Environmentally Friendly Carbonization Furnace Market — Strategic Outlook for 2026 Decisions

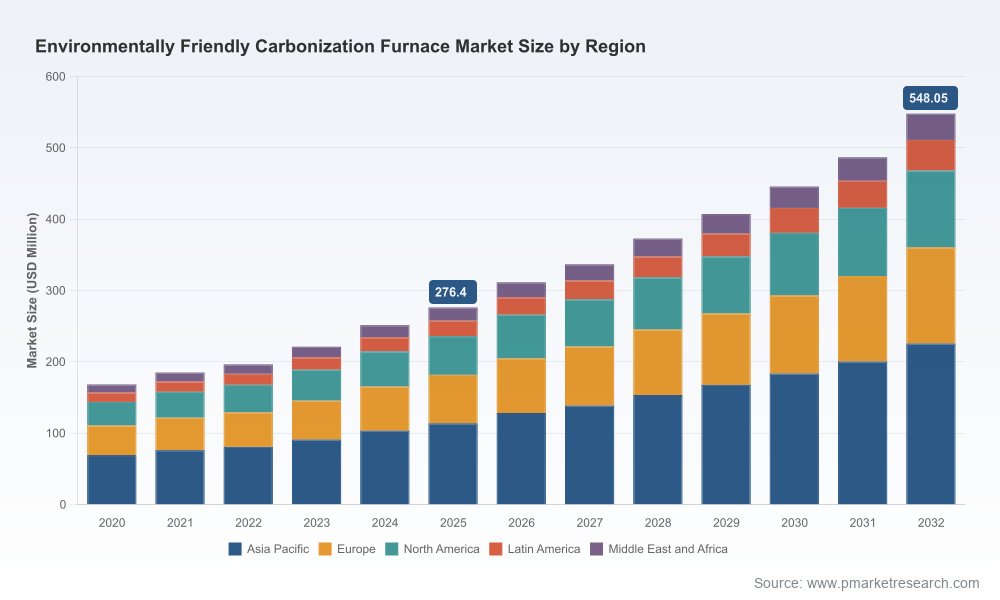

PW Consulting’s latest market research — Environmentally Friendly Carbonization Furnace Market — presents an action-oriented view of a technology sector entering a decisive growth phase. From 2020 through 2025 the market expanded rapidly, rising from roughly USD 168 million to USD 276 million. Our base-year analysis and modelling show the market expanding at a compound annual growth rate (CAGR) of 10.25% over the 2026–2032 forecast window, taking headline market value to the mid-hundreds of millions of USD by the end of the period. For executives planning capital allocation, supply-chain contracts, or strategic partnerships in 2026, this report synthesizes the market dynamics, vendor positioning, and deployment playbooks required to convert that growth into defensible commercial advantage.

Environmentally Friendly Carbonization Furnace Market

Why 2026 is a Strategic Pivot

Three converging forces make 2026 a pivotal year for firms in the carbonization furnace ecosystem:

Environmentally Friendly Carbonization Furnace Market

- Regulatory tightening and standards adoption: North American and European regulatory frameworks increasingly prioritise low-emission enclosed pyrolysis systems and validated carbon sequestration claims. Compliance timelines and permitting complexity will accelerate buyer preferences for fully enclosed, low-emission furnace architectures.

- Commercialisation of higher-value end-markets: Demand for biochar and biocarbon in soil health, water treatment, industrial carbon replacement, and specialty materials has matured from pilot-stage procurement toward long-term offtake and industrial-scale integration. Buyers will prioritise consistency, traceability, and product certification.

- Technology and automation inflection: Recent product upgrades and acquisitions across the vendor landscape indicate an industry-wide shift toward automated thermal control, integrated emissions management and scalable continuous processes—capabilities that materially affect unit economics and risk profiles.

What the Report Delivers — Practical Intelligence for 2026 Decisions

This study is designed as an operational playbook as much as a market forecast. Users will find:

Environmentally Friendly Carbonization Furnace Market

- Forecast-driven investment framing: Top-down and bottom-up models aligned to our 2026–2032 forecast that let CFOs stress-test capacity expansion plans under multiple demand and regulatory scenarios.

- Plant-level CapEx and OpEx templates: Modular cost templates and build schedules for batch, continuous and rotary kiln systems, with sensitivity matrices for feedstock mix, moisture, and scale that impact thermal efficiency and product yield.

- Vendor benchmarking and procurement scorecards: Comparative assessment across technology readiness, lifecycle emissions, automation maturity and after-sales capability — built to inform RFIs and vendor shortlists.

- Feedstock and offtake mapping: Practical guidance for securing agricultural and forestry waste streams, contracting structures, and counterparty diligence to underpin long-term feedstock availability without exposing buyers to excessive price or quality volatility.

- Regulatory and compliance playbook: Permitting roadmaps, emissions-testing approaches and third-party carbon measurement & verification frameworks that buyers and financiers increasingly require.

- Risk registers and mitigation tactics: Actionable measures for supply-chain bottlenecks, performance guarantees, insurance structures, and contingency plans for feedstock substitution or technology underperformance.

Note: This announcement is deliberately summary in nature. The full report contains granular region-by-region and application-by-application forecasts, detailed vendor scoring tables, and downloadable plant-level financial models; those segment-level datasets are not included in this release to protect the analytical value offered in the full deliverable.

Competitive Landscape — Profiles and Strategic Moves

The market remains moderately fragmented, with the top three suppliers accounting for a material but not dominant share of global shipments and the top five increasing that concentration — a structure that leaves room for both organic scaling and M&A-driven consolidation. Key players profiled in the report include:

- GreenPower LTD (Europe; facilities in Ukraine, Indonesia, South Korea) — A technology-centric vendor known for patented batch and continuous designs. Recent product evolution includes the BIO-KILN rebrand and an upgraded BIO-CARBON continuous system featuring the ACS 2026 automation package (announced May 2026). This enhancement improves thermal control and product consistency, signalling a push toward industrialised continuous processing for global OEM customers. (See company: https://greenpower.equipment)

- Beston Group Co., Ltd. (Zhengzhou, China) — A high-volume supplier of carbonization systems, with proven multi-feedstock continuous operation capability demonstrated by extended continuous runs. Its focus remains on exporting modular systems and scaling turnkey installations for waste-to-resource projects.

- Wilson Biochar, LLC (USA) — Emphasises on-site, lower-capacity biochar kilns tailored for agricultural and land-management buyers focused on carbon sequestration and soil amendment. The firm’s product-market fit is notable in decentralised and agrarian deployment models.

- Zhengzhou Shuliy Machinery, Tianjin Mikim Technique and Zhengzhou Belong Machinery — These manufacturers anchor the cost-competitive segment with a portfolio of continuous and batch furnaces targeting commodity charcoal and biochar production at different scales. Their strategic advantage is supply-chain integration for common biomass feedstocks.

- CHAR Technologies Ltd. (Toronto, Canada) — A technology and project developer with capabilities spanning high-temperature pyrolysis and scaled biocarbon production. Notable moves include a commercial pilot for PFAS destruction integrated with biochar/syngas production (initiated 2025) and a strategic acquisition of biocarbon assets in Québec (April 2026), strengthening feedstock-to-facility execution capability. (See company: https://www.chartechnologies.com)

Collectively, these players illustrate two parallel market dynamics: product differentiation through automation and emissions control, and consolidation through asset acquisition and strategic partnerships. Buyers should map vendor capability not only to price and capacity, but to lifecycle emissions and product traceability — criteria increasingly weighted by regulators and end-market offtakers.

Decision Frameworks for 2026

Below are the priority decision levers we recommend organisational leaders use when building carbonization furnace strategies in 2026:

- Technology choice aligned to value capture: Match furnace architecture (batch vs continuous vs rotary) to offtake characteristics: continuous plants suit high-volume, certified offtake contracts; batch may be preferable where feedstock variability and decentralised deployment matter.

- Permitting-first siting: Factor permitting timelines and emissions testing at the earliest site selection stage; delays here are the dominant source of schedule slippage in our project database.

- Secure feedstock via layered contracting: Blend short-term spot agreements with medium-term supply contracts and embedded community sourcing to hedge against supply interruption and reputational risk.

- Design for verification: Specify measurement points, sample regimes and third-party verification clauses in procurement documents to support future carbon crediting or sustainable procurement claims.

- Modular scaling and financing: Consider staged capacity additions with standardised modules to de‑risk first-of-kind operations and to facilitate predictable commissioning and financing milestones.

- Vendor risk and performance bonding: Insist on performance acceptance tests and availability guarantees tied to liquidated damages, especially for continuous systems where uptime materially alters unit economics.

Key Performance Indicators and Monitoring

Operational KPIs that should be central to dashboards and M&A diligence include:

- Plant availability and run-time cadence

- Thermal efficiency and specific energy consumption

- Product consistency (carbon content, particle size, moisture)

- Emissions intensity per tonne of feedstock processed

- Feedstock variability tolerance (percentage of operations within spec)

- Opex per tonne processed and per tonne of final product

Risks to Monitor and Mitigation Options

Key risk vectors for 2026 and recommended mitigations include:

- Policy risk: Rapid changes in emissions standards — mitigate with transactional flexibility in contracts and technology upgrade pathways.

- Feedstock risk: Price and quality volatility — mitigate through diversified sourcing and inventory strategies.

- Technology adoption risk: Integration and scale-up failure — mitigate with staged commissioning, third-party FAT/SAT and vendor performance bonds.

- Market risk: End-market acceptance and pricing pressure — mitigate via offtake pre-commitments and product certification strategies.

- Reputational risk: Questioned sequestration claims — mitigate through independent MRV (measurement, reporting and verification) frameworks and transparent supply-chain traceability.

How PW Consulting’s Report Helps Executives Execute in 2026

Executives preparing CAPEX approvals, supply agreements, or M&A plays will find the report’s synthesis tailored to decision-making timelines common in 2026: procurement-ready vendor shortlists, plant-level financial models, step-by-step permitting playbooks, and scenario-based valuation adjustments for different regulatory trajectories. Our modelling and vendor benchmarking emphasise measurable performance attributes (automation, emissions control, modularity) that directly influence financing terms and offtake negotiation leverage.

This announcement intentionally omits the granular segment-level tables and region-by-application breakdowns that financial sponsors and project developers rely upon when finalising commitments. Those detailed datasets, together with downloadable cost-model spreadsheets and a dynamic vendor database, are included in the full PW Consulting report and accompanying subscription services.

Next Steps

For corporate strategy teams, investors and project developers, the next pragmatic steps in 2026 are clear: prioritise technologies and vendors that can demonstrably meet tightening emissions standards while delivering consistent product quality; structure offtake and feedstock contracts to de-risk revenue and input inputs; and pursue modular, staged expansion to align capital deployment with market proof points. PW Consulting stands ready to provide bespoke briefings, model customization, and vendor due-diligence packages that convert the market’s growth outlook into executable projects and financings.

To understand the full depth of our analysis, access detailed segment forecasts, or arrange a client briefing, please contact the PW Consulting research team for the full report and database access.

For detailed analysis of this topic, please visit the official page:Environmentally Friendly Carbonization Furnace Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com