US Magnet Bearings Industry Insights Technology Developments and Market Trends

Other |

2026-01-15 09:34:26

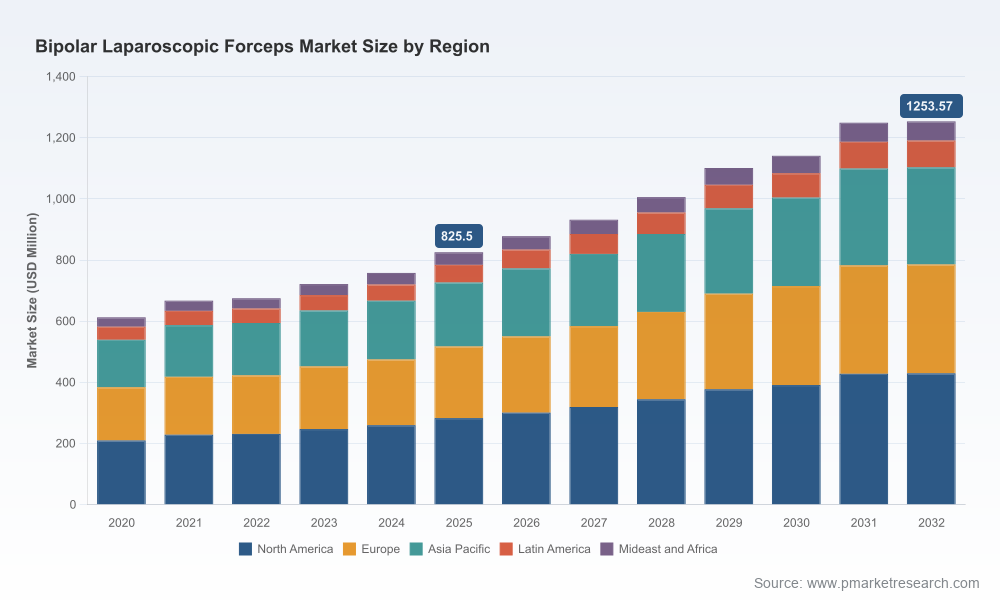

PW Consulting’s latest market study on the Bipolar Laparoscopic Forceps market delivers a decision-grade intelligence suite designed to guide corporate strategies through 2026 and beyond. Built on a 2020–2025 historical analysis and a 2026–2032 forecast horizon, the report quantifies a clear growth trajectory (CAGR 6.15%) and positions the market to exceed USD 1.25 billion by the end of the forecast window. For executive teams weighing capex, R&D prioritization, or M&A, this brief summarizes the strategic takeaways and operational playbook elements that matter most—while reserving the full segmentation matrices and proprietary scenario outputs for the full report.

Bipolar Laparoscopic Forceps Market

Actionable foresight timed to budgeting cycles: 2026 will be a pivotal planning year for product launches, procurement contracts, and platform integrations. Our study translates macro growth (mid-single-digit CAGR) into concrete demand drivers—clinical workflows, sterilization economics, and sustainability pressures—so teams can prioritize investments that generate ROI by 2028–2030.

Bipolar Laparoscopic Forceps Market

De-risking portfolio choices: Whether evaluating reusable versus disposable architectures or new material investments (e.g., PVC-free disposables), the report blends clinical, regulatory, and commercial inputs to quantify breakeven horizons and sensitivity to utilization shifts.

Bipolar Laparoscopic Forceps Market

Competitive positioning and consolidation signals: With the market exhibiting moderate concentration (CR3 ~42.5%; CR5 ~55.8%), we identify where scale matters, where adjacency plays win, and which niches remain attractive for challengers.

Our top-line model places the global Bipolar Laparoscopic Forceps market at approximately USD 825.5 million in 2025, with projected expansion to roughly USD 878 million in 2026 under the base-case forecast. By 2032 the market is expected to surpass USD 1.25 billion. This steady growth is being driven by a mix of procedure volume recovery, technology substitution, and incremental per-procedure device spend as hospitals seek to shorten OR time and reduce conversions to open surgery.

Implications for corporate strategy:

Revenue planning: Firms should model mid-single-digit topline growth while stress-testing for faster substitution in regions that accelerate disposable adoption or implement PVC-free mandates.

R&D prioritization: Investment choices between durable, sterilizable instruments and single-use disposables require an explicit view on sterilization economics, instrument life-cycle costs, and environmental policy traction.

Procurement renegotiation: Health systems can leverage forecasted growth and supplier concentration data to time multi-year purchasing commitments or demand value-added services (training, maintenance, instrument traceability).

Regulation and sterilization: Laparoscopic bipolar forceps are governed as Class II devices in key markets. Reusable instruments require robust cleaning, inspection, and sterilization workflows (gravity, ETO, low-temperature plasma systems). The operational burden of reprocessing is a determinative factor in the reusable vs. disposable trade-off.

Materials and sustainability: The emergence of PVC-free disposable options reflects both environmental pressures and procurement preferences. Manufacturers who can combine low environmental footprint with comparable performance will have a differentiated commercial argument.

Reimbursement and coding: Common procedural coding conventions influence hospital economics for minimally invasive approaches. Procedural codification can materially impact uptake curves for advanced bipolar devices that reduce OR time or complications.

The market is populated by a mix of global medtech majors, specialized device firms, and regional manufacturers. The report includes in-depth profiles, capability maps, and strategic assessments for the leading players, including:

B. Braun / Aesculap (Melsungen, Germany) — a systems and consumables player offering both reusable and single-use bipolar forceps, with a recent R&D focus on irrigating and non-stick technologies to improve coagulation efficiency.

Medtronic (Dublin, Ireland) — leverages energy-platform compatibility and clinical evidence around precision coagulation as a channel advantage; strategy centers on platform-led instrumentation sales and clinical training programs.

Karl Storz (Tuttlingen, Germany) — known for rotating bipolar dissectors in multiple diameters and deep penetration into laparoscopic gynecology and general surgery workflows; competitive edge is instrument ergonomics and procedure-specific assortments.

Boer Medical (Hangzhou, China), Zhejiang Geyi Medical Instrument (China), and Advin Health Care (Ahmedabad, India) — regional manufacturers emphasizing cost-competitive disposable and reusable lines and fast SKU expansion into emerging markets.

Purple Surgical (United Kingdom) — innovating on multi-function bipolar cutting forceps that combine dissection, coagulation, and transection in a single instrument to reduce instrument exchanges and OR time.

Recent product launches underscore how incumbents are competing on features beyond basic performance: in October 2025, Aesculap launched an irrigating disposable bipolar forceps with higher irrigation output and non-stick coatings; earlier, in July 2024, a European supplier introduced PVC-free disposable options targeting environmental stewardship. These moves signal a two-front competition—clinical performance and material sustainability.

The full PW Consulting report is built as a practical toolkit rather than a static narrative. Key deliverables include:

Top-line market model and scenario suite (base, upside, downside) with sensitivity levers for procedure mix, disposable penetration, and sterilization cost inputs.

Competitive benchmarking dashboard with CR3/CR5 analysis, product feature matrices, pricing bands, and go-to-market archetypes.

Commercial playbook: value propositions by buyer persona (hospital procurement, ASC operators, ambulatory centers), negotiation levers, contract structures, and service bundle options.

Product strategy toolkit: modular R&D roadmaps, adoption curve templates, and a product launch checklist aligned to regulatory and sterilization constraints.

M&A and partnership screening: target heatmaps, due-diligence checklists focused on regulatory compliance, sterilization validation, and supply-chain resiliency.

Operational levers for supply chain and cost-to-serve optimization, including third-party sterilization and instrument management programs.

To preserve commercial value for clients, the report previews aggregated segment trends and concentration metrics while withholding detailed regional and application-level tables that are available in the full deliverable.

Align product roadmaps to sterilization economics: Model TCO across sterilization approaches and time-to-recovery for capitalized sterilization assets. If reprocessing costs exceed a defined threshold, disposables or hybrid leasing can be competitive.

Differentiate on sustainability and materials compliance: Fast-followers should prioritize PVC-free and low-epoxy designs where procurement policies favor environmental attributes.

Leverage platform integration: For firms with energy platforms or electrosurgery ecosystems, instrument compatibility and bundled training can protect premium pricing and raise switching costs.

Calibrate commercial coverage to concentration dynamics: In markets where top players control majority share, challengers should pursue focused clinical niches or service-led value propositions to gain traction.

Pursue targeted M&A to fill capability gaps: Use buy-build options to accelerate access to complementary materials, sterilization validation expertise, or regional distribution channels.

Our approach combines a granular understanding of clinical workflows, device lifecycle economics, and supplier positioning to produce a roadmap that is both strategic and executable. The report translates the market’s mid-single-digit CAGR and estimated billion-dollar trajectory into specific investment thresholds, prioritized product features, and procurement playbooks that will influence outcomes in the 2026 planning window.

Executives who integrate these findings into capital and product planning processes will be able to prioritize projects that turn growth into sustainable share gains while avoiding common pitfalls related to reprocessing liabilities, materials non-compliance, and misaligned go-to-market execution.

This brief highlights the most consequential insights for 2026 decision-making while reserving the full segmentation tables, regional and application-level forecasts, and proprietary scenario outputs for the full report. For access to the complete dataset, interactive dashboards, and client workshops that operationalize the playbook, please visit the PW Consulting report page or contact our advisory team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Bipolar Laparoscopic Forceps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com