Recycled Rare Earths: Strategic Imperatives for 2026 — PW Consulting Preview of the Recycled Rare Earth Market Report

As global supply chains recalibrate under geopolitical pressure and electrification accelerates, recycled rare earths are shifting from niche sustainability projects to strategic industrial inputs. PW Consulting’s forthcoming Recycled Rare Earth Market report (base year 2025; forecast 2026–2032) synthesizes historical dynamics (2020–2025) and delivers the decision-grade analysis executives need to make confident capital, procurement, and policy-facing choices in 2026. This preview outlines the report’s strategic value, highlights market-scale context, summarizes critical competitive moves, and maps pragmatic steps for companies and policymakers — while intentionally retaining the report’s proprietary segment-level datasets to encourage engagement with the full analysis.

Recycled Rare Earth Market

Market Context at a Glance

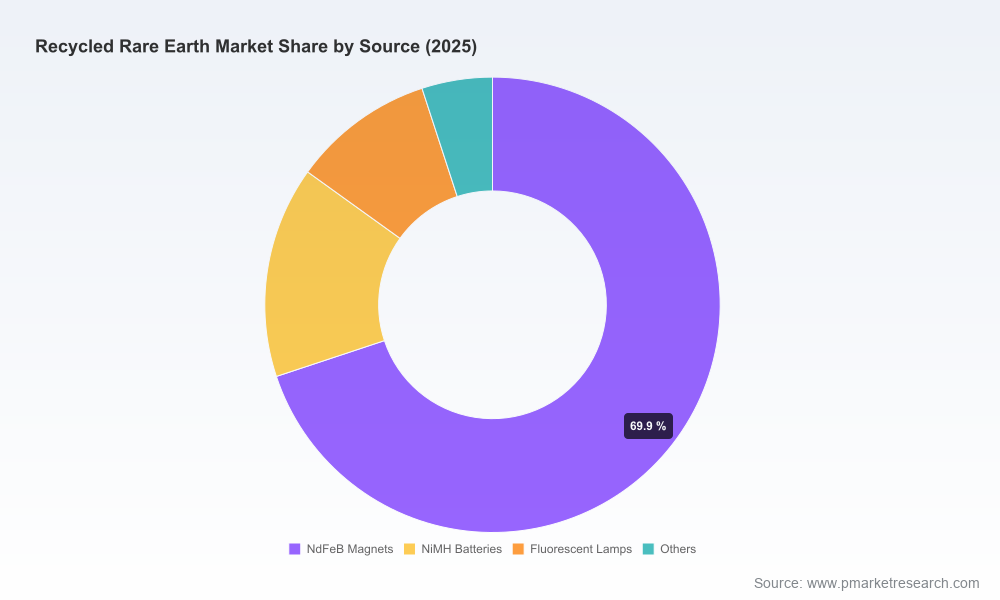

The recycled rare earths market has evolved from an emergent circular opportunity into a commercially material sector. Between 2020 and 2025 the market expanded substantially, reflecting rising collection rates, maturing hydrometallurgical and hydrogen-decrepitation processing routes, and early-stage commercial off-take agreements with OEMs. Our modeling shows the industry poised for sustained growth through 2032 on the back of structural demand for NdFeB magnet REEs and policy-driven incentives for domestic supply chains. PW Consulting’s forecast projects a robust compound annual growth rate (CAGR) of 12.7% over the 2026–2032 period, with the total market moving into the low‑to‑mid billions (USD) by the end of the forecast horizon.

Recycled Rare Earth Market

Why 2026 Is a Breakout Year

- Policy inflection points. Recent export control measures and follow-on announcements from major producing countries have injected supply-side uncertainty. Concurrently, tariff measures and domestic stimulus programs are scheduled to take effect in key consumer markets beginning in 2026, creating a window in which recycled material can capture strategic share.

- Commercial-scale recycling capacity comes online. Multiple producers are transitioning from pilot operations to multi-tonne commercial throughput, enabling supply reliability and cost competitiveness versus primary routes.

- OEMs are operationalizing circular sourcing. Several large manufacturers have executed or announced multi-year commitments to recycled-content magnets and have folded recycling suppliers into design-for-recyclability roadmaps.

Data-Driven Insights You Can Act On

PW Consulting’s report couples market-scale metrics with operational KPIs to produce a decision-oriented toolkit. Highlights include:

Recycled Rare Earth Market

- Supply-demand trajectories and sensitivity scenarios that quantify upside and downside pressure on recycled REE availability under alternate policy and scrap-collection assumptions.

- Integrated cost-benchmarks and unit economics for major recycling technologies, enabling rapid comparison of capex intensity, Opex drivers, and feedstock breakeven thresholds.

- An interactive supplier scorecard and capacity map (regional and technology overlays) that ranks commercial recyclers on technology readiness, feedstock flexibility, and scale-up risk.

- Commercial levers and contracting templates for off-take, tolling, and joint ventures designed to secure feedstock at scale while preserving margin capture.

- Regulatory impact matrices that translate export controls, tariffs, and extended producer responsibility policies into concrete procurement and capital planning triggers.

Note: This preview intentionally omits the report’s granular segment-by-segment datasets and price curves; the full intelligence package includes downloadable models and supplier-level volume forecasts that underlie the summary views presented here.

Competitive Landscape — Strategic Positions and Implications

The field of active recyclers and incumbent processors now spans innovative start-ups to integrated rare earth producers. Our qualitative assessment of key players identifies where strategic advantage is forming and where risks remain concentrated.

- Cyclic Materials (Toronto). Strengths: technically differentiated hydrometallurgical flowsheets and an integrated hub-and-spoke buildout in North America. Strategic implication: their campus expansion targets both scale and vertical integration, making them a prime partner for OEMs seeking nearshoring and traceability. Risk: execution and ramp timelines will be the primary value drivers to watch in 2026.

- MP Materials Corp. (Mountain Pass, USA). Strengths: an integrated REE producer with the advantage of processing capacity and high-profile commercial commitments that anchor recycled feedstock into existing magnet supply chains. Strategic implication: vertical integration and large OEM commitments de-risk demand for recycled material and accelerate downstream magnet manufacture with circular content. Risk: balancing primary and secondary feedstock economics and ensuring recycled inputs meet specification at scale.

- American Resources / Electrified Materials (Indiana). Strengths: rapid expansion of pre‑processing capability to consolidate diverse scrap streams domestically. Strategic implication: these capabilities create aggregation points that improve feedstock economics for downstream recyclers; companies dependent on consistent feed quality should prioritize supply agreements with such aggregators.

- Hitachi Metals (Japan). Strengths: mature magnet-to-magnet recycling processes and industrial partnerships in high-value applications. Strategic implication: their technology pedigree positions them as an attractive licensing or JV partner for manufacturers pursuing short-loop recycling strategies.

- HyProMag (Mkango) / University of Birmingham. Strengths: hydrogen processing and short-loop magnet fabrication demonstrate a low‑footprint circular route. Strategic implication: the technology is particularly compelling for high-performance magnet recycling where alloy properties must be preserved; OEMs with stringent magnetic performance requirements should engage early.

- Geomega, Umicore, Accurec, REEcycle, Carester. Strengths: a mix of specialized technology providers and broad metals recyclers bringing diverse processing options and geographic reach. Strategic implication: multi-source strategies that blend these capabilities will mitigate single‑technology risk and create resilience against policy shocks.

Recent Developments to Monitor in 2026

- Early-2026 capacity announcements from North American recyclers signal material increases in available secondary feedstock processing volumes, accelerating market liquidity.

- Large OEM commitments to recycled magnets — already public in several high-profile instances — are transitioning from headline statements to executable contracts, shaping offtake windows and quality requirements.

- Regulatory actions and temporary suspensions from major exporting countries create episodic premiuming for secure, traceable recycled content; buyers must factor geopolitical risk into procurement cost curves.

Strategic Recommendations for 2026 Decision-Makers

Based on our scenario modeling and supplier assessments, PW Consulting recommends a prioritized three-tier playbook for industrial players and investors planning for 2026:

- De‑risk supply through hybrid contracting. Combine short-term tolling agreements with medium-term off‑take contracts and conditional option rights on new recycling capacity. This approach secures material while preserving optionality as technologies and policies evolve.

- Invest in feedstock aggregation and pre‑processing. Aggregators that can cost-effectively homogenize and condition magnet waste create downstream scale and margin. For manufacturers, partnering with or investing in pre-processing hubs reduces feed variability and quality risk.

- Prioritize technology fit-for-purpose, not brand pedigree. Match processing routes to product performance requirements (e.g., short-loop magnet-to-magnet for high-performance alloys vs hydrometallurgical routes for commodity recovery). Include scalability and effluent/energy profiles in techno-economic decision matrices.

- Embed policy scenario planning into capital allocation. Use a tiered capex roadmap that links investment tranches to policy triggers (e.g., tariff activation, export control renewals, incentive programs) so capex is responsive rather than speculative.

- Operationalize traceability and chain-of-custody standards. Buyers should require auditable traceability to unlock premium green procurement pools and satisfy evolving regulatory disclosure obligations.

- Explore strategic alliances with OEMs and recyclers. Co-investment models and long-term offtake-for-infrastructure deals reduce commercialization risk and lock in recycled content commitments crucial to ESG and market security objectives.

What the Full Report Enables (and Why It Matters)

PW Consulting’s full Recycled Rare Earth Market report supplies the granular evidence base that turns strategic intent into executable plans. Subscribers receive:

- Proprietary supply-demand tables and price curve scenarios for 2026–2032 calibrated to policy, technology, and scrap‑collection sensitivity tests.

- Company-level capacity build schedules, technology readiness assessments, and a customizable supplier scorecard for integration into procurement RFPs.

- Negotiation playbooks for offtake and JV structures, plus model commercial terms that preserve upside while allocating technology and execution risk appropriately.

- Regulatory playbooks mapping jurisdictional dynamics to specific operational and compliance actions.

Because the value of recycling derives as much from access to reliable data and contracts as from chemistry and equipment, the report is purpose-built to shift conversations from “could we” to “how fast” and “at what terms.”

Closing: How to Use This Intelligence in 2026

Executives should treat 2026 as a staged decision year: secure near-term sources through flexible agreements, pursue selective investments that align with validated demand (especially where OEM commitments exist), and maintain an active posture on policy monitoring. Investors should prioritize enterprises demonstrating both technological differentiation and credible feedstock aggregation pathways. Policymakers should design incentive structures that accelerate collection infrastructure and transparent certification systems, rather than prescriptive technology mandates.

PW Consulting’s Recycled Rare Earth Market report offers the datasets, scenario tools, and commercial templates to operationalize these recommendations. For firms preparing procurement cycles, capital allocation decisions, or regulatory strategy in 2026, this analysis provides a rigorous, actionable foundation. Visit our report page to access the full dataset, interactive models, and supplier scorecards that underpin the conclusions summarized here.

For detailed analysis of this topic, please visit the official page:Recycled Rare Earth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com