Narrowband Internet of Things (IoT) Market Overview: Key Drivers and Challenges

Networking |

2026-02-26 08:01:46

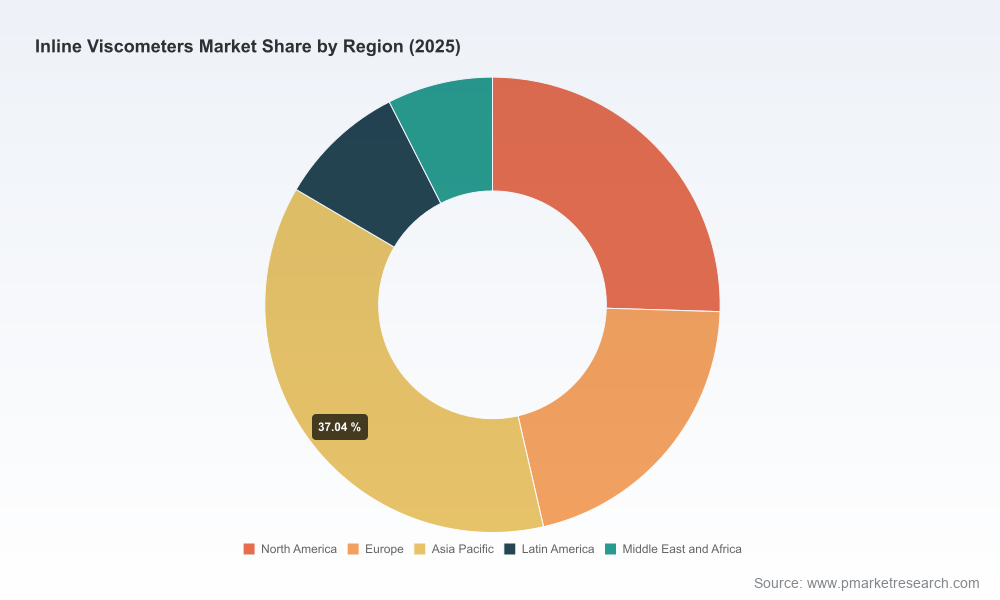

PW Consulting’s latest market research on Inline Viscometers synthesizes five years of historical market behavior with a robust seven-year forecast to deliver a decision-grade view for executives planning investment, procurement, and product strategy in 2026. Anchored on a 2025 base year, our analysis shows the global inline viscometers market expanding at a compound annual growth rate (CAGR) of 6.85% through 2032, reflecting a trajectory from USD 248.5 Million (2025) to an expected USD 395.7 Million by 2032. This brief highlights the report’s strategic value, the operational intelligence within, and the implications for incumbent suppliers, new entrants, and industrial end-users over the coming 12–18 months.

Inline Viscometers Market

Timing. 2026 represents an inflection window where investments in inline process measurement tools will be re-evaluated against rising automation, digital twin adoption, and tighter product quality mandates. Our forecast and scenario work enable CFOs and GMs to align capex approvals with realistic adoption curves rather than vendor optimism.

Inline Viscometers Market

Risk-weighted choices. The market’s steady CAGR masks heterogeneous risk across technologies and end markets. The report translates macro growth into risk-adjusted opportunity maps so procurement and product teams prioritize pilots and scale-ups with the highest ROI.

Inline Viscometers Market

Supplier strategy. With the market moderately concentrated — top firms together account for just over half of industry revenues — our supplier scorecards and negotiating playbooks are calibrated to extract value where switching costs and technical integration barriers are highest.

Technology convergence and differentiation. Inline viscometers are evolving from standalone measurement instruments to integrated process sensors that feed control loops, predictive models, and digital twins. Solutions that enable low-latency integration with distributed control systems (DCS), provide validated APIs, and support edge analytics are positioned to capture premium adoption.

Standards and regulatory environment. ISO 3219:2021 remains the reference for rotational viscometer methods. Compliance with recognized measurement standards is increasingly a procurement gate — especially in regulated segments like pharmaceuticals and food & beverage — and must be a non-negotiable element in supplier selection criteria.

End-market demand drivers. Quality requirements in downstream processing (coatings, adhesives, specialty chemicals), viscosity-critical production in food & beverage, and process control needs in petrochemicals and oil & gas continue to drive demand. At the same time, digitalization mandates in process industries are accelerating replacement of manual lab testing with inline, continuous monitoring.

Service and lifecycle economics. Buyers are moving beyond purchase-price analysis toward TCO frameworks that account for calibration cycles, downtime risk, spare parts availability, and software subscription costs. Service-enabled business models (e.g., performance-as-a-service, predictive maintenance contracts) are emerging as differentiators.

Sensor modalities. The market is technologically plural: resonant/oscillatory approaches, rotational sensing, and emerging vibrational techniques each have niche advantages. Our report maps out where each modality delivers the best trade-off between accuracy, installation complexity, and maintenance burden — without disclosing proprietary segment tables.

Integration patterns. Demand is split between simple retrofit sensors for legacy setups and fully integrated inline units for greenfield projects. The latter category commands higher systems-integration budgets and longer procurement cycles but offers superior data fidelity for control applications.

Digital acceleration. Embedded condition monitoring, remote calibration, and cloud-enabled analytics are accelerating buyer preferences for suppliers with a software roadmap and proven cybersecurity practices.

Our competitive analysis profiles leading vendors and synthesizes strategic positioning across product breadth, go-to-market coverage, integration capability, and service footprint. Below are summarized strategic readouts for select players included in the report.

AMETEK Brookfield (USA) — Strengths: deep penetration in food, chemical, and pharmaceutical process monitoring with established inline sensor lines. Strategic imperative: leverage service networks to convert existing installed base to subscription-based calibration and analytics.

Anton Paar GmbH (Austria) — Strengths: premium engineering and strong reputation for high-precision inline instruments. Strategic imperative: expand systems-integration partnerships to reduce friction for large-scale process control deployments and underscore compliance credentials for regulated industries.

Rheonics AG (Switzerland) — Strengths: resonant sensor technology and dual viscometry-density offerings that appeal to oil & gas and coatings sectors. Strategic imperative: pursue targeted OEM partnerships and broaden regional service coverage to overcome scale limits.

Emerson Electric Co. (USA) — Strengths: integration of viscosity measurement with established flow measurement platforms, enabling higher adoption in process automation environments. Strategic imperative: exploit systems-level architectures to bundle measurement, control and analytics as a seamless offering.

KROHNE Messtechnik GmbH (Germany) — Strengths: strong presence in chemical and petrochemical process instrumentation with broad instrumentation portfolios. Strategic imperative: articulate a clear play for software-enabled servicing to protect margins as hardware commoditization pressures grow.

Across vendors, the report identifies three repeatable plays that are proving effective: (1) software-enabled differentiation, (2) service and lifecycle monetization, and (3) channel expansion via OEM and systems integrator partnerships. These playbooks are described with executable tactics and KPIs to measure success.

Actionable market model: a transparent, auditable market-sizing model covering 2020–2032 (2025 base year), with scenario toggles to test adoption curves, price erosion, and service penetration impacts.

Procurement playbook: supplier scorecards, RFP templates, total cost of ownership calculators, and a staged pilot-to-scale procurement timeline tailored for both retrofit and greenfield implementations.

Commercial and product strategy toolkit: market-entry decision matrices, feature-pricing elasticity insights, and go-to-market segmentation for prioritizing verticals and account types.

Technical evaluation framework: objective test protocols for in-situ validation, calibration verification checklists aligned to ISO 3219:2021 where applicable, and interoperability assessment guides for DCS/SCADA integration.

Competitive intelligence annex: vendor benchmarks, M&A watchlist triggers, supplier risk heatmaps, and negotiation levers keyed to service level differentials and intellectual property ownership.

For Buyers (end-users and OEMs): prioritize pilots that validate not only measurement accuracy but also integration and lifecycle costs. Insist on proof points for remote calibration, cybersecurity posture, and clear migration paths from pilot to full-scale deployment.

For Incumbent Suppliers: double down on recurring revenue models and invest in middleware/APIs that make your sensors the path of least resistance for process automation projects. Consider strategic partnerships to fill regional service gaps rather than large greenfield investments.

For New Entrants and Investors: target differentiated niches where sensor modality confers a clear performance advantage (e.g., high-solids slurries, multi-phase flows) and use performance-as-a-service to lower buyer switching friction.

For Private Equity and Corporate Development: use the market’s moderate concentration as a signal — platform plays that consolidate service capabilities and software stacks can create outsized value, particularly if executed with disciplined integration playbooks.

PW Consulting’s Inline Viscometers Market report is optimized for decision-makers preparing budgets, RFPs, and M&A dockets in 2026. It provides the calibrated demand curves, validated supplier scores, and executable procurement templates that shorten decision timelines and reduce execution risk. The analysis preserves proprietary segmentation details to ensure our clients retain exclusive access to the decision-critical tables and supplier benchmarking for negotiation leverage.

For strategic teams ready to operationalize these insights, PW Consulting offers tailored briefings, data exports from our market model, and workshop sessions designed to translate market intelligence into a 90–180 day roadmap. The public brief above outlines the contours of the opportunity; our full report and consulting engagements contain the granular datasets, scenarios, and implementation playbooks that drive competitive advantage.

To arrange a briefing or to obtain access to the full report and executive datasets, please visit our website or contact PW Consulting’s research desk to receive the executive summary and validation materials.

For detailed analysis of this topic, please visit the official page:Inline Viscometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com