Egg-Free Mayonnaise Market Forecast: Strong Growth Expected by 2034

Other |

2026-06-03 08:07:54

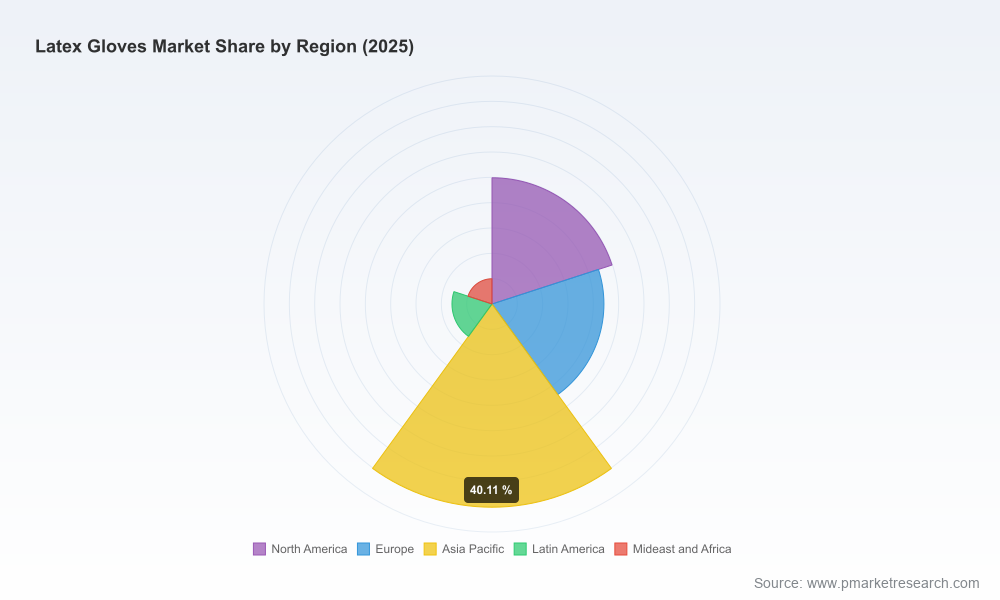

Our latest Latex Gloves Market report establishes a calibrated, decision-ready view of the market as of the 2025 base year and projects forward across a 2026–2032 forecast horizon. The global market stood at approximately USD 9.5 billion in 2025 and shows a steady mid-single-digit trajectory, with a compound annual growth rate (CAGR) of 4.2% embedded into our baseline forecast. The trajectory through 2032 reflects structural demand in medical and industrial channels, punctuated by episodic supply-side shocks and regulatory changes that will determine winners and laggards over the next three years.

Latex Gloves Market

Procurement and cost management — With natural rubber latex remaining a dominant cost input and exposed to seasonal and weather-driven price swings, procurement leaders must move beyond transactional buying. Our report identifies the contractual levers and hedging constructs that materially reduce realized cost volatility without sacrificing supply continuity.

Latex Gloves Market

Capacity planning and plant investment — Manufacturers deciding whether to expand, retrofit, or mothball lines need forward curves and utilization stress tests, not just headline growth rates. The 4.2% CAGR and our scenario overlays translate into concrete utilization thresholds that justify capital allocation or strategic idling in 2026.

Latex Gloves Market

Portfolio and product strategy — Shifts in end-user preferences (notably migration toward non-latex alternatives in certain healthcare and food service channels) mandate a differentiated product roadmap. The report maps where premium features (accelerator-free, sulfur-free latex, enhanced tactile sensitivity) preserve market share versus where substitution risk is highest.

Regulatory and ESG readiness — Pending and postponed regulatory actions (including the EU’s treatment of natural rubber under deforestation rules and continuing FDA device classifications) are not theoretical risks; they are timing and compliance events that can compress supply or raise entry costs. The report provides a regulatory calendar and compliance playbook for 2026 preparedness.

M&A and partner diligence — Investors and corporate development teams need a compact shortlist of targets based on capacity quality, geographic risk, and margin resilience. Our concentration analysis shows a moderately consolidated market where CR3 and CR5 dynamics create both partnership opportunities and competitive pressures.

We designed this report as an operational toolkit for 2026. Our analysis synthesizes market-sizing, supplier economics, standards compliance, and product innovation into tactical recommendations. Key takeaways include:

Margin exposure is concentrated in feedstock cost and accelerator sourcing. Manufacturers that invest now in alternative chemistries or long-term NR contracts realize a disproportionate improvement in gross-margin volatility.

Product differentiation — especially accelerator-free and sulfur-free formulations — is an immediate defensive and offensive lever. Recent innovation showcases from major manufacturers validate that investment in hypoallergenic formulations accelerates retention in regulated medical accounts.

Distribution and procurement contracts will shift to more flexible frameworks. Service-level agreements that include tiered pricing, capacity reserves, and shared risk clauses outperform fixed-price, short-term purchases under stressed supply scenarios.

Regulatory alignment and certification (ASTM/EN standards, FDA pathways) are non-negotiable for market access and pricing power. Early certification can create multi-quarter lead times as a barrier to entry for competitors.

Proprietary market model with annualized demand and supply balances through 2032, plus three alternate scenarios (downside shock, base, accelerated substitution).

Supplier heat map and supplier risk scoring — capacity quality, geographic exposure, ESG risks, and cost-to-serve metrics.

Raw material sensitivity matrix with suggested hedging and contract structures tailored to natural rubber latex volatility.

Regulatory tracker and compliance checklists for FDA, EU standards, and major Asian regulatory regimes, including timelines and recommended actions for 510(k) and EN certification pathways.

Go-to-market playbooks for manufacturers and distributors addressing pricing architecture, channel segmentation, and tender response templates.

M&A screen and integration checklist highlighting accretive bolt-ons, capacity consolidation candidates, and tech-driven differentiation targets.

Commercial negotiation scripts and procurement term-sheets that translate market projections into actionable contract clauses for 12–36 month horizons.

The industry structure remains moderately concentrated: the top three suppliers capture a meaningful share of market value while the top five wield a majority share of the market’s commercial gravity. That concentration creates a mix of competitive intensity and coordinated stability—an environment in which scale matters for raw material procurement, certification throughput, and distribution reach.

Top Glove Corporation Bhd (Malaysia): A volume leader with high running capacity and recent launches around accelerator-free and lightweight formulations. Their scale provides negotiating leverage on NR sourcing and enables rapid commercialization of innovations presented at industry forums.

Hartalega Holdings and Kossan Rubber Industries (Malaysia): Both emphasize premium medical-grade solutions and maintain technical depth in latex processing. Their product focus and quality positioning help defend healthcare accounts where EN/ASTM compliance and tactile performance are decision drivers.

Supermax and Sempermed: Players that combine regional manufacturing strengths with targeted product portfolios—effective at serving hospital systems and distribution partners that prioritize blended portfolios (latex and non-latex).

Ansell Limited: A global defender of premium protection solutions, leveraging R&D to deliver barrier performance and comfort. Its global reach and brand equity are substantial advantages in tender-heavy markets.

Cardinal Health and Medline Industries: As major distributors and OEM partners, they influence channel dynamics and can accelerate shifts toward private-label or branded product mixes depending on contract economics.

INTCO Medical (China): Recent product introductions into sulfur-free synthetic-latex formulations indicate an aggressive product diversification strategy; watch for their push into regulated export markets and compliance declarations that could close the gap with established players.

Regional manufacturers (India, Malaysia, Europe): Mid-sized producers remain important for specialized or local demand pockets; their agility in niche segments can create acquisition appeal for larger players seeking margin expansion.

Product innovation: Accelerator-free and sulfur-free latex formulations have moved from concept to commercial rollouts, reducing allergy exposure and creating premium positioning. Manufacturers introducing these products are capturing improved contract terms in hospital tenders.

Capacity signals: Leading manufacturers report very large installed capacities and are balancing utilization with cost pass-through strategies. That balancing act will determine short-term pricing dynamics as markets normalize.

Regulatory timing: The EU’s deferred enforcement timeline for certain natural rubber sourcing rules shifts compliance urgency into late 2026—creating a narrow window for suppliers to remediate supply chains and secure certified provenance.

Substitution risk: End-user migration to nitrile in specific segments persists; policy actions and allergy prevalence estimates continue to shape demand composition, increasing the value of dual-material capability.

Manufacturers: Prioritize dual-feedstock capacity, accelerate hypoallergenic latex lines, secure multi-year NR supply agreements with staged price-pass clauses, and invest in certification lead-times to preempt tender cycles.

Distributors: Reconfigure assortment strategies to combine premium allergy-safe latex with competitive nitrile SKUs, and negotiate portfolio-level SLAs rather than SKU-level terms to manage inventory and service costs.

Healthcare purchasers: Reassess total cost of ownership to include allergy-risk mitigation and supply resiliency; incorporate certification and traceability requirements into RFPs to align supplier incentives.

Investors and M&A teams: Look for targets that offer either technological differentiation (formulation IP, certification pipelines) or capacity that fills strategic geographic gaps; valuation arbitrage exists where market concentration enables consolidation synergies.

Our findings are grounded in primary interviews with manufacturing and procurement leaders, on-site plant assessments, customs and trade flows, company filings, and proprietary cost models that map raw-material inputs to finished-goods economics. We triangulate bottom-up production capacity with top-down demand modeling and stress-test results across three macro scenarios to surface decision thresholds rather than single-point forecasts.

This release is a concise orientation to the strategic choices ahead in 2026. It is intentionally selective: the full report contains the detailed segmentation, supplier scorecards, scenario spreadsheets, and contract templates that are necessary to execute the measures summarized here. For organizations making sourcing commitments, capital allocation decisions, or M&A moves in 2026, the full dataset and playbooks are essential.

Contact PW Consulting to access the complete Latex Gloves Market report, the underlying models, and a tailored briefing workshop to translate these insights into your 2026 operating plan and board materials.

For detailed analysis of this topic, please visit the official page:Latex Gloves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com