Die Rolle der Künstlichen Intelligenz in Online-Casinos: Chancen und Herausforderungen

Games |

2026-06-15 16:36:25

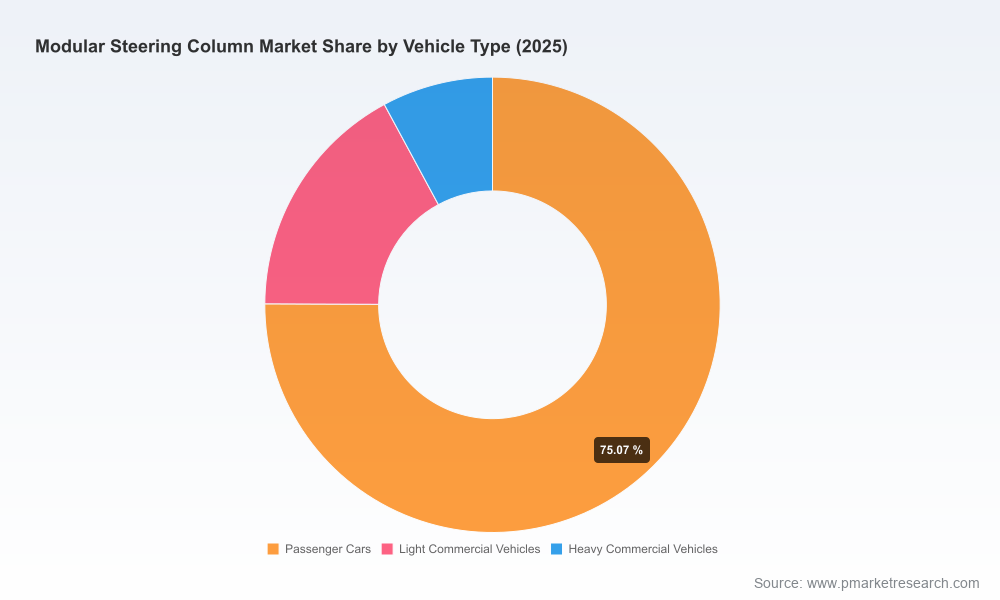

As automotive platforms evolve around electrification, ADAS integration and occupant safety, the modular steering column has emerged as a pivotal system-level enabler — linking ergonomics, crashworthiness, electronic functionality and vehicle architecture flexibility. PW Consulting’s latest Modular Steering Column Market study projects the market to expand at a 5.96% CAGR over the 2026–2032 forecast window. In practical terms, the global market progresses from an estimated USD 2,646.2 million in the 2025 base year to approximately USD 3,969.5 million by 2032. This growth trajectory underscores a steadily increasing commercial imperative for OEMs and tier suppliers to reassess platform strategies, supplier partnerships and material choices as they plan 2026 product and sourcing cycles.

Modular Steering Column Market

Synchronizing platform and supply strategies: Modular steering columns are no longer a discrete mechanical commodity; they are integration hubs for safety systems, electronic controls and driver convenience features. Procurement cycles initiated in 2026 will determine architecture choices that persist through the next generation of vehicle programs. Delaying a strategic decision risks committing to sub-optimal architecture or higher integration costs mid-program.

Modular Steering Column Market

Balancing safety compliance with cost and weight targets: Regulatory and functional-safety frameworks (notably FMVSS-related crash-energy management mandates and ISO 26262 requirements for electronic control modules) are tightening integration complexity. Suppliers that can demonstrate validated energy-absorbing mechanisms together with compliant control modules will command strategic value in OEM shortlists.

Modular Steering Column Market

Capturing margin through modularity and variant consolidation: The market’s structural dynamics favor suppliers that can offer modular platforms which reduce total variant count and simplify wiring and assembly. Executives must weigh the up-front systems cost against lifecycle savings in assembly, validation and aftersales.

Our analysis identifies four convergent forces that will shape procurement and R&D decision-making in 2026:

Integration of electronic functionality: Electrically adjustable columns, integrated locking and sensor suites are moving from optional extras to baseline elements for many mid- and upper-segment vehicles. This raises the bar for functional safety and brings software/firmware capability requirements into the sourcing equation.

Lightweighting pressure: Material substitution (in particular greater use of magnesium and aluminum alloys) is delivering tangible mass reductions at the component level. Industry literature notes a roughly 1:3 weight substitution ratio for magnesium versus ferrous metals — a factor that matters when programs are balancing fuel/energy efficiency targets and component-level cost.

Crash-energy management and occupant safety: Regulatory expectations for controlled compression and limited rearward displacement in frontal impacts create technical challenges that span mechanical collapse behavior and electronic detection. Suppliers that can harmonize both domains provide a differentiated value proposition.

Consolidation and concentration: Market concentration metrics indicate a meaningful presence of large, capable tier suppliers. The three-largest suppliers hold a significant share of market revenues, with a broader top-five accounting for a sizeable majority — an important consideration for OEMs seeking scale, global validation footprints and integrated engineering services.

Our competitive review of incumbent and leading suppliers focuses on four selection criteria that will be decisive in 2026 sourcing decisions: system modularity and variant management, global industrial footprint and program support, validated crash and functional-safety performance, and the ability to integrate electronics/software into a maintenance-minimized architecture.

Nexteer Automotive (Auburn Hills, MI) — offers broad portfolios spanning modular steering columns, intermediate shafts and scalable EPS suites. Recent product activity includes the launch and trade-show unveiling of a High-Output Column-Assist Electric Power Steering (HO CEPS) solution in April 2025, reinforcing its strategy of platform scalability and electrified assistance integration.

thyssenkrupp AG (Essen, Germany) — markets individual and modular columns with adaptive crash behavior, emphasizing differentiated load management depending on occupant restraint state; a strong contender for applications where nuanced crash performance is a program requirement.

Kongsberg Automotive (Kongsberg, Norway) — specializes in tailored tilt-and-telescopic products from modular systems, with in-house capabilities across design, development and validation — an asset for commercial and off-highway platforms where bespoke packaging is common.

Merit Automotive (Spain) — brings modular electronics and wiring simplification to steering column modules, enabling OEMs to reduce variant complexity and harness consolidated security/convenience features across vehicle ranges.

NSK, Robert Bosch, ZF (TRW), JTEKT, Hyundai Mobis and Mando — these established players combine global scale, regional program support and evolving material/weight strategies. Their portfolios range from lightweight, maintenance-free columns to electronically integrated control modules suitable for buses, trucks and high-volume passenger vehicles.

Material choices, process capabilities and component-level validation timelines will be core negotiation levers in 2026. Key pragmatic points for procurement and engineering leaders:

Sourcing strategy for lightweight alloys: Transitioning to magnesium or aluminum alloys yields component mass reductions, but also requires early-stage supplier qualification for casting, machining and corrosion-management processes. Plan for extended validation cycles if switching alloy families.

Integration of electronic modules and functional-safety alignment: ISO 26262 compliance is non-negotiable for electronic steering controls. OEMs should demand documented safety cases and up-to-date toolchains from suppliers during RFPs.

Variant reduction as a cost lever: Suppliers that can demonstrate a reduction in harness complexity and assembly steps through modularization often unlock downstream savings that outweigh incremental component costs.

Validation and crash testing capacity: Ensure your preferred suppliers have adequate global validation facilities and documented crash performance records aligned with relevant standards such as FMVSS energy-absorption requirements.

This study was designed to be a decision-ready toolkit for 2026 program planning cycles. Highlights include:

A transparent market-sizing and forecast model (base year 2025) projecting to 2032, with scenario workflows to stress-test planning assumptions against alternative growth paths.

A supplier capability map and qualification checklist tailored for OEM program managers, enabling rapid down-selection on the basis of modularity, electronics integration and validation footprint.

A risk register and mitigation playbook covering regulatory shifts, raw-material volatility and test-capacity bottlenecks, with recommended contractual language to align supplier commitments to program milestones.

Engineering-to-procurement handoffs including a practical migration plan for alloy substitution and wiring consolidation that estimates likely validation lead times and breakpoints for cost recovery.

Competitive intelligence dossiers on the leading OEM suppliers, including product rollouts, trade-show activity and emergent integration trends — structured so commercial teams can extract negotiation levers quickly.

Initiate platform-level steering column strategy reviews now: Lock in architecture choices early in 2026 to capture modularity-driven cost and integration benefits across vehicle programs.

Prioritize suppliers offering validated electronic module stacks and documented ISO 26262 safety cases — these lower program execution risk and speed time-to-market.

Treat material transitions as program-level decisions: If weight reduction is a target, pair alloy substitution decisions with supplier commitments on process capability, corrosion protection and crash-validated performance.

Use concentrated supplier footprints to your advantage: The market’s top suppliers control a meaningful share of revenues. Leverage their scale for global program support but maintain competitive tension through dual-sourcing strategies where feasible.

For executives and program leads, 2026 is a pivotal scheduling year: decisions made now about architecture, partner selection and material strategy will reverberate through vehicle programs that remain in production well into the next decade. Our analysis shows a market expanding consistently from a mid‑2020s base at a near‑6% CAGR to a materially larger industry by 2032 — a dynamic that rewards early strategic clarity and disciplined supplier qualification.

PW Consulting’s Modular Steering Column Market report provides the granular scenario analyses, supplier due‑diligence templates and executable migration plans needed to convert this macro outlook into concrete competitive advantage. For access to the full dataset, regional breakdowns, proprietary segmentation tables and the detailed supplier dossiers that inform these conclusions, please visit our report page.

For detailed analysis of this topic, please visit the official page:Modular Steering Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com