Mussel Oil and Powder Market Growth Accelerates as Demand for Natural Health Supplements Surges

Other |

2026-06-16 11:06:19

As organizations prepare 2026 budgets and strategic roadmaps, PW Consulting today releases an executive-level preview of our forthcoming Cold Roof Coating Market research. Built on a base year of 2025 and a rigorous historical review (2020–2025), the study quantifies a market that has demonstrably moved from recovery into structurally higher demand. The global market reached USD 5,310.45 Million in 2025 and, under our baseline scenario, is projected to expand at a 7.15% CAGR to approximately USD 8,611.45 Million by 2032. This preview outlines the report’s strategic value for executive decision-making in 2026 while deliberately withholding granular segmentation figures to encourage access to the full model and datasets.

Cold Roof Coating Market

Capital allocation and portfolio prioritization: With persistent momentum in energy-efficiency retrofits and new-build sustainability requirements, firms must decide which product families, procurement channels, and geographies to prioritize in 2026. The market’s mid-single-digit-to-high-single-digit CAGR creates a runway for investment but requires disciplined portfolio choices to capture profitable share.

Cold Roof Coating Market

Regulatory and standards-driven demand: Recent updates to testing and rating frameworks have raised the bar on liquid-applied coatings and polymer/composite materials. These changes will reshape product eligibility for incentive programs and municipal code compliance from 2026 onward, affecting product certification strategies and go-to-market timing.

Cold Roof Coating Market

Margin and supply-chain pressure: Volatility in petrochemical feedstocks, pigment costs (notably titanium dioxide), and specialty additives means manufacturers and buyers alike must embed commodity scenarios into pricing, hedging, and sourcing decisions for 2026.

Integrated market model (2020–2032): A flexible, downloadable model that lets executives stress-test demand under alternative macro-, regulatory-, and raw material scenarios. The model can be filtered by product family, end-application, and region (full segmentation available in the paid report).

Risk-adjusted investment playbooks: Actionable frameworks for capex, R&D, and M&A decisions, including required returns and sensitivity thresholds tied to raw material swings and certification timelines.

Channel and commercial playbooks: Go-to-market blueprints for OEMs, formulators, distributors, and applicators—covering pricing architecture, specification strategies for architects and facility managers, and warranty-anchored commercial offerings.

Regulatory and standards tracker: A concise, time-lined digest of standards changes, testing updates, and certification pathways that influence product qualification and municipal incentive eligibility.

Supplier benchmarking and capability map: A pragmatic assessment of incumbent and emerging suppliers across formulation capability, testing and certification readiness, manufacturing footprint, and service/warranty execution.

Investment heatmaps and exit scenarios: Priority sub-segments and technology vectors for investment, plus modeled exit multiples under different consolidation scenarios.

Standards evolution accelerates commercial adoption. The ANSI/CRRC S100-2025 update introduced revised protocols for liquid-applied systems and new polymer/composite testing provisions; the Cool Roof Rating Council’s parallel steps to accredit international labs increase global comparability of product ratings. These shifts compress the time-to-specification for projects that rely on certified performance, creating both opportunities for fast-to-certify players and barriers to entry for slower movers.

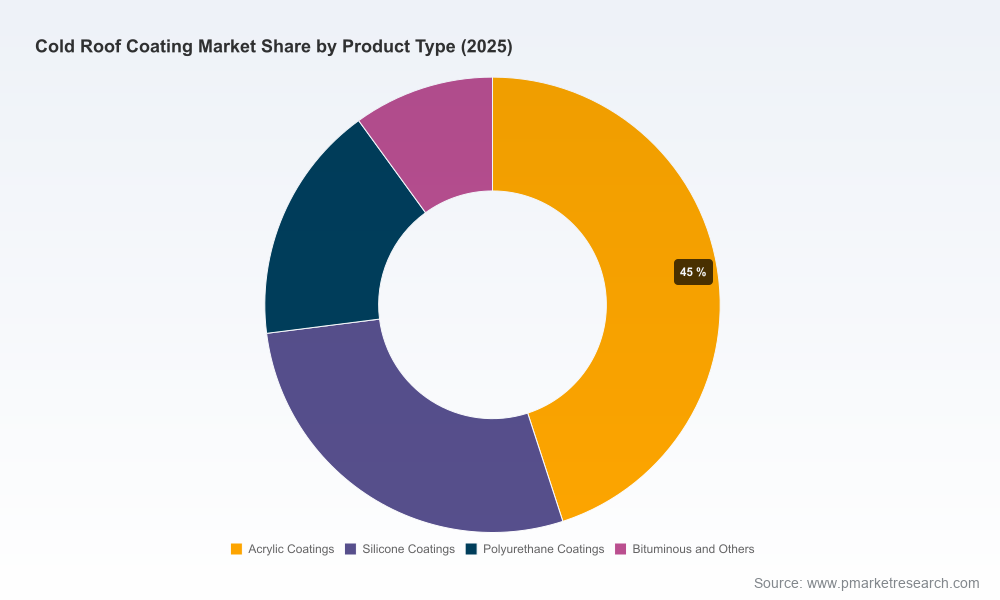

Raw-material cost volatility is no longer an operational footnote. Petrochemical-derived resins and critical pigments continue to show price swings that materially affect cost of goods sold. Separately, silicone formulations typically command a meaningful premium over acrylic alternatives due to superior durability — our sector analysis finds that silicone premiums can range substantially and should be a central input in pricing strategy and product lifecycle economics.

Warranty and service are differentiators. The introduction of long-term warranty programs and installer certification schemes (e.g., a recent 25-year warranty program announced in early 2026) is reframing buyer expectations. Companies that can reliably back performance with installer networks and validated lifecycle economics will outcompete in commercial and large-scale restoration segments.

Innovation and sustainable formulations are increasingly table stakes. New product launches that combine low-VOC profiles, fiber reinforcement for low-sag applications, and demonstrable compliance with regional building codes are commanding specification preference in many institutional buyers.

The market remains moderately consolidated: the top three suppliers collectively hold a meaningful but not dominant share, and the top five increase concentration further—an environment that supports targeted M&A and strategic partnerships. Leading corporates and specialized manufacturers play different strategic games:

Sherwin-Williams and PPG Industries leverage scale and channel reach to embed high-performance, infrared-reflective systems into global architectural and industrial pipelines. Their advantages lie in distribution, specification influence, and R&D scale—key factors for firms aiming to defend or expand share in 2026.

AkzoNobel, BASF, Dow, and Sika compete on formulation depth and systems capability—elastomeric and polymer-engineered solutions that balance durability with reflectivity. Their industrial-grade product sets are attractive for large facility owners and infrastructure projects where lifecycle cost matters most.

RPM (Tremco), Henry (Carlisle), and GAF are powerful in roof system integration and installer networks; these firms can extract premium pricing through warranty-led offers and bundled restoration services—an increasingly important route-to-market for 2026 commercial projects.

Smaller, nimble specialists like NanoTech Materials, Castagra, Gardener-Gibson, Karnak, Western Colloid, and Neogard (Hempel) are deploying product innovation (ceramic insulative technology, fiber-reinforced coatings, VOC-free formulations) and rapid certification strategies to secure niche positions. Their agility makes them attractive targets for partnerships or acquisition to accelerate product diversification.

Standard-setting progress: The CRRC’s 2025 standard updates and its approval of an internationally accredited testing laboratory materially reduce the certification friction for manufacturers targeting multiple markets. This accelerates cross-border product rollouts and increases the value of early certification investment.

Product and commercial innovation: New product launches that meet stricter regional codes and low-VOC expectations are raising the specification bar. Additionally, extended warranty programs backed by installer certification are shifting the competitive battlefield from price-only to total-cost-of-ownership and service reliability.

Embed standards and certification into product roadmaps. Make CRRC and equivalent test beds a gating item for new launches. The time and cost of certification should be part of NPV calculations and product launch timelines.

Pursue margin-resilient portfolios. Given raw-material volatility, structure product lines with clear margin differentiation—premium, warranty-backed systems (e.g., silicone-based) versus value acrylic platforms—and price them accordingly.

Invest selectively in installer ecosystems and warranty programs. Long-tenor warranties with certified applicators reduce lifecycle risk and command specification preference in commercial tenders.

Operationalize supply resilience. Hedge critical feedstocks where economics support it, qualify alternate resin suppliers, and evaluate near-shoring for high-value formulations to reduce lead-time risk.

Target M&A and partnerships to fill capability gaps. For incumbents seeking faster entry into high-growth niches (e.g., ceramic-insulative or fiber-reinforced systems), acquiring nimble innovators or forming exclusive licensing deals accelerates time-to-market with lower execution risk.

Our complete Cold Roof Coating Market report provides the granular data, scenario models, and supplier scorecards that procurement, product, and corporate development teams require to make defensible 2026 decisions. Subscribers gain access to the full segmentation matrix, downloadable demand and revenue models, and implementation playbooks—assets designed to shorten decision cycles and reduce execution risk.

This preview surfaces the strategic contours and near-term catalysts that will shape the competitive landscape in 2026. For executives preparing budgets, designing product roadmaps, or evaluating M&A targets, the full PW Consulting report is the operational intelligence platform that converts market visibility into prioritized action. Access to the complete datasets, scenario tools, and supplier-specific assessments is available through our report portal.

To discuss how these insights apply to your 2026 business plan, request a briefing with PW Consulting’s Cold Roof Coating practice—where we translate market dynamics into executable strategy.

For detailed analysis of this topic, please visit the official page:Cold Roof Coating Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com