2020–2025 historical), and a detailed, model-driven forecast (2026–2032) with scenario sensitivity to raw-material price and regulatory outcomes

Segment-level analysis by region, resin type and application, with demand drivers, pricing dynamics and elasticity matrices (note: detailed segment tables and unit economics are proprietary and available in the full report)

Regulatory and standards playbook — EAD/ETA pathways, testing timelines and checklist for Option variants

Supplier and channel matrix, including capability scoring, approval breadth, and M&A fit scores

Commercial playbooks, tender checklists, and contractor-adoption frameworks

Raw-material scenario analysis and procurement hedging strategies

Case studies demonstrating specification wins, retrofit projects and product bundles that improved share-of-wallet

PW Consulting’s Injection Mortar Anchors Market report is designed to be a decision-useful tool for executives setting 2026 budgets and three‑year roadmaps. Our clients use the analysis to prioritize certifications, size investments, plan M&A outreach and shape pricing and procurement strategies that are robust to resin-price shocks and changing approval regimes.

For the full dataset, proprietary segment tables, and actionable annexes (including supplier scorecards and a downloadable financial model), please contact PW Consulting or visit our website to request the complete report and client briefing.

For detailed analysis of this topic, please visit the official page:Injection Mortar Anchors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com