Desktop Cloud Terminal Market Outlook 2026: Strategic Imperatives for Enterprise Decision‑Makers

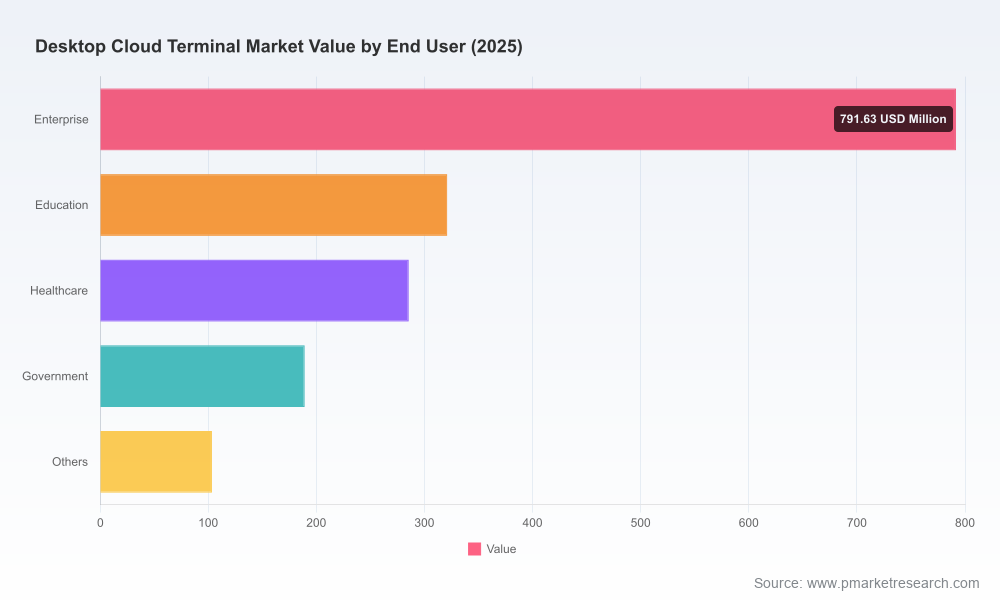

PW Consulting’s latest Desktop Cloud Terminal Market report (base year 2025, forecast period 2026–2032) reframes how CIOs, procurement leaders and corporate strategists should evaluate end‑user computing investments heading into 2026. The market reached approximately USD 1,690.75 Million in 2025 and is projected to grow at a compound annual growth rate of 4.98% through the forecast window, reaching the mid‑two‑billion USD range by 2032. This briefing highlights the report’s practical value for enterprise decision‑making while purposefully withholding the full, granular segmentation tables that are available in the complete study.

Desktop Cloud Terminal Market

Why 2026 Is a Pivot Point

Three converging forces make the coming 12–24 months critical for desktop cloud terminal strategy:

Desktop Cloud Terminal Market

- Technology convergence: DaaS, VDI and cloud‑native desktop services (Windows 365, Azure Virtual Desktop, and comparable offerings) have matured into enterprise‑grade options. Hardware vendors now ship thin, zero and ARM‑based endpoints tuned for these platforms.

- Regulatory and geopolitical pressures: Recent governance and national security measures—such as EU data sovereignty mandates and tightened export controls—are reshaping procurement, deployment geography, and supplier selection criteria.

- Operational economics and sustainability: Data center energy costs rose meaningfully amid AI workload growth, altering the calculus of total cost of ownership (TCO) for cloud‑delivered desktops and the value of energy‑efficient endpoints.

Taken together, these forces push enterprises to adopt a more disciplined, scenario‑based procurement approach. The market’s steady growth (CAGR ~4.98%) masks important inflection points—particularly around energy, compliance and supplier concentration—that will determine which technology and commercial models pay off.

Desktop Cloud Terminal Market

What the Report Delivers — Practical, Executable Content

PW Consulting’s report is structured to support operational decisions, not just market orientation. Key deliverables that CIOs and procurement leads will find immediately actionable include:

- Proven TCO and ROI models tailored to cloud terminal deployments, with sensitivity analyses for energy price shocks and DaaS cost paths.

- A vendor evaluation framework that scores partners across protocol support, firmware lifecycle policies, hardware refresh economics, and cloud management maturity.

- Migration playbooks for 30/90/180 day pilots—covering discovery, pilot design, user segmentation, and success metrics—and an RFP template aligned to compliance needs.

- Security and zero‑trust checklists mapped to CISA’s Zero Trust Maturity Model and practical hardening steps for cloud endpoints.

- Scenario planning modules that model the impact of regulatory constraints (data residency, export controls) and supply chain disruption on deployment timelines.

- Executive one‑pagers and board‑ready risk/benefit slides that translate technical tradeoffs into financial and strategic outcomes.

These tools are grounded in a transparent methodology (historical analysis 2020–2025; forecast 2026–2032) and are designed for direct adoption by IT program teams and procurement committees.

Competitive Landscape — Who to Watch and What It Means

The industry remains led by established OEMs and specialist endpoint vendors. PW Consulting’s competitive analysis synthesizes product roadmaps, protocol support and go‑to‑market moves. Key providers examined in the report:

- Dell Technologies (Round Rock, Texas, USA — https://www.dell.com) — Offers Wyse thin clients optimized for cloud desktop virtualization with broad compatibility across Citrix, VMware Horizon and Microsoft Azure Virtual Desktop. Recent product launches emphasize multi‑monitor support and deeper Windows 365 integration.

- HP Inc. (Palo Alto, California, USA — https://www.hp.com) — Continues to refresh its thin client portfolio (t‑series and mt‑series) for zero‑client and VDI access. Certification and compatibility work with major desktop virtualization platforms reduces integration risk for large deployments.

- Lenovo Group (Beijing, China / Morrisville, North Carolina, USA — https://www.lenovo.com) — Combines endpoint hardware lineage with enterprise services through ThinkCentre and ThinkEdge thin clients, recently updating product families with higher‑performance processors aimed at more demanding virtual workloads.

- IGEL Technology (Reading, UK — https://www.igel.com) — Differentiates on software‑centric endpoints with IGEL OS and a management layer built for secure, policy‑driven cloud access. The vendor’s OS updates continue to add native protocol support and zero‑trust features.

- 10ZiG Technology (Bristol, UK — https://www.10zig.com) — Focuses on zero clients and thin clients with attention to protocol diversity (PCoIP, Blast, RDP), offering cost‑effective options for large seat counts.

- Huawei Technologies (Shenzhen, China — https://www.huawei.com) — Supplies cloud desktop terminals aligned with operator and enterprise VDI environments; regional buyers must weigh performance and integration strengths against geopolitical and supply considerations.

- Acer (New Taipei City, Taiwan — https://www.acer.com) — Positions Veriton N series thin clients for mainstream VDI and DaaS use cases, emphasizing affordability and straightforward manageability.

Recent vendor activity in 2025–2026 (product launches, certifications, OS releases and processor refreshes) shows competition shifting toward platform compatibility, security posture and lifecycle economics rather than raw device specs alone. For buyers, this means prioritizing vendors with demonstrable firmware update policies, long‑term management platforms and multi‑protocol support.

Strategic Implications — A Playbook for 2026

Enterprises should treat desktop cloud terminals as an integrated program—hardware, management software, cloud provider choice and security posture—rather than a line‑item purchase. PW Consulting’s report recommends a six‑step decision playbook:

- Inventory and segment: Classify users by risk, performance needs and location to identify clear pilot cohorts.

- Model TCO under stress: Run sensitivity scenarios for energy inflation and DaaS pricing to reveal hidden ops costs.

- Design interoperable pilots: Test at least two vendors and two protocols in production‑adjacent environments before enterprise roll‑out.

- Embed zero‑trust: Apply endpoint certification, identity controls and telemetry requirements that align with CISA guidance and internal risk tolerances.

- Mitigate supply and compliance risk: Place long‑lead equipment on staggered contracts, and codify data residency constraints into procurement terms.

- Measure sustainability and user experience: Include energy consumption and end‑user QoE as procurement KPIs alongside price and warranty terms.

For procurement leaders, the immediate priorities are contract language that secures firmware updates and repair SLAs, and commercial terms that allow for flexible seat counts as hybrid work patterns settle. For IT leaders, the priority is operationalizing endpoint telemetry and integrating it with identity and device posture systems.

90/180/365‑Day Roadmap — How to Convert Insight into Execution

- Day 0–90: Rapid discovery and pilot design; select three pilot vendors and two cloud service models (VDI and DaaS). Deploy telemetry and run the TCO sensitivity model.

- Day 90–180: Execute pilots, validate security controls against zero‑trust maturity criteria and benchmark user experience across network variances.

- Day 180–365: Negotiate enterprise contracts with staged delivery, measurable SLAs for firmware updates and energy consumption reporting; implement phased roll‑out with continuous measurement against KPIs.

Executive Decision Checklist

- Do we have a segmented user map that justifies different endpoint classes (thin, zero, ARM)?

- Have we stress‑tested TCO for energy and DaaS pricing volatility?

- Are firmware lifecycle and update SLAs contractually mandated?

- Is endpoint telemetry integrated with our identity and SIEM platforms?

- Have we evaluated supply chain and geopolitical risk for critical components?

- Do our procurement terms enforce data residency and regulatory compliance where required?

- Are sustainability KPIs included in vendor scorecards?

Closing: The Strategic Value of the Full Report

PW Consulting’s Desktop Cloud Terminal Market report provides the evidence base, scenario tools and vendor scorecards necessary for defensible, procurement‑grade decisions in 2026. The analysis translates market growth—the clear mid‑single‑digit CAGR and projected expansion to the billions over the forecast period—into actionable playbooks and procurement templates that materially reduce rollout risk and lifecycle cost. To preserve the integrity of commercial negotiations and to support bespoke procurement scenarios, the report reserves full subsegment tables, regional breakouts and vendor scorecard matrices for the complete publication.

For executive teams preparing 2026 budgets and strategic roadmaps, the report serves as both a risk‑mitigation toolkit and a practical guide to capture the productivity and cost benefits of cloud‑delivered desktops while navigating the new realities of regulation, energy economics and supplier geopolitics. Access the full study and downloadable implementation assets via PW Consulting to move from strategy to execution with confidence.

For detailed analysis of this topic, please visit the official page:Desktop Cloud Terminal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com