Global Glyceryl Mono Oleate Market to Hit USD 782.5 Million by 2032 at 7.9% CAGR

Other |

2026-06-05 09:21:20

As organizations enter a decisive planning window for 2026, the operations and maintenance (O&M) landscape for data centers is transitioning from tactical fire‑fighting toward strategic infrastructure stewardship. PW Consulting’s latest market study, “Data Center Operations and Maintenance Service Market — 2026–2032 Outlook,” synthesizes five years of historical performance and a prospective seven‑year forecast to give CIOs, facility heads, and procurement leaders the evidence base they need to make high‑impact choices this year.

Data Center Operations And Maintenance Service Market

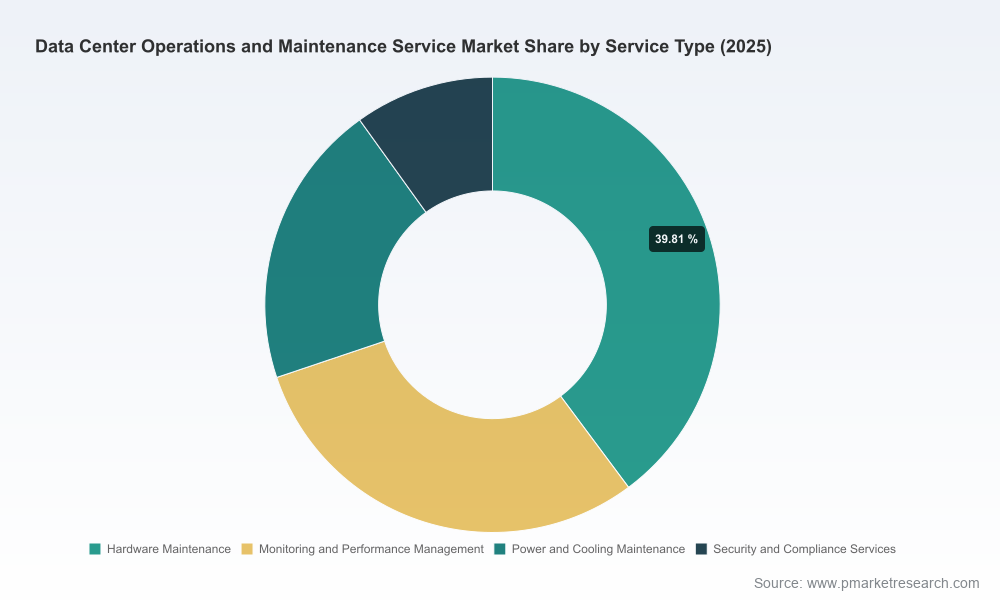

At the macro level, the global O&M services market has more than recovered from pandemic‑era volatility, growing from a mid‑teens billion‑dollar base in 2020 to an estimated market size of roughly USD 36.45 billion in the report’s base year (2025). Our model projects continued expansion through 2032 at a compound annual growth rate (CAGR) of approximately 11.7%, driven by hyperscale capacity growth, proliferating colocation footprints, and rising operational complexity tied to hybrid cloud architectures and edge deployments.

Data Center Operations And Maintenance Service Market

Timing: 2026 is the inflection point for multi‑year capacity contracts, cloud repatriation pilots, and large‑scale modernization programs. Decisions made this year will determine cost and resilience outcomes throughout the next decade.

Data Center Operations And Maintenance Service Market

Risk & compliance: New energy and operational standards — including the 2025 updates to ASHRAE guidance for data center energy performance — are changing asset lifecycle economics. The report translates those regulatory changes into operational thresholds and retrofit triggers.

Talent & delivery: Labor scarcity remains acute. Industry surveys show a majority of operators struggling to retain qualified O&M staff. Our analysis quantifies the labor exposure embedded in long‑term operations models and presents mitigation pathways (automation, third‑party specialists, and flexible staffing pools).

Vendor strategy: Market concentration is material but not monopolistic. The top tier of providers consolidates a meaningful share of global supply, while a broad field of specialists competes on niche capabilities — creating options for hybrid sourcing models that optimize cost, uptime, and sustainability.

Decision frameworks for 2026 procurement: A step‑by‑step methodology to determine when to insource, outsource, or co‑manage O&M services across locations and facility types, including templated evaluation criteria for RFPs and contract SLAs.

Workforce and skills playbook: Role‑based competency matrices, productivity benchmarks, and strategic hiring versus partnering scenarios calibrated to current labor market dynamics and McKinsey‑level estimates of labor intensity for large buildouts.

Energy and sustainability retrofit guide: Practical thresholds derived from ASHRAE energy standards and cost‑benefit breakpoints for retrofits (cooling upgrades, power distribution optimization, and liquid cooling adoption) aligned to common procurement cycles.

Digitalization and AIOps roadmaps: Prioritized use cases for remote monitoring, predictive maintenance, and automated orchestration — including expected O&M ROI and KPIs to track in the first 6–18 months after deployment.

Risk scenarios and resilience playbooks: Stress‑test matrices for supply chain disruption, staffing outages, and multi‑site failure modes, with contingency staffing plans and vendor escalation templates.

TCO and lifecycle models: Financial templates that reconcile CapEx, recurring O&M, and avoidance savings from uptime improvements — adaptable to hyperscale, colocation, enterprise, and edge footprints.

Our forecast shows sustained, above‑market IT growth translating into steady demand for specialized O&M services through 2032. The implication for executives is clear: commodity maintenance will be increasingly automated and priced competitively, while high‑value services — predictive analytics, integration for hybrid cloud stacks, and sustainability optimization — will command premium margins. That bifurcation creates avenues to reduce unit operating cost while investing selectively in capability areas that drive differentiation.

From a competitive standpoint, concentration metrics indicate a market where a small set of global integrators and platform owners hold sizable influence, but where sizable opportunities remain for third‑party specialists and regional operators to win through service innovation and cost efficiency. For buyers, that means negotiating for outcome‑based SLAs, retaining vendor flexibility through contract modularity, and benchmarking specialized services against a curated set of providers rather than a single market index.

Schneider Electric — Strength in integrated hardware and software platforms. Their combined DCIM and infrastructure management platform positions them to sell lifecycle programs that wrap predictive maintenance, parts replacement, and energy optimization into a single contract.

Vertiv — Thermal and critical systems specialization. Vertiv remains a go‑to for thermal management and OEM‑grade service agreements, particularly where uptime SLAs intersect with heavy cooling loads.

IBM and Kyndryl — Service depth across global footprints. Both bring enterprise‑grade managed services with strong hybrid cloud integration and AI‑driven analytics; their capabilities are attractive for clients aiming to converge IT operations with infrastructure O&M.

HPE — Modernization and consumption models. HPE’s as‑a‑service approach converts CapEx into predictable O&M commitments, which can accelerate upgrades in secure private cloud contexts.

Cisco — Networking and automation leadership. Cisco’s strengths in automation and security align with the need to reduce mean time to detection and remediation across distributed networks.

Colocation and platform operators (Equinix, Digital Realty, NTT) — Integrated delivery models. These operators blend facility ownership with managed service offerings, appealing to enterprises looking for predictable, scaleable operations with strong interconnection options.

Specialists and third‑party maintainers (Evernex, EthosEnergy, Worley, major facilities firms) — Cost control and niche capabilities. These firms provide lifecycle extension, emergency repairs, and on‑site power expertise that can materially lower total lifecycle cost when deployed strategically.

Recent vendor moves illuminate competitive tactics: large platform providers securing multi‑year capacity and service agreements, traditional equipment and system integrators expanding into delivered operations through acquisitions, and facilities management companies winning sustainability‑focused, rolling service contracts. These trends underline a duality: scale players doubling down on integrated offerings while agile specialists push value through service depth and cost arbitrage.

Labor constraints: Industry surveys and analyst estimates confirm widespread difficulty in recruiting and retaining O&M talent. Organizations must plan for both higher labor cost assumptions and investments in automation or managed service partnerships to preserve service levels.

Regulatory and compliance pressure: Updated energy standards and heightened privacy/security certification expectations mean that compliance is now a core operational vector. The cost and timeline impacts of meeting new standards should be baked into 2026 budget cycles.

Capital allocation trade‑offs: Large‑scale labor and operations investment estimates suggest a multi‑billion‑dollar exposure across buildouts and lifecycle maintenance. Firms will need to weigh spend between growth (capacity expansion) and optimization (efficiency, retrofits).

Technology acceleration: AIOps, DCIM maturity, and edge orchestration are converging to make predictive maintenance a realistic, high‑ROI strategy for many operators — but only with disciplined data governance and integration approaches.

Adopt outcome‑based SLAs with clear uptime, energy, and response KPIs; include step‑change clauses for regulatory shifts.

Implement a phased automation plan: prioritize telemetry, anomaly detection, and remote remediation capabilities before workforce restructuring.

Run a vendor hedging exercise: split long‑term capacity services from specialist maintenance to preserve negotiating leverage and continuity of operations.

Embed compliance milestones into project timelines to avoid scope creep when new standards or certifications are required.

Model labor sensitivity in financial plans and include alternative staffing scenarios (outsourced pools, shared service centers, and targeted upskilling investments).

PW Consulting’s study provides a tactical bridge between macro forecasts and executable O&M choices. With a market that more than doubles in size by the end of the forecast horizon under current assumptions, 2026 represents a pivotal year to lock in strategies that control cost, ensure compliance, and capture operational leverage from technology and service innovation.

In keeping with the brief’s role as a strategic “trailer,” this article outlines the high‑value themes and decision levers executives must consider. The full report contains the granular scenario models, vendor scorecards, procurement templates, and segmentation intelligence required to operationalize these insights — including the detailed breakdowns and financial models that underpin our recommendations.

For organizations preparing their 2026 plans, PW Consulting’s Data Center Operations and Maintenance Service Market report is designed to shorten the path from insight to action. Contact PW Consulting or visit our report page to access the complete analysis, vendor matrices, and tailored implementation assets.

For detailed analysis of this topic, please visit the official page:Data Center Operations And Maintenance Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com