Hazardous Chemical Warehousing and Logistics: Strategic Imperatives for 2026 — PW Consulting Market Brief

As companies prepare capital allocation, network redesign, and compliance roadmaps for 2026, PW Consulting’s new Hazardous Chemical Warehousing and Logistics Market report delivers a targeted intelligence brief that turns market noise into executable strategy. This release distills why the sector matters, how value pools are shifting, and where operators, shippers, and investors should concentrate effort — while preserving the proprietary segment-level analysis that powers decisive action. This article highlights the report’s strategic value and practical utility without disclosing the complete segmented data, intentionally directing executives to the full report for the detailed inputs necessary to execute change.

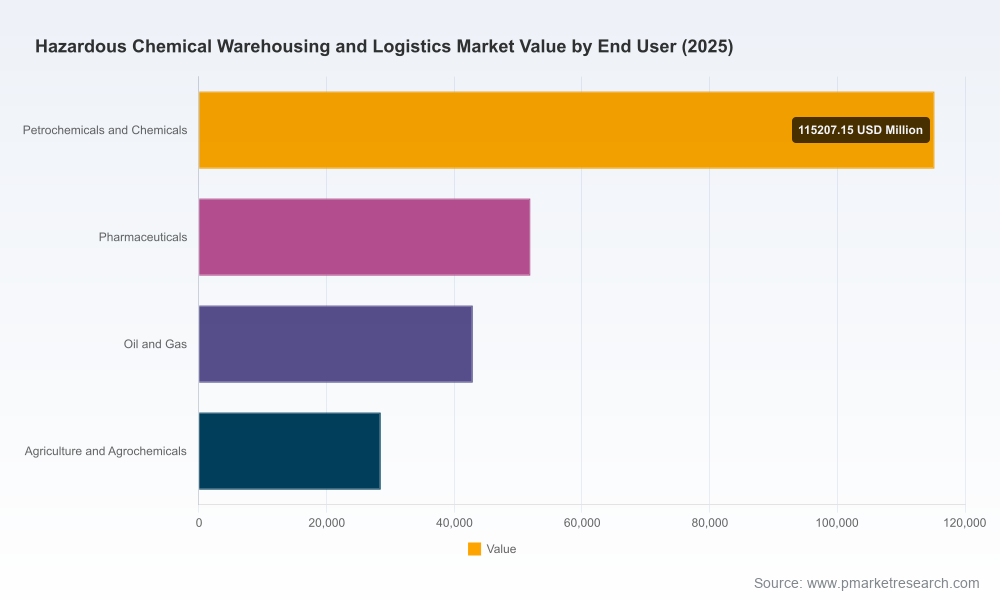

Hazardous Chemical Warehousing And Logistics Market

Executive snapshot

The hazardous chemical warehousing and logistics market is on a sustained expansion path. From our base-year analysis (2025), the global market is sizable and estimated to continue growing at a steady compound annual growth rate (CAGR) of 6.12% over the 2026–2032 forecast window. PW Consulting’s modeled trajectory anticipates material upside through 2032 as companies adapt to new regulation, modal shifts, and demand rebalancing across industrial value chains.

Hazardous Chemical Warehousing And Logistics Market

Why this matters for 2026 decision-making

- CapEx and network design hinge on credible forecasts. Many capital projects initiated in 2026 will have multi-year payback profiles in hazardous logistics — from ADR-compliant tank farms to automated hazmat-enabled warehouses. Our forecast scenarios and sensitivity testing enable CFOs and supply chain VPs to stress-test returns under alternative regulatory and logistics-cost regimes.

- Regulatory timing requires pre-emptive operational changes. A series of regulatory updates effective from 2026 (including the IATA 67th edition, IMDG amendments, and ADR 2025 harmonization efforts) change how dangerous goods are classified, documented and transported internationally. Companies that plan for compliance early reduce downtime, mitigate recall and recall-like events, and capture first-mover advantages in sustainable hazmat transport.

- Fragmentation creates both risk and acquisition opportunity. The market exhibits low top-tier concentration (CR3 and CR5 metrics indicate a fragmented competitive landscape), meaning regional specialists, niche service providers, and asset-heavy operators all hold valuable capabilities. For strategic acquirers, this fragmentation presents a clear runway for roll-up strategies and bolt-on capabilities that improve route density and compliance coverage.

Market sizing — the macro view (what we disclose)

PW Consulting’s market sizing anchors decision-making with an audited base year (2025) and a full forecasting methodology for 2026–2032. The 2025 global market size provides the foundation for our scenario planning, and under the central case the market expands at 6.12% CAGR across the forecast. By 2032, our central scenario projects the market to have materially increased from the 2025 baseline, reflecting a combination of structural demand growth, compliance-driven service expansion, and higher value-added revenue per ton for hazardous handling and storage.

Hazardous Chemical Warehousing And Logistics Market

Regulatory and operational dynamics reshaping the sector

- Regulatory tightening and harmonization. The IATA Dangerous Goods Regulations (67th edition), the IMDG Code Amendment that came into force in 2026, and the full operability of ADR 2025 collectively raise the bar for cross-border hazardous logistics. In parallel, North American rulemaking proposals seek closer alignment with international standards. These changes increase compliance costs in the short term but create durable barriers to entry for noncompliant operators.

- Workplace safety and labelling updates. OSHA updates effective in 2026 expand requirements for workplace labelling and employee training, elevating the importance of integrated training platforms and certification-managed third-party warehouses.

- Modal shifts and asset innovation. Recent service launches and asset deployments — from ADR-certified hydrogen trucks to ISO tank rail corridors and purpose-built liquid chemical vessels — indicate that logistics providers are selectively investing in low-emissions and high-compliance modes. These investments alter modal cost curves and open new route architectures for bulk and packaged hazardous flows.

- Technology for visibility and risk control. Real-time tracking, advanced telematics, and cloud-based documentation platforms are becoming table stakes. Providers introducing provenance and safety-monitoring capabilities are commanding premium contracting terms with chemical producers and distributors.

Competition and capability map — what leaders are doing

The competitive landscape combines global integrated logistics providers, chemical-specialist networks, and regional niche operators. Leading global players are extending multimodal service portfolios, investing in dedicated hazmat facilities, and emphasizing compliance certifications as a commercial differentiator. At the same time, specialized operators with tank-container and intermodal expertise continue to play a pivotal role in cross-border liquid chemical flows.

- Integrated global networks. Major global providers are standardizing hazmat compliance and real-time visibility across wide networks, using scale to offer end-to-end chemical logistics solutions that integrate storage, packaging, and multimodal transport. Their playbooks prioritize standardized operating procedures, centralized compliance teams, and investments in certified assets.

- Specialist operators and intermodal players. Tank-container and bulk-liquid specialists maintain strategic relevance where route complexity and product specificity dominate. Their technical know-how in handling flammable and corrosive liquids commands higher margins on complex lanes.

- Regional emerging-market adapters. Providers with strong local regulatory relationships and multimodal capabilities are seizing growth as industrialization and chemical manufacturing expand in select growth corridors.

Recent corporate moves underscore these dynamics: acquisitions to broaden hazardous-handling footprints, technology launches to deliver real-time visibility, and certification-driven product introductions (for example, the first ADR-certified hydrogen truck in Europe and new ISO-tank rail services). These developments show providers are balancing compliance, decarbonization, and network density in their growth plans.

Strategic imperatives for 2026

- Prioritize compliance-first network investments. Capital budgets should allocate to compliance-critical assets and controls first: certified storage bays, segregated tank farms, and validated handling systems. Doing so prevents costly retrofits and protects contractual continuity with large chemical customers.

- Layer technology for visibility and auditability. Adopt real-time tracking and electronic document management that map directly to IATA/IMDG/ADR requirements. Visibility is not just a cost saver — it is a commercial differentiator that reduces insurance friction and speeds claims resolution.

- Design for modular flexibility. Given regulatory and product volatility, modular warehousing and adaptable tank capacity provide operational resilience. Use short-cycle lease strategies and modular tank leasing where possible to manage demand fluctuations.

- Pursue targeted M&A and partnerships. With low concentration at the top of the market, roll-ups and strategic partnerships remain the most immediate path to building comprehensive regional-to-global networks. Prioritize targets with proven hazmat certifications and local regulatory expertise.

- Embed sustainability into hazardous handling. Investment in low-emissions transport (e.g., hydrogen-capable vehicles, modal shifts to rail/sea), waste reduction in packaging, and energy-efficient storage offers long-term cost and reputational benefits — and increasingly, contractual prerequisites with multinational chemical buyers.

What the PW Consulting report delivers — practical contents for action

We designed the report as a playbook for 2026 executives. Highlights include:

- Robust market sizing and scenario models (base year 2025; full forecast 2026–2032) calibrated to policy, fuel, and modal-availability shocks.

- Regulatory impact matrices that translate IATA/IMDG/ADR/OSHA/PHMSA developments into operational change-tasks and estimated implementation timelines.

- Capability benchmarking and vendor scorecards for hazmat warehousing, tank services, and multimodal providers — enabling due diligence and supplier-selection decisions.

- Network-design templates and total-cost-of-ownership (TCO) calculators that let users compare capex vs. opex trade-offs for building vs. outsourcing hazardous storage and handling assets.

- Risk and compliance playbooks, including incident-response frameworks, third-party audit checklists, and staff certification roadmaps.

- Acquisition screening criteria for roll-up strategies, integrating route density analytics, certification portfolios, and customer-concentration metrics.

The report intentionally omits raw proprietary segment tables from this public summary. Our clients receive those segment-level breakouts (by service, end-use, and region), plus transaction comps and primary-source interview transcripts, enabling immediate execution of M&A, network redesign, and compliance programs.

How executives should use this intelligence in 2026

- Use the macro forecast and scenario outputs to set realistic revenue and capacity targets for the next capital planning cycle.

- Map regulatory timelines to procurement and training programs so that new requirements become part of hiring and vendor contracts rather than after-the-fact costs.

- Prioritize partnerships and bolt-on assets in markets where you lack hazardous-capable coverage instead of building from scratch; the market’s fragmentation makes strategic partnerships high-return options.

- Embed sustainability KPIs into tender scoring to capture future-proof customers and reduce long-term insurance and fuel exposure.

Conclusion — an actionable intelligence pathway

The hazardous chemical warehousing and logistics sector is transitioning from a compliance-only market to one where network design, technology, and sustainability create durable competitive advantage. PW Consulting’s market analysis quantifies the opportunity in the aggregate and supplies the operational tools executives need to convert forecasted growth and regulatory shifts into measurable performance. For decision-makers preparing 2026 strategies — whether investing in assets, evaluating acquisitions, or renegotiating supplier arrangements — the right intelligence shortens execution cycles and reduces implementation risk.

Access the full report

To obtain the full Hazardous Chemical Warehousing and Logistics Market report, including the detailed segmented revenue tables, regional and end-user breakouts, vendor scorecards, and downloadable modeling tools, please visit the PW Consulting research page. The full report provides the granular inputs and templates that make the difference between a theoretical plan and an executable program for 2026.

For detailed analysis of this topic, please visit the official page:Hazardous Chemical Warehousing And Logistics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com