Special Electronic Chemicals for Photoresist Market — Strategic Outlook for 2026 Decisions

Executive summary

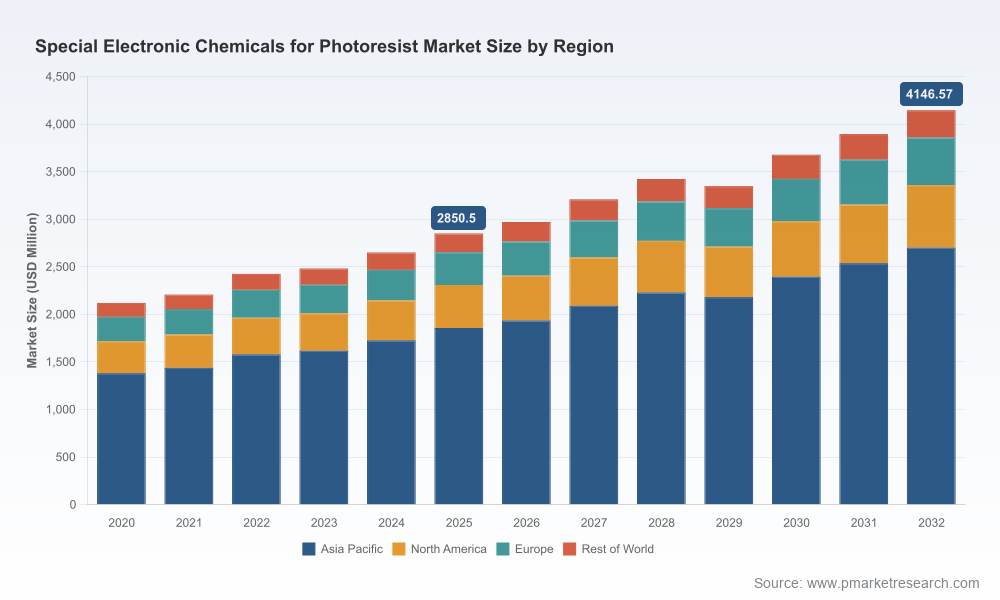

PW Consulting’s Special Electronic Chemicals for Photoresist Market report provides a decision-grade roadmap for executives steering investments, operations, and partnerships in 2026 and beyond. The global market for photoresist-related electronic chemicals has demonstrated steady expansion, rising from approximately USD 2.12 billion in 2020 to USD 2.85 billion in 2025, and is forecast to grow to roughly USD 4.15 billion by 2032 at a compound annual growth rate (CAGR) of 5.51% (2026–2032 forecast period). Market concentration remains meaningful: the top three suppliers account for a majority share of global revenues, and the top five approach three-quarters of the market — an important structural fact for strategy and procurement.

Special Electronic Chemicals For Photoresist Market

Why this report matters for 2026 strategic choices

- Timing and scale of capital allocation: manufacturers and investors need forward-looking clarity on demand inflection points to avoid over- or under-investing in specialty capacity.

- Supply-chain resilience and sourcing strategy: global capacity additions and raw-material constraints require pre-emptive supplier qualification, redundancy planning, and inventory optimization.

- Technology roadmaps and product positioning: the evolution to EUV, advanced ArF, and next-generation resists shifts requirements for resins, photoacid generators, solvents and additives — with implications for R&D focus and co-development partnerships.

- Regulatory risk and sustainability planning: tightening PFAS scrutiny and state-level restrictions in the U.S., together with customer sustainability mandates, create immediate compliance and reformulation pressures.

Market trajectory and near-term outlook

The photoresist chemicals complex is on a steady growth path. After achieving notable recovery and expansion in the 2020–2025 window, the market enters 2026 with momentum but also growing complexity. Our forecast shows mid-single-digit CAGR expansion through 2032, driven by capacity builds for leading-edge lithography, incremental penetration of advanced display applications, and continued support from legacy PCB and mid-tier semiconductor nodes. This growth profile rewards strategic, rather than speculative, capital deployment: selective capacity increases tied to clear demand commitments outperform broad greenfield plays without offtake visibility.

Special Electronic Chemicals For Photoresist Market

Key dynamics shaping 2026 decisions

- Raw-material availability and quality: producers rely on high volumes of solvents and polymer resins to support global production. High-purity grades (with impurity thresholds measured in parts-per-million or lower) have become a gating factor for sub‑10 nm node processing, forcing tighter upstream integration or certification standards for solvent and monomer suppliers.

- Concentration and supplier bargaining power: a relatively concentrated supply base gives leading vendors pricing and technology leverage. This dynamic accelerates supplier consolidation in certain subsegments and makes long-term supply contracts commercially attractive for large consumers.

- Regulatory headwinds — PFAS and beyond: regulators are increasingly scrutinizing chemistries used in photolithography, including certain photoacid generators. Executives must quantify compliance exposure, plan for reformulation costs, and anticipate phased restrictions that can differ at the national and subnational levels.

- Technological displacement and adjacency opportunities: developments such as EUV resist innovation, fluorine-free formulations for immersion processes, and spin-on hardmask adoption create opportunities for differentiated premium products and for materials suppliers to move up the value chain through co-development with foundries and OSATs.

- Capital intensity vs. speed-to-market: recent capacity additions and land purchases by established suppliers underscore the premium value of existing know‑how and customer qualification pipelines versus the time and cost needed to qualify new entrants.

Competitive landscape — what strategic leaders need to know

The competitive field is anchored by several large, vertically integrated players with deep technology portfolios and long-standing customer relationships. These incumbents combine product breadth with global production footprints and advanced application support. Notable strategic signals observed recently include:

Special Electronic Chemicals For Photoresist Market

- Tokyo Ohka Kogyo (TOK): reinforcing long-term supply through land acquisitions for a second plant site and an explicit medium-term capital plan. This underlines TOK’s intent to protect capacity for advanced resists and to support customer qualification timelines.

- JSR Corporation: accelerating regional manufacturing footprint via a joint venture in Taiwan aimed at closer proximity to advanced foundry and OSAT customers, shortening qualification cycles and mitigating logistics risk.

- DuPont: rapid capacity ramp-up at a Japan site completed recently, reflecting a strategy of targeted scale to meet global demand and to secure offtake commitments with strategic buyers.

- Shin‑Etsu, FUJIFILM, Merck (EMD/AZ), and Sumitomo Chemical: maintain diversified portfolios across resist chemistries, solvents, and ancillary materials, leveraging both process expertise and integrated supply chains.

- Specialists and regional players (e.g., Dongjin Semichem, Allresist, micro resist technology, Kayaku Advanced Materials, Eternal Chemical, Halocarbon): operate in niche segments or provide critical upstream inputs such as high‑purity fluorochemicals — often serving as agile partners for quick-turn co-development or localized supply.

For buyers and investors, these dynamics imply that partnerships with incumbents will often bring lower technical and qualification risk, while selective alliances with specialists can accelerate innovation or fill capacity gaps in targeted geographies.

Operational playbook: actionable moves for 2026

- Lock pragmatic offtake and capacity options: prioritize contracts with phased take-or-pay clauses linked to node transitions and customer demand triggers rather than committing to full fixed-volume CAPEX without conditionality.

- Pursue multi-tier supplier qualification: ensure at least two qualified sources for critical high‑purity solvents and polymers, and contractually secure secondary capacity options to manage single‑point failures.

- Invest in upstream analytics and traceability: implement real-time quality monitoring and lot‑trace systems to reduce qualification lead times and to accelerate reclamation of yields impacted by raw-material variances.

- Formulate a PFAS mitigation roadmap: conduct chemical inventories, quantify reformulation timelines and costs, and establish a prioritized list of chemistries for substitution or containment aligned with regulatory scenarios.

- Targeted M&A and JV playbook: prioritize bolt-on acquisitions that add immediate process know‑how, regional production, or unique chemistries; use JVs to share risk for large-capacity projects in proximity to high-growth foundry clusters.

- Embed sustainability into commercial differentiation: customers and regulators increasingly reward demonstrable reductions in fluorinated components and transparent lifecycle assessments; invest selectively to turn compliance into a revenue differentiator.

What PW Consulting’s report delivers (practical and actionable)

This Special Electronic Chemicals for Photoresist Market report is engineered to support board-level and operational decisions across the value chain. Key deliverables include:

- Top-line market model with historicals (2020–2025) and a granular forward forecast (2026–2032), calibrated to multiple demand scenarios and supply-side elasticity assumptions.

- Consolidated supplier scorecards that assess technological capability, capacity maturity, qualification timelines, and financial resilience.

- Scenario-driven investment cases for greenfield versus brownfield capacity expansions, including sensitivity to raw-material bottlenecks and regulatory timelines.

- Commercial negotiation playbooks and contract templates addressing supply security, quality metrics, penalty structures, and change‑control for evolving chemistries.

- Regulatory impact matrix and mitigation timelines for PFAS and related chemical policy shifts at federal and state levels.

- Operational checklists for procurement, quality, and R&D teams to compress supplier qualification and accelerate new chemistry adoption.

To balance brevity and confidentiality, this public synopsis highlights strategic themes and evidence-based guidance without reproducing the proprietary subsegment metrics, supplier revenue splits, or detailed pricing curves that reside in the full report.

How to convert insight into advantage

Executives should treat 2026 as a window to convert market clarity into competitive advantage. That means: committing to modular CAPEX tied to validated demand signals; locking multi‑sourced supply for critical chemistries; accelerating reformulation efforts where regulatory risk is concentrated; and selectively deepening partnerships with incumbents for scale or specialists for speed. For investors, the current market structure rewards capital deployed into technology-focused assets with clear pathways to qualification and offtake.

Next steps — access the full intelligence

PW Consulting’s full report contains the detailed models, supplier level assessments, and the operational templates referenced above. We intentionally limit public exposure to headline metrics and strategic guidance to preserve the commercial sensitivity of our market-level segmentations and revenue allocations. For organizations preparing procurement strategies, CAPEX roadmaps, or M&A due diligence in 2026, the complete report is an essential toolkit.

Contact PW Consulting to obtain the full Special Electronic Chemicals for Photoresist Market report, bespoke briefings, or a scenario workshop tailored to your portfolio or supply‑chain exposure.

For detailed analysis of this topic, please visit the official page:Special Electronic Chemicals For Photoresist Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com