North America Padded Mailers Market Overview: Key Drivers and Challenges

Other |

2026-04-09 07:41:03

PW Consulting’s latest industry study on the Digital Inclinometer Market delivers a concise, transaction-focused intelligence pack designed for procurement leaders, product strategists, and corporate development teams planning for 2026. Built from five years of historical tracking and a seven-year forecast horizon, the report benchmarks the market’s maturation: from a mid‑hundreds million USD sector in 2025 to a materially larger opportunity by 2032, underpinned by a 6.3% compound annual growth rate (CAGR). This briefing highlights the decision‑critical implications, the competitive posture of incumbent suppliers, and the pragmatic tools we include to accelerate confident investment, sourcing, and product decisions next year.

Digital Inclinometer Market

Procurement and capital planning cycles in industrial, construction, and infrastructure sectors are aligning around multi‑year SHM (Structural Health Monitoring) programs and renewable energy deployments. These programs create windows in which sensor platform choices become long‑tail commitments.

Digital Inclinometer Market

MEMS technology has become the default engineering approach in digital inclinometers because it balances precision, size, power consumption, and unit economics—shifting buyer preferences toward integrated, network‑ready sensors rather than bespoke mechanical solutions.

Digital Inclinometer Market

Quality management and regulatory signals — such as recent ISO 9001 follow‑up audits within the vendor base — reduce supplier risk for large projects and accelerate the inclusion of electronic inclinometers into safety‑critical architectures.

Tactically, 2026 is the year to convert pilot deployments into platform standards. Decisions made this year will cascade into multi‑year service agreements, analytics investments, and maintenance contracts.

The full PW Consulting report is structured to support live decision processes rather than serve as a theoretical textbook. Key deliverables include:

Independent market sizing and forecast model (base year: 2025) with scenario runs for conservative, central, and high‑adoption paths through 2032; model assets are provided in editable format for M&A and strategic planning use.

Decision frameworks and procurement templates — RFP language, technical specification checklists, and a supplier due‑diligence scorecard calibrated to reliability, environmental ruggedness, and interface compatibility (e.g., RS‑232/RS‑485/Modbus, CAN, networked protocols).

Commercial benchmarking — pricing bands, warranty structures, and aftermarket service models, with negotiation playbooks by buyer archetype (OEM, contractor, asset owner).

Technology and product taxonomy — performance tradeoffs between MEMS, force balance, and optical inclinometers, and guidance on selecting sensor architectures by use case.

Go‑to‑market and channel strategy blueprints for vendors and distributors seeking to capture share in solar tracking, slope monitoring, and machinery safety segments.

M&A and partnership screening — a prioritized list of capabilities that create roll‑up value (e.g., embedded firmware IP, field calibration services, integrated telemetry), plus an early‑warning risk register tied to supplier concentration and component sourcing risks.

Case studies and ROI calculators — real‑world TCO examples for typical deployment topologies and sample sensor fleet lifecycles that buyers can adapt for internal business cases.

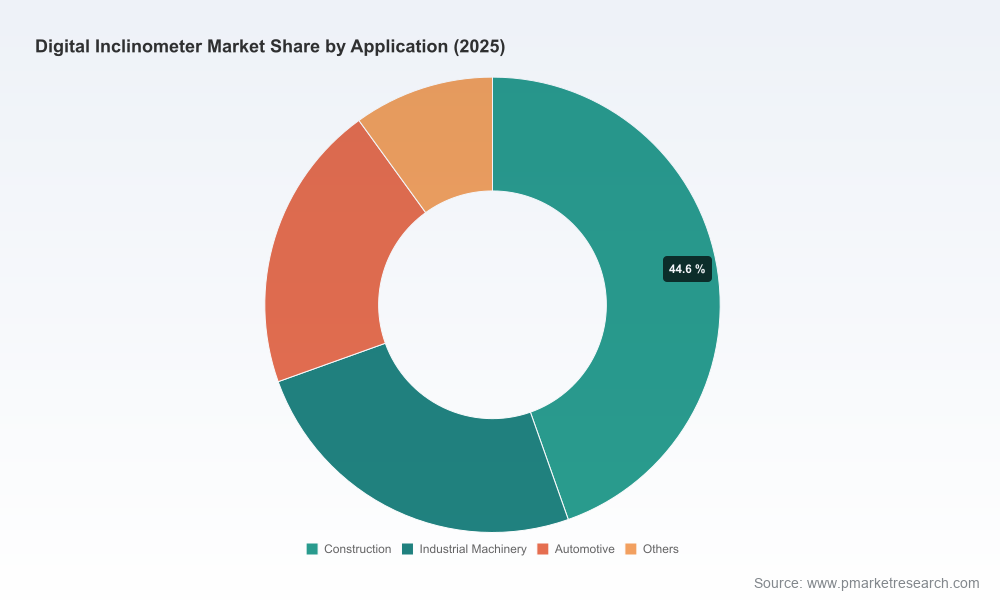

Historically the market has expanded at a steady clip, reflecting rising demand in structural health monitoring, machinery safety, and renewable energy tracking systems. By anchoring to our base year (2025), users can see how near‑term vendor strategies and procurement schedules impact medium‑term financials. From a strategic finance perspective, the projected mid‑single digit CAGR through 2032 highlights two practical implications:

For buyers: unit price pressure will remain real as scale and MEMS commoditization continue, but total spend can grow materially as fleets proliferate and connectivity/analytics services are purchased alongside hardware.

For vendors and investors: margin expansion is achievable through software and service layers, not purely hardware differentiation. The route to premium valuation goes through integrated monitoring offerings and long‑duration service contracts rather than incremental sensor improvements alone.

The market’s competitive map is populated by specialist sensor houses, geotechnical system integrators, and electronics majors. Rather than a single dominant platform, buyers face a mix of vertically integrated suppliers and niche innovators. Below we summarize the strategic posture of principal vendors tracked in the study:

Jewell Instruments (Manchester, NH, USA) — A strong player in MEMS and force balance inclinometers offering single, dual, and tri‑axis devices with both analog and digital outputs (RS‑232, RS‑485, Modbus). Jewell’s recent product refreshes emphasize higher resolution and faster response, signaling a continued focus on performance differentiation for industrial and harsh‑environment customers.

GEOKON (Lebanon, NH, USA) — Specialized in geotechnical inclinometer solutions, including spiral indicator probes and in‑place inclinometer systems used for slope stability and structural monitoring. Their product set is tailored to long‑term monitoring projects, making them a preferred partner for infrastructure owners and consulting engineers.

US Digital (Vancouver, WA, USA) — Offers absolute optical and networked inclinometer models with full 360° range and high resolution, aimed at applications requiring precision and range, such as solar tracker control and marine dredging operations.

Level Developments Ltd (Croydon, UK) — Focused on digital inclinometers and OEM tilt sensors, including temperature‑compensated devices for solar and industrial use. Their product catalog emphasizes cost‑effective dual‑axis sensors for mainstream tracking and machine control applications.

Rieker Inc (Aston, PA, USA) — Concentrates on vehicle and boom angle monitoring, with product lines targeted at mobile equipment manufacturers and fleet integrators.

Fredericks Company (Huntingdon Valley, PA, USA) — Provides a broad range of analog and digital sensors with wider angular ranges and legacy serial protocols; well suited to precision industrial and environmental sensing tasks.

TE Connectivity (Schaffhausen, Switzerland) — Supplies AXISENSE series sensors with automotive‑grade interfaces (e.g., CAN J1939) and solutions tailored to platform leveling and tip‑over protection in harsh operational environments.

Recent vendor activity underlines two themes relevant to 2026: (1) quality and process certifications are driving buyer confidence (e.g., supplier ISO audit completions), and (2) product refresh cycles emphasize higher resolution MEMS sensors and temperature compensation for field robustness. Examples include product introductions and catalog updates across the vendor base that prioritize integration-friendly interfaces and solar‑tracking suitability.

Run a supplier segmentation exercise now: split suppliers by capability (hardware IP, field services, systems integration) and align contracts to desired outcomes (hardware supply vs. monitoring as a service).

Prioritize interface compatibility and lifecycle management in RFPs — insist on open protocols and firmware update pathways to avoid lock‑in and to enable future analytics upgrades.

Negotiate bundled agreements that shift value capture from unit hardware to software/subscription tiers; include performance SLAs tied to measurement accuracy and availability.

Build a supplier risk register focused on component sourcing (critical MEMS die availability) and quality certification status; accelerate dual‑sourcing where uptime is mission‑critical.

Consider strategic partnerships or tuck‑in acquisitions to acquire calibration services, site installation capabilities, or cloud analytics that accelerate recurring revenue streams.

Embed field validation pilots into procurement contracts with staged payments tied to performance milestones to derisk large rollouts.

To preserve its value as a commercial, transaction‑ready product, the full PW Consulting report contains granular segmentation (by region, by sensor type, by application), vendor share tables, modelled price curves, and deal‑level comparators — elements intentionally omitted from this briefing. If your 2026 strategy requires line‑item pricing, regional demand scenarios, or a validated list of short‑ and mid‑term acquisition targets, the complete dataset and supporting models are available through PW Consulting’s report portal.

Accessing the full report provides: editable forecast models, supplier due‑diligence templates, RFP language, and a prioritized action plan tailored to buyer type. These assets are designed to be dropped into procurement workflows and strategic planning cadences to materially reduce time to decision and execution risk.

In short, the Digital Inclinometer Market is transitioning from a specialist niche into an integrated component of broader monitoring and automation stacks. For 2026, the critical choices are less about sensor selection in isolation and more about who provides the data‑to‑decision chain. PW Consulting’s report arms teams with the market sizing, procurement tools, and competitive intelligence needed to make those choices deliberately and with conviction.

For detailed analysis of this topic, please visit the official page:Digital Inclinometer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com