Experts Predict Robust Growth in US Slot Machine Equipment Sector

Other |

2026-06-12 10:47:11

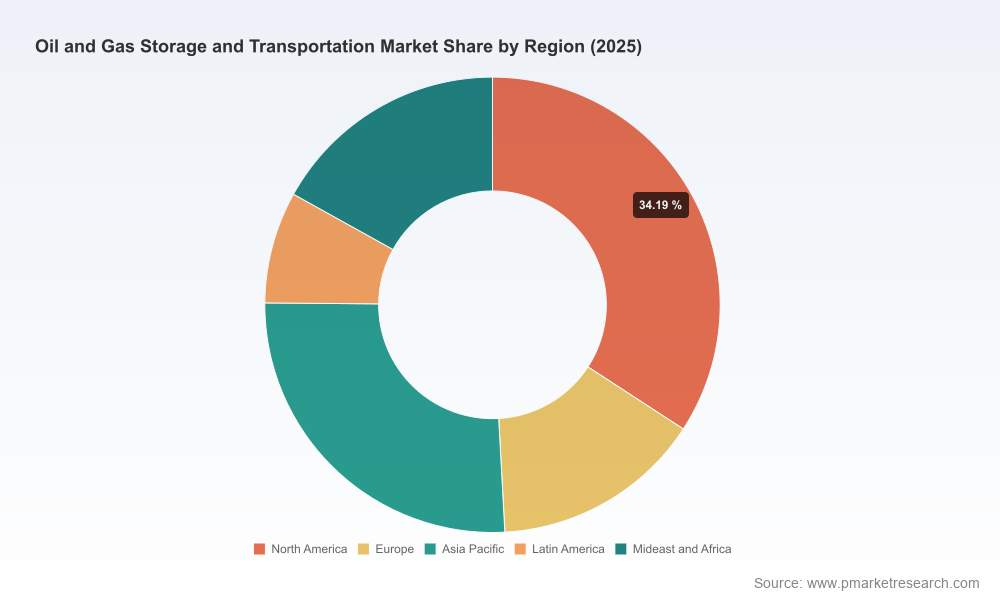

PW Consulting’s latest market study on Oil & Gas Storage and Transportation synthesizes macro trajectories, operational levers, and competitive dynamics into an actionable roadmap for corporate decision‑makers working against the 2026 planning horizon. Built on a 2025 base and a 2026–2032 forecast window, the report models an industry that continues to expand—at a compounded annual growth rate of 5.28%—from a market scale of roughly USD 571 billion in 2025 to an anticipated market approaching USD 819 billion by 2032. This release is intended as a strategic “preview”: it surfaces the essential trends, risk vectors and playbooks executives need now, while reserving the granular, segment‑level datasets for subscribers and report purchasers.

Oil And Gas Storage And Transportation Market

Timing: 2026 is an inflection year where legacy infrastructure, emergent policy, and shifting commodities inventories interact. Our model integrates observed industry shifts through 2025 and projects practical capacity and throughput scenarios through 2032, enabling near‑term CAPEX prioritization and multi‑year supply‑chain decisions.

Oil And Gas Storage And Transportation Market

Decision relevance: The report translates macro forecasts into operational decisions—portfolio prioritization, contract strategy, M&A targets, and contingency planning—so boards and CEOs can convert topline projections into executable tactics.

Oil And Gas Storage And Transportation Market

Risk calibration: We quantify volatility drivers—inventory dynamics, geopolitical pipeline projects, strategic reserve actions, and regulatory trajectories—and map them to probability‑weighted outcomes that matter to CFOs and asset managers.

Resilient growth with differentiated returns: While the aggregated market shows steady expansion at a mid‑single‑digit CAGR, value is migrating to nodes that combine storage flexibility with transportation optionality. Investors will see superior risk‑adjusted returns from assets that can shift between products and delivery modes as seasonal and strategic stock movements evolve.

Inventory overhang and episodic draws: Global observed oil inventories reached their highest recent level in early 2026. At the same time, significant month‑to‑month draws and localized floating storage increases indicate episodic stress points in physical logistics. Firms must plan for both sustained elevated inventory baselines and short, intense liquidity events that strain terminal and pipeline throughput.

National champions vs independents: Market concentration analyses show limited dominance by a handful of large players, with meaningful share still dispersed among regional incumbents and independents. This structure produces opportunities for niche operators and joint ventures—particularly where national oil companies or sovereign projects require partner expertise for rapid scale‑up.

Decarbonization as a business line: Existing oil & gas transport and storage networks constitute valuable backbone infrastructure for emerging carbon transport and storage (CTS) systems. Policy‑driven targets for CO2 movement and storage create near‑term repurposing and retrofit opportunities for terminals and pipelines, unlocking alternative revenue streams and extending asset lives.

Project pipeline and geopolitics shape access: Major offshore pipeline projects entering operations around 2026, together with regionally concentrated contract awards and strategic reserve exchanges, will reconfigure flow patterns. Operators must update flow‑assurance modeling and contractual terms to reflect shifting source/destination pairs and enhanced geopolitical contingency planning.

Proprietary market forecast model (2026–2032) calibrated to 2020–2025 observed performance and forward scenarios; model outputs are available at market and asset levels for subscribers.

Supply‑chain stress tests and throughput sensitivity matrices that map inventory shocks and pipeline outages to terminal utilization and pricing differentials.

Contract and commercial playbooks: standard and non‑standard contracting templates, tolling/fee recommendations, and clauses to protect operators in volatility episodes.

M&A and JV deal architecture: target screening criteria, valuation ranges, due diligence checklists focused on storage integrity, environmental liabilities, and product conversion potential (e.g., LNG, NGL, chemical feedstocks).

Asset retrofit and decarbonization blueprints: engineering and commercial roadmaps to integrate carbon transport, hydrogen readiness, and low‑emissions operational practices into storage and pipeline assets.

Regulatory and policy tracker with immediate impacts to permitting, strategic reserve interaction, and emissions compliance—mapped to regional decision nodes that affect scheduling and capex phasing.

Performance benchmarking and KPI dashboards, enabling operators to compare throughput efficiency, storage utilization, and unit economics while preserving confidentiality through anonymized peer sets.

The market exhibits a mix of global independents, integrated midstream majors, and state‑backed operators. Our competitive review synthesizes strengths, strategic intent, and likely moves for the firms that will set the tone for 2026 engagements.

Global terminal specialists: Companies with extensive international terminal networks and multi‑product capability retain commercial optionality. Their strength lies in flexibility to capture arbitrage between crude, refined products, and chemicals.

North American midstream giants: Operators that combine pipeline reach with substantial storage assets will continue to dominate regional flows and exert pricing influence on access fees and throughput prioritization.

Integrated national players: Sovereign companies with deep logistical footprints and state support can move quickly on large capex projects and strategic stock placements; their project timelines and contract appetites are pivotal for regional developers.

Independents and niche providers: Specialized operators can win by offering modular storage solutions, flexible commercial terms, or by becoming the integration partner for carbon and hydrogen infrastructure retrofits.

We profile leading companies in the public domain to illustrate these dynamics: global independent terminal operators with multi‑country terminal networks; U.S. and Canadian pipeline and storage majors with vast corridor control; Gulf region national operators executing multi‑billion‑dollar field and downstream programs; and regional providers with strategic coastal or inland storage nodes. The full report provides detailed company scorecards, balance‑sheet exposure maps, and scenario‑based threat assessments for each named player.

Strategic reserve activity: Recent government exchanges of strategic inventory in 2026 have blurred the line between commercial and emergency storage demand, creating short‑term capacity squeezes in locations tied to official stock movements.

Major contract awards: Large engineering and construction contracts tied to new field developments and pipeline expansions have cascading effects on logistics demand and create opportunities for local storage and export capacity growth.

Project start‑ups and offshore pipelines: The commissioning of significant pipeline corridors in 2026 alters regional flow economics and may result in stranded capacity in legacy routes if operators do not adapt commercial terms.

Regulatory and demand shifts: Projections for reductions in transportation energy demand under stringent emissions scenarios alter long‑run product demand mixes and should influence long‑term storage allocation and terminal specialization decisions.

Adopt a modular CAPEX posture: Prioritize investments that increase optionality—convertible tanks, multi‑grade piping, and modular meter and custody transfer systems—because optionality protects value in volatile inventory regimes.

Stress‑test contractual exposure: Revisit long‑term take‑or‑pay and throughput contracts with counterparties, and build contingency clauses for government interventions and major project delays.

Pursue selective partnerships: Where national projects or large field developments present scale opportunity, structure risk‑sharing JVs that offer local access while limiting balance‑sheet concentration.

Accelerate decarbonization monetization: Convert suitable pipeline and storage corridors for carbon or low‑carbon carriers where feasible; the economics of CTS and hydrogen readiness are improving for well‑located assets and can materially alter asset life‑cycle value.

Update operating playbooks: Invest in inventory forecasting, flow optimization tools, and dynamic pricing engines to capture arbitrage and minimize idle capacity loss during episodic inventory swings.

The study’s base year is 2025, with a historical foundation spanning 2020–2025 and a forecast horizon from 2026 to 2032. The headline CAGR used across scenarios is 5.28%. Data inputs combine operator disclosures, trade flows, satellite and AIS shipping analytics, regulatory filings, and PW Consulting’s proprietary demand‑supply model. Confidentiality filters are applied to ensure firm‑specific insights are presented as anonymized benchmarks unless permissioned by the operator.

This briefing is designed to surface high‑value strategic insight and operational implications. For boards, strategy teams, and asset managers requiring the full suite—detailed segment and regional breakdowns, terminal‑level datasets, company scorecards with financial overlays, and the downloadable forecast model—please access the report landing page. The full report includes the granular tables and appendices that underpin the summaries above; this preview intentionally withholds segmented numeric tables to preserve the actionable exclusivity of the purchased dataset.

PW Consulting’s Oil & Gas Storage and Transportation Market study is built to convert macro forecasts into executable plans for 2026 and beyond. If your 2026 strategy depends on aligning capital spend, contractual posture, or M&A activity with the rapidly evolving logistics and storage landscape, this report is designed to be the operational backbone of that work.

For detailed analysis of this topic, please visit the official page:Oil And Gas Storage And Transportation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com