Sensing the Cabin – Growth Dynamics in the In-Vehicle Occupancy Detection Radar Sensor Market

Other |

2026-05-20 09:47:58

PW Consulting’s new Polyelectrolyte Market report (base year 2025; historical window 2020–2025; forecast 2026–2032) translates complex industry dynamics into actionable intelligence for leadership teams planning through 2026 and beyond. Our bottom-up market model projects the global polyelectrolyte market to grow from an estimated USD 3,450 million in 2025 to approximately USD 4,952 million by 2032, reflecting a compound annual growth rate (CAGR) of 5.31% over the forecast period. This trajectory is neither uniform nor inevitable — it is driven by intertwined demand trends, raw-material cost volatility, regulatory pressure, and a competitive landscape that mixes global scale players with high-capacity regional producers.

Polyelectrolyte Market

Budgeting and procurement: A mid-single-digit CAGR and the observed price dynamics in 2025 require procurement strategies that balance spot buying, index-linked contracting and strategic inventories to shield margins from input swings.

Polyelectrolyte Market

R&D and product positioning: Regulatory tightening and faster adoption of high-performance chemistries are favoring differentiated polyelectrolyte grades — companies that can demonstrate lower dose, higher efficiency, or improved environmental profiles will capture premium demand.

Polyelectrolyte Market

Capacity and CAPEX choices: Forecasted growth supports targeted capacity investments, but siting, feedstock security and energy profile must be evaluated to avoid margin erosion from raw material or logistics shocks.

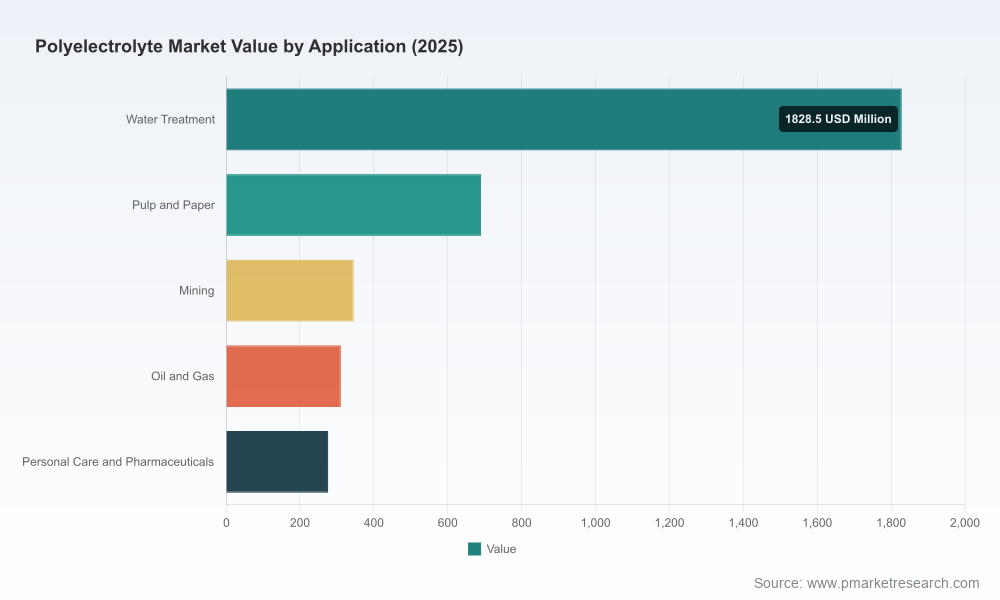

The market’s expansion from the mid‑2020s toward 2032 is steady rather than exponential. Our model synthesizes historical consumption patterns (2020–2025), plant-level capacity data, and end‑market demand — particularly from water treatment, pulp & paper, mining, and industrial process chemistry — to arrive at the 5.31% CAGR. This stability creates room for disciplined growth strategies: selective greenfield projects in underserved corridors, bolt‑on M&A to shore up specialty portfolios, and differentiated pricing mechanisms in mature geographies.

Regulation and environmental enforcement: Stricter wastewater discharge standards and an elevated corporate focus on water stewardship are accelerating the adoption of higher‑performance polyelectrolytes in municipal and industrial treatment plants. This is one of the most durable demand-side drivers entering 2026.

Feedstock exposure: Polyelectrolyte supply chains remain exposed to upstream monomer dynamics. Acrylamide production is linked to acrylonitrile feedstock, which in turn is sensitive to crude oil and petrochemical cycle swings. This linkage implies that crude price volatility and regional feedstock constraints can transmit rapidly to producer margins and pricing.

Regional price signals in 2025: Pricing trends through 2025 already reflect these pressures and demand conditions. China saw a modest annual decline in a widely traded polyacrylamide grade (~3% year‑over‑year in 2025) driven by weak demand and capacity expansion, while Northeast Asian and European posted different price levels reflecting local supply–demand and energy cost structures. These regional differentials will influence sourcing and transfer‑pricing strategies in 2026.

The polyelectrolyte industry combines multinational integrated chemical houses, focused specialty players, and high‑capacity regional manufacturers. Market concentration is moderate: the top three players account for roughly one‑third of global market volumes while the top five approach the mid‑40s in percentage terms. That structure creates both competitive pressure and transactional opportunity.

SNF Floerger (Andrézieux, France) — A global leader in polyacrylamide‑based polyelectrolytes with extensive high‑volume manufacturing and a strong position in water and wastewater flocculation. SNF’s scale gives it cost and logistical advantages for large municipal and industrial contracts.

BASF SE (Ludwigshafen, Germany) — Deploys well‑known product lines tailored to water treatment and paper process chemistry. BASF’s strength lies in formulation breadth and upstream integration into specialty chemistries.

Kemira Oyj (Helsinki, Finland) — Deeply embedded in pulp & paper and municipal water treatment markets, with a suite of cationic and anionic products and strong process‑optimization services.

Solenis LLC (Wilmington, Delaware, USA) — Focuses on water‑soluble polyelectrolytes across paper chemicals and industrial applications; competitive on service models and localized supply.

Ecolab Inc. (Nalco Water) (St. Paul, Minnesota, USA) — Combines polyelectrolyte chemistries with digital water‑management services and operational contracts, which can deepen customer stickiness beyond product pricing.

Dow Chemical Company (Midland, Michigan, USA) — Offers polyelectrolyte solutions as part of its broader industrial chemicals portfolio; benefits from large‑scale raw material integration and global logistics.

Thermax Limited (Pune, India), Arkema (Colombes, France) and a cohort of high‑capacity regional producers in China and India (including firms with large annual capacities) — These players provide critical scale in regional markets and compete on cost, service response and formulation adaptation.

Strategic implication: multinational buyers should reassess vendor rationalization with a twofold lens — price and capability. Suppliers with digital service offerings, local blending/packaging footprints, and demonstrated feedstock hedging strategies will be strategic partners rather than simple commoditized vendors.

Demand and supply model (2020–2032): A bottom‑up, SKU‑level model calibrated with primary interviews, plant data and trade flows to enable scenario testing under different feedstock and regulatory assumptions.

Price‑sensitivity and margin maps: Stress tests showing the impact of crude and acrylonitrile moves on producer margins, along with practical procurement hedging templates for 12–24 month cycles.

Competitive benchmarking: Profiles and capability matrices for leading global and regional players, including manufacturing footprint, technology strengths, and service models to support sourcing and M&A diligence.

Scenario playbooks: Three operational scenarios (status quo, accelerated regulation, and feedstock shock) with recommended tactical moves for sales, operations and procurement teams.

Investment and M&A framework: Target scoring criteria, integration checklists and valuation sensitivity analyses that align with the market’s consolidation dynamics.

Sustainability and regulatory impact assessment: Evaluation of emerging discharge standards and chemical safety regulations, and how these will recalibrate product specifications and customer purchasing criteria.

Adopt differentiated procurement: Combine longer‑dated indexed contracts for base volumes with flexible spot allocations to capture regional price dips and preserve working capital.

Prioritize specialty grades: Allocate R&D and commercial resources to high‑efficiency, low‑dose chemistries that command premium pricing under tighter environmental norms.

Review footprint versus feedstock exposure: Evaluate plant location decisions against feedstock access and energy cost profiles; nearshoring or contract manufacturing can reduce logistics and feedstock risk.

Build service differentiation: Bundle formulation optimization, dosing automation and outcome‑based performance contracts to lock in customers and reduce price elasticity.

Use consolidation selectively: Target bolt‑on acquisitions that provide specialty capabilities or fill strategic geographic gaps, and apply strict integration metrics to realize synergies.

The report’s conclusions are grounded in a mixed‑method research approach: primary interviews with supplier and end‑user executives, plant capacity surveys, trade flow analysis, and dynamic price modeling. We have triangulated public disclosures, proprietary pricing trackers and on‑the‑ground validation to ensure robust scenario planning. While we disclose top‑line market trajectory and structural metrics in this release, the report contains the granular segmentation, regional and application splits, vendor market shares and model workbooks required for transactional decision‑making.

For executives preparing 2026 budgets, the report functions as a strategic control panel: it highlights likely cost headwinds, identifies value pools for differentiated products, and prescribes procurement and M&A moves aligned with plausible macro scenarios. For procurement and operations leaders, the practical tools and stress tests reduce the risk of over‑investing in exposed capacity or under‑hedging raw material cost exposure. For corporate development teams, the competitive mapping and valuation sensitivity support disciplined pursuits that accelerate scale or capability without undue execution risk.

PW Consulting has prepared a concise executive deck and an interactive data workbook that accompany the full report. These materials allow teams to run custom scenarios tied to company‑specific volumes, feedstock contracts and regional exposure. To access the full dataset, segmentation tables and the scenario workbooks necessary for detailed 2026 planning, please visit PW Consulting’s Polyelectrolyte Market report page or contact our advisory team for a briefing.

For detailed analysis of this topic, please visit the official page:Polyelectrolyte Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com